…and there is good news

I always know when there’s big industry news day because my daily enews reports come flying in with similar headlines. Today was a good day. The Centers for Medicare and Medicaid Services (CMS) announced the 2023 Medicare Part B Premiums. And be still my heart…they are actually lower than the 2022 premiums.

The Standard Part B Premium

Everyone, unless they qualify for a low-income subsidy, pays the standard or base monthly premium. In 2022, those with Medicare Part B pay $170.10 per person, per month. The 2023 Medicare Part B premium was reduced to $164.90.

The reduction is a nod to a situation last year. A new Alzheimer drug was expected on the market last year, called Aduhelm. It carried an extraordinary price tag. $56,000 per year. And Medicare would have had to pick up the tab for those on Medicare.

So, they adjusted the Medicare Part B premium from 2021’s $148.50 per person per month up to the $170.10 you’ve been paying in 2022.

Then, in a rare move by the pharmaceutical manufacturer of this drug, they lowered the price. Cut it by about 50%! But it was too late for CMS to turn the ship around.

They didn’t forget about the larger than expected premium bump last year and were able to lower it slightly this year.

My article in Retirement Daily

I was fortunate to share this good news first on Retirement Daily. My recent article explains more on the 2023 Medicare Part B premium as well as other cost changes. You can read the article directly on Retirement Daily.

You can also watch a video interview of me talking to editor, Bob Powell, attached to this article.

Keep in mind that Medicare is a “quartet” – a compilation of four very different pieces. Costs in Part A are increasing for those who do not have a Medigap or Medicare Advantage plan. Some Part D plan premiums are up…some are down. Plus, drug prices always run amok.

For your primary resource, you can visit Medicare.gov’s page on pricing.

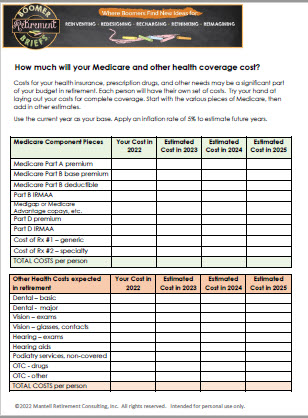

A new worksheet for your health care cost budget

Make sure you take the time to put your entire “Medicare” budget together.

Earlier this year, I started piecing together various insurance and drug line items we need to consider once in Medicare. It’s not just 4 piece-parts. I’ll attach it here so you can update your costs for the 2023 Medicare Part B premium. And estimate all the other costs you’re dealing with.

Give it a try. If you find there are other key cost areas I’m missing, please shoot me a note. I’m happy to update any of the worksheets I develop.

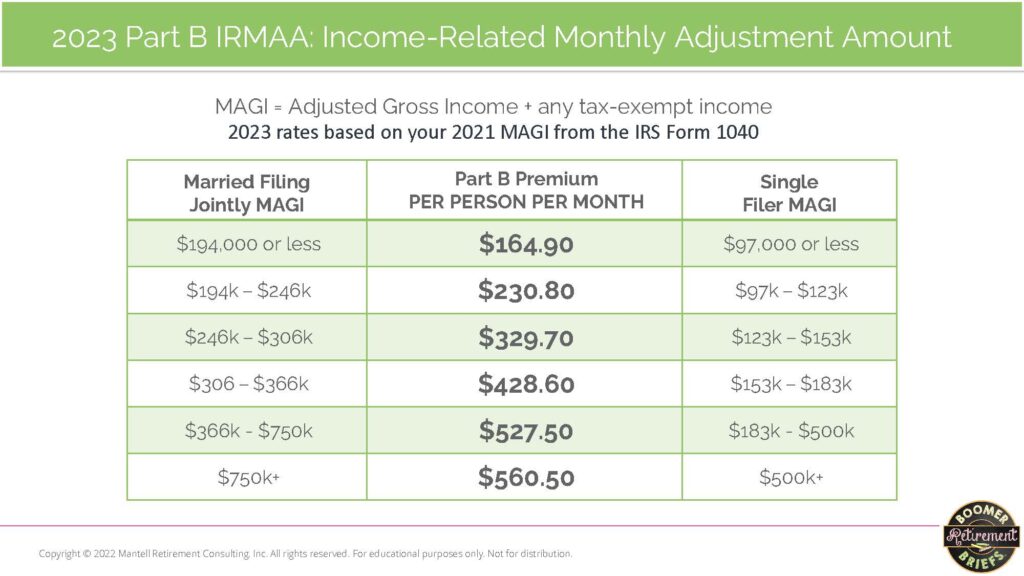

IRMAA – the gal you don’t want to meet!

Whenever I talk about Part B premiums and the means testing part of Medicare, I introduce “IRMAA.” And immediately, a 1940’s young woman working at the USO carrying a donut tray pops into my head. I think the name Irma seems like it’s a WWII name. But when talking about IRMAA and Medicare, oof. Look out!

IRMAA is the Income-Related Monthly Adjustment Amount. And this name does capture what we’re talking about here. Based on your income during your retirement years, you may have an adjustment to your Part B premium. And by adjustment, I mean an increase.

When you have income higher than a certain threshold each year in retirement, you’ll pay more for Medicare Part B premiums. That’s because higher income folks are getting less of a Federal Government subsidy toward the total premium.

2023 Medicare Part B Premiums for Higher Income Folks

Here’s a look at the 2023 Part B IRMAA amounts. Check out the much higher income brackets for both married, filing jointly couples. And for single filers.

Any IRMAA charges for 2023 will be based on the income you reported on your 2021 tax returns. You filed those returns earlier this year (usually by April 15th-ish). Social Security will use that information to see if you will pay a higher 2023 Medicare Part B premium.

Expect a letter from the SSA in early- to mid-December with your specifics.

Stay tuned for more Medicare information

I’ll continue to post information about Medicare and Social Security as information becomes available. And do let me know if you have questions. Dealing with the consumer-driven health care system is nothing short of nuts. I’m happy to help where I can.

Quick reminder, we’ll be entering the Medicare Open Enrollment Period shortly. Starting October 15 and going through December 7th. I’ll get some new Part D information out to you in the next blog. Meanwhile you might want a refresher here: Re-shop your Medicare Part D Plans.