Around noon on Friday, March 30th, I was giving a presentation for the Financial Planning Association of New England. It was on one of my favorite topics: Social Security. The first question I asked the audience was “When is Social Security going bankrupt?” Most people said around 2034. That’s what pretty much everyone thinks. The problem is that’s not the answer. Social Security is NOT going bankrupt. Not in 2034. Or in 2033. Not ever.

At the very same time I was delivering this message, the Social Security Trustees were releasing the 2023 Trustees’ Report. This massive 276-page report gives both houses of Congress, and the rest of us, a comprehensive review of two trust funds. One of the many, many areas they report is when the Asset Reserve Account is likely to be depleted.

That’s where all hell breaks loose. Every year. Just like clockwork. More on the mayhem further in…

OASI vs DI

The Trustees’ report contains a tremendous number of interesting facts and stats. Financial advisors should be well-versed in this information. For example, the following are basic facts about how the two Trust Funds are structured:

- OASI is the Old Age and Survivor Insurance fund. It pays retirement, widow(er), and minor children’s benefits. The DI trust fund—Disability Insurance—pays monthly income if you become disabled. Each trust fund is funded separately and assessed individually.

- The Social Security “old age” fund was became law in 1935. Then in 1939, survivors, spouses, and disability provisions were added.

- A Board of Trustees was created in the original 1935 law to oversee the financial operations of both Trust Funds. You know the Trustees: Treasury Secretary, Janet Yellen. Labor Secretary, Julie Su. HHS Secretary, Xavier Becerra. Social Security Commissioner, Kilolo Kijakazi. Two public representatives’ slots are open.

- This is the 83rd comprehensive report. Not really a new thing.

The size, scope, and scale of this program is impressive

Individuals trying to deal with the Social Security Administration (SSA) about their benefits often find it frustrating. It’s particularly challenging when trying to get the right information about survivor benefits. Each of us needs specific information related to our own unique situation. But Social Security is set up to handle large scale customer service.

From the SSA’s perspective, they must deal with 66 million Americans, two different trust funds, and Medicare enrollment. The Social Security program is massive. Gigantic. Enormous. Choose your favorite word.

The fact of the matter is, no one organization, especially an under-funded one, can provide the level of service we all think we deserve. So, it’s important to realize what these workers are up against:

- They deal with 51 million retired workers and their dependents. Those dependents may be a spouse, and ex-spouse, minor children, or disabled adult children, or a combination. Dependents may also be the worker’s parents in some cases.

- The agency also deals with 6 million surviving spouses, surviving ex-spouses, and the minor children of the deceased worker.

- Let’s not forget the 9 million people who are disabled and their dependents and families.

Our charming personalities shine through

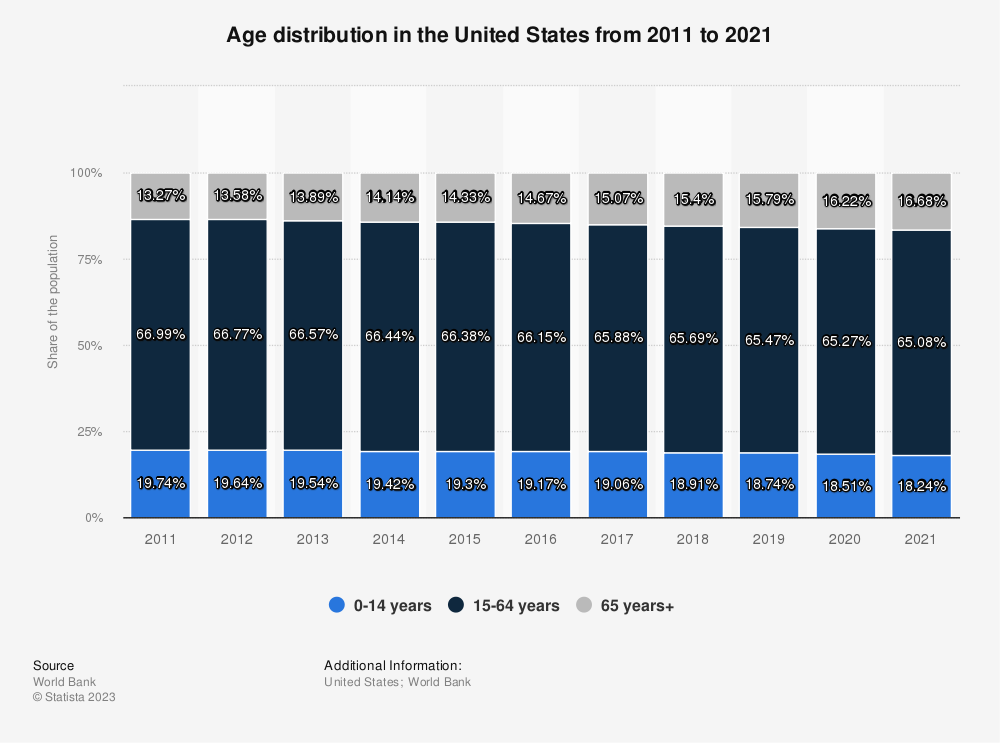

To put these numbers in perspective, the population of the US is approximately 332 million. Roughly 55 million are aged 65 and older. That’s about 16.7% of the total population.

Just in the last decade, the 65+ population has grown by leaps and bounds. From only 13.3% of the population in 2011 to 16.7% now is dramatic demographic change. Take a look at this graph from Statistica:

Social Security agents deal with every one of these older Americans. So, they routinely deal with 55 million charming personalities, all with diverse needs and family situations. And must remember and apply thousands of rules that sit underneath some 4,800 pages of the Social Security law.

The agents also handle another 10 million requests for those who have qualifying disabilities. And it’s not a one-time benefit claim. Often, those with disabilities move in and out of needing benefits.

Oh, and by the way, the SSA agents also process your enrollment into Medicare. And all the appeals filed for IRMAA redeterminations. (Read more in this post.)

All this is to say, Social Security is a gigantic program serving tens of millions of Americans. It is the law of the land. And it is complex. Only Congress can make changes to the law. And importantly, Social Security is not going bankrupt.

Billions of transactions…Trillions of dollars

The goal of the Trustees’ Report is to report to Congress on “the actuarial status and financial operations of the OASI and DI Trust Funds.”

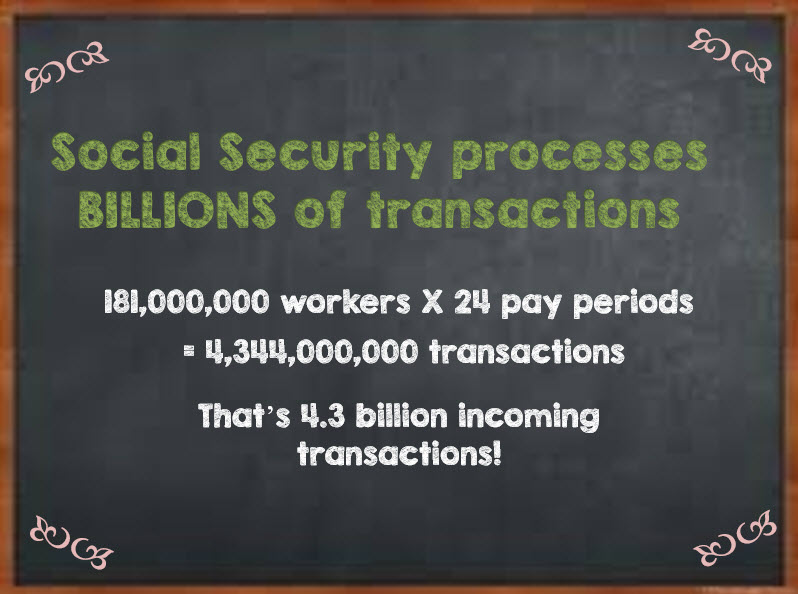

The public can find a complete accounting of the inflows and outflows of these funds in this report. If you thought the program was gargantuan from the last section, here’s where the volume really ramps up. In 2022, about 181,000,000 people worked for wages in covered jobs. That means 181 million workers’ wages paid FICA taxes.

If we assume payroll cycles are twice a month, the volume flowing through the Trust Fund looks something like this:

Furthermore,

- In 2022, the OASI (retirement) Trust Fund receipts totaled $1.057 Trillion.

- Payments made to retirees, survivors, and dependents hit a record of nearly $1.1 Trillion.

- That means something in the order of 684,000,000 payments were made on time to all non-disabled beneficiaries.

Yowza. Those are some huge volumes.

Not a single mention of “bankruptcy”

The goal of both Trust Funds is to provide adequate funding for 75 years of benefit payments. If that goal is not going to be met, the Trustees estimate when full benefit payments would be reduced.

It turns out there is a table in the report showing when a portion of retirees’ benefits could be cut. In the current report, recipients could see a decrease in monthly benefits starting in 2033. That is, if Congress doesn’t take decisive action to shore up the funding of the program.

This report, and all 82 prior reports have clearly stated if and when funding of OASI will be insufficient to meet obligations owed to retirees and others.

What you will not find in the report is when Social Security will go bankrupt. Throughout the entire 276-page report, there is not a single mention of Social Security going bankrupt. That’s because Social Security is not going bankrupt.

Rather, what you find in this year’s report is the Trustees’ note of the status:

“…the OASI Trust Fund reserves become depleted in 2033, one year earlier than projected in last year’s report. And, as in last year’s report, the DI Trust Fund reserves do not become depleted within the 75-year long-range projection period.”

More about that “Reserve” account

Notice the missing word in all the alarming headlines: reserves. Turns out, that’s a super important word. And it is one of the many reasons why Social Security is not going bankrupt.

It’s not that the entire OASI Trust Fund is in danger. It’s that the reserve account is being used up. Yet, most media stories feature blistering headlines about the full and utter failure of Social Security.

The reserve account is essentially a savings account attached to the huge checking account that is the Trust Fund. When there is excess cash at the end of the month, it gets routed to the asset reserve account. The Trust Fund works quite like your own checking account with a savings account attached.

The assets in the reserve account are now being used to pay current retirees 100% of the benefits they are owed. Even though 181 million workers paid FICA taxes, those income dollars are not enough to pay the 57 million beneficiaries. In 2022, there was a $40.7 Billion shortfall between incoming dollars and outgoing payments.

The reserve account had $2.75 Trillion in it at the beginning of 2022, so there was plenty to cover the shortfall.

Isn’t anyone minding the store?

Those who are accountable for the payment of benefits have known for a long time that the reserve account would be tapped to pay benefits. In fact, Congress and the Trustees have known since 1983. So, for the last 40 years.

The Reserve Account has been tapped before. In fact, in the 1980 Trustee’s Report you’ll find this reporting on page 3:

“Short-range (1980-84)-Under all three sets of assumptions, expenditures from the OASI trust fund are expected to exceed income in every year during this period. Under present law, the assets of the OASI trust fund would soon become insufficient to pay benefits when due. This would occur late in 1981 under the intermediate and pessimistic sets of assumptions, and early in 1982 under the optimistic set. Accordingly, changes in the law are needed so that OASI benefits will continue to be paid when due.”

1980 Social Security Trustees’ Report

Well, well, that certainly looks familiar. Yes, back in the 1970s and early 1980s, Social Security was also going “bankrupt.” And retirees were understandably concerned their benefits would be cut.

Until the reserve account had nearly run dry and recipients were due to have delays in their monthly payments, Congress didn’t act. It also helped that a presidential election cycle was ramping up.

1983 Social Security Amendments

That last crisis era ushered in the 1983 Social Security Amendments. To shore up the system, significant changes were made by Congress including:

- Increasing the retirement age from 65 to 67 in two-month increments.

- Increasing payroll tax on individuals and self-employed people.

- Adding a tax on 50% of benefits for those above certain income thresholds.

- Expanding participants into Social Security and FICA to include Federal government employees, Congress members, and federal judges.

- Created the Windfall Elimination Provision, reducing benefits for those who have both an uncovered pension and qualify for Social Security.

Even with these changes, one thing was abundantly clear: There would still be a shortfall in meeting monthly payments when the baby boomers reached retirement. The first projection estimated the reserve fund would meet payment demands until about 2050. By 1991, projections for funding shortfalls dropped to 2041. And by 1996, full benefits were projected to be paid only until 2029.

For the last decade or more, we’ve all known that the mid-2030s would be the tipping point. Incoming FICA dollars would not be sufficient to pay out the benefits in this self-funding program. The reserve fund would have to make up the difference.

Despite it all, Social Security is not going bankrupt

While the media sounds the alarm that Social Security is going bankrupt, it’s important to keep in mind the realities of the law. And how Congress works.

There is no imminent danger here to meet benefit obligations. There’s nearly $3 Trillion in the reserve account. It will keep payments whole for another decade.

See? What’s the rush to fix Social Security? There’s so much time. Ha.

Congress simply does not work on anything that isn’t a crisis. There are other fish to fry. We have our next presidential election cycle already underway. While I expect Social Security and Medicare to be key positions in the platforms, no changes are likely to take place yet.

So, it’s a matter of patience. And, somewhat of a leap of faith. That’s a tall order in our current climate. But a necessary outlook. Otherwise, the danger is making sub-optimal decisions about claiming Social Security. In the end, claiming early will only hurt you and your old age lifestyle.

Social Security is not going bankrupt. Congress knows it. And will eventually get around to shoring up this bedrock of American retirement income. But probably not for another 10 years. Stay tuned…

Additional Reading

The Crisis Last Time from the Brookings Institution – a 2005 article about how Congress did manage to compromise and shore up Social Security in 1982 – 1983

Social Security Trustees Report of 1980 – PDF of the report

Social Security Trustees Report of 2023 – released on March 30, 2023 – Landing page on SSA.gov

The last time I wrote about Social Security is Not Going Bankrupt

And, an analysis of why Social Security is not going bankrupt

And of course, you can get much for information about your individual Social Security claiming strategies in my book: What’s the Deal with Social Security for Women.

(It’s for men too!)