You may recall last month’s blog post, Social Security Solvency: It’s Here to Stay. In that post, I shared where you can get the numbers to see how the program is working and what the projections are for its longevity. This month, I wanted more analysis of Social Security solvency in a way to bring home how impactful, or not, changing Social Security would be on the retirement income of retirees and near-retirees. And, on your retirement income.

I’ll give you the big ah-ha right up front: Social Security solvency simply must prevail or we will have a massive public policy catastrophe on our hands, and you’ll starve in old age.

There Is Time to Shore Up Social Security

Too dramatic? Well, maybe. And, I usually try not to be an alarmist. But, after you see the results from the two scenarios in my analysis, please run your own numbers. You’ll want to have a good handle on what your situation looks like. Unless you’ve saved millions of dollars, paid off your mortgage, and plan to live like a pauper in retirement, you need to see where you stand in terms of the importance of Social Security solvency.

It’s fair to say that those of us closest to and living in retirement have concerns about Social Security solvency. It’s also fair to say that we’ve got time to shore up this critical income source. We need to encourage our representatives in Congress to get on the stick and solve this solvable situation. Make sure you know where your Congressional representatives stand on shoring up Social Security and vote in the November election.

Creating Income in Retirement Starts with Social Security Solvency

Your retirement income will come from various sources of money such as pension plans, 401(k)s, 403(b)s, IRAs and other savings and investments. The more you get from one source, the less you’ll need from another. There is no perfect formula for how to draw from each source. That’s why you need to figure out your strategy well before retirement.

As a general guideline, Social Security is the foundation, or the first source of income to consider. Once you lock that in, you start drawing down from your other savings. But how much will you get in Social Security? How will you know you are making the right decisions about when to start claiming? What if Social Security does get cut in the future and how will the change affect you?

To help think about these options, I ran several different scenarios to see just how important Social Security solvency is to all us Boomers. Keep reading for some eye-popping results!

Some Background on My Social Security Scenarios

I am amazed by the Baby Boomers who tell me that they don’t believe Social Security is going to be there for them. I ask if they’ve prepared a detailed retirement income plan yet. Of course, the answer is almost always “no”.

Let me say how critical it is that you create a retirement income plan. Today. Get some of your numbers on paper so you can see what you are dealing with. There are plenty of helpful online tools for you to use. You can call many of the large financial services firms to have them help you develop a plan over the phone—a particularly good route if you are a self-directed, DIY investor. Plus, there are excellent financial advisers who specialize in helping clients build comprehensive retirement income plans.

For the purpose of my analysis to look at the implications of losing or reducing Social Security benefits, I used the Retirement Income Calculator on T. Rowe Price’s individual investor website. It’s a bit clunky to use. But, in just 5 minutes, it gives you a rough idea of where you stand. It shows the magnitude of your ability to pay for retirement with and without Social Security.

Case 1: Sally Snowflake, A Single Lady

This first analysis looks at a career woman who is planning for retirement. She’s 58 years old (born March 1960) and plans to work until age 67, her Full Retirement Age (FRA) according to Social Security. She makes $145,000 per year and has saved $470,000 to date. She’s got another 9 years to continue saving and will do so. She has a balanced asset allocation, meaning her investment portfolio is invested 60% in equities, 30% fixed income and 10% cash. Overall, she’s feeling confident that she’ll be able to keep working and that her savings plus Social Security should provide a nice income for her in retirement.

At her salary, she nets about $7,600 per month, after saving in her 401(k) and paying taxes. She’s working on paying off her mortgage completely by retirement. Her target spending amount in retirement is $6,000 per month. A rough estimate of her Social Security payment is $3,040 per month. so she’ll have to draw down her savings at $2,960 per month to meet her $6,000 goal. She’s also planning that her retirement will last until age 95.

Sally’s Initial Results

Entering all of this data into T. Rowe Price’s Retirement Income Calculator, Sally’s initial results are the following:

- Assuming a $6,000 per month budget in retirement, Sally has a 68% chance of her assets lasting until age 95. And that is with her waiting until FRA of 67 to collect her full Social Security payment of $3,040 per month.

What? Only a 68% chance she won’t run out of money? After all her hard work at saving and off her mortgage? Yup.

The tool goes on to suggest that if Sally can reduce her spending to about $5,600 per month, she’ll have an 80% chance of her money lasting. If she can reduce her spending by a full $1,000 per month, and live comfortably on $5,000, her chance of having money until age 95 reaches 94%.

Eliminating or Reducing Social Security

Let’s address those who believe Social Security solvency is going bust, leaving all of us near-retirees out in the cold.

- If Sally plans for $0 from Social Security, there is only an 18% chance that her portfolio will last to 95. That’s essentially no chance at all. She’d have to further decrease her already reduced budget from $5,000/month to $2,500/ month just to get an 80% chance of having money at 95.

A more measured analysis says that we should all look at the implications if Social Security solvency is protected, but reduced by 25%.

- In the 25% reduction scenario, Sally’s Social Security income would drop from $3,040/month to $2,280/month. If she can budget for a total spend of $5,000 per month, she’s got a 75% chance of her savings lasting to age 95. Decreasing her spending a couple of hundred dollars more per month, to $4,840, her odds of having money at age 95 moves up to 80%.

Case 2: Sally Snowflake & Richard Raine, Happily Married Couple

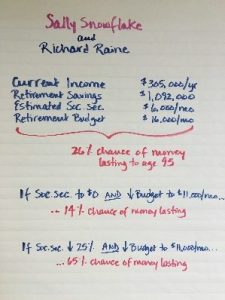

In this next analysis, Sally’s parameters stayed the same, but now she’s married to her college sweetheart, Richard. He brings a lot to the party. He’s saved $622,000 in various retirement accounts. His salary is $160,000 per year. Richard is 18 months younger than Sally, and he plans to retire when he reaches his FRA at age 67.

Together, they make a pretty healthy income, and they spend a good amount to run their household. In this example, they expend about $16,000/month. For their first attempt at planning for retirement income, they assume they will spend about the same. They will not have their mortgage paid off, but with over $1 million saved already with 10 more years of savings to come, and Social Security of just over $6,000 per month for the two of them, they think they are in good shape to retire as planned. Are they being too optimistic?

The Initial Results for Sally and Richard

Again, using T. Rowe ‘s calculator, and assuming they will continue to spend $16,000 per month, the result is a 26% chance that their savings will last until age 95. This is a stark look at the impact of losing those power paychecks. Yes, they are too optimistic!

Furthermore, the calculator shows that in order to reach an 80% chance of having some savings at the end of retirement, they have to cut their spending down to $11,600 per month. That’s a 28% reduction in their budget. They were not expecting that.

They thought they might be prepared to cut some out of the budget, perhaps getting down to $13,000 per month. Yet even that significant decrease only moves the likelihood of having income at the end of their retirement to 62%.

Now, Consider Cutting Social Security

Moving forward into the analysis, I took a look at changing two key parameters: (1) If they drop their spending to $11,000 per month and (2) if they assume $0 in Social Security.

- This result showed that there’s a 14% chance of having any money left at all. Ouch. If Social Security were eliminated entirely, they would have to reduce spending to $5,500 per month. That’s a 66% decrease from their original $16,000 target. How could they afford that kind of cut in lifestyle spending?

- If Sally and Richard experience a 25% cut in Social Security, down to $4,516/month, and cut their spending to the $11,000 target per month, they still end up in dire straits. They would have a 65% probability of having any of their personal savings at the end of retirement.

How High Should You Aim?

These are significant dilemmas that Boomers all over the country are facing. And, it’s not good news. Many financial professionals still aim for clients to have an 80% probability that they should have some money at the end of retirement. Since there are so many unknowns, advisors do have their hands somewhat tied. Personally, I am not at all comfortable with only an 80% chance that I’ll have money if I live well into my 90s. If I am alive and well at 95 or 98 or 100, I want to know I’ll have enough money, not an 80% chance.

Finding out your money probably won’t last on your 75th birthday is much worse than finding out about it at age 55 or 60. There is still time to make some critical moves if you understand the possibilities before you decide to leave that paycheck from your employer behind.

Why This Kind of Analysis Matters

What I particularly like about the T. Rowe tool is that it gives you reasonable comparisons. It shows the likelihood that all of your savings will or will not last as you draw on them for income in retirement. It includes Social Security, pensions, annuities and whatever savings you have available for income. Comparisons and options are based on your inputs. All in a short amount of time. It’s a place to focus on 3 critical issues when planning for your own retirement income:

1. Budget

You have to know how much you will be spending each month in retirement. If you don’t want to call it a budget, that’s fine. But how much does it take to run your household? Where do you have wiggle room to cut back if you need to?

2. Longevity

Unless you are already suffering from a chronic illness that comes with a deadline, you should plan for a long retirement. Not all of us will get decades in retirement, but you’d better have enough money if you do live to 100. Half of us will live to our late 80s or early 90s. Twenty-five percent of us will live to 95 and beyond.

3. Social Security solvency matters

And, it matters a lot. Regardless if you are feeling rich or not so rich, Social Security makes a gigantic difference to the health of your retirement savings. If you claim at 62 for no particular reason, you’ve started your retirement income with a 25% or more pay cut from Social Security. If there is a further 25% cut in benefits from the program starting in the mid-2030’s, that might put another significant damper on your spending plans.

The important perspective these online tools provide is a comprehensive view of your various buckets of money and how the sources interact. You need to see what you’ll have available for income before you quit your job and move into retirement. Plus, what would happen if one of the income sources changes during retirement? Your electric bill won’t stop coming. You’ll need to eat. And, paying for health insurance isn’t discretionary.

What to Do for Your Own Situation

It’s not that hard to do a topline analysis of your personal household finances. The Sally and Sally/Richard scenarios are totally made up, so they don’t apply to your specific situation. So, gather your own information and stick the numbers in a tool. Use the T. Rowe calculator. Use one at Fidelity or Schwab or Vanguard. Call the 800 number and ask a representative to help you pull together an initial plan. Carve out an hour or two to get a baseline look at your financial picture. Only you can do this.

Here are the 5 key numbers you need for a topline view:

1. Your 401(k), 403(b), and other retirement assets in total. Include your spouse’s or partner’s totals if you have one.

2. The total amount you spend each month. It doesn’t matter where or why you spend the money. Just tally up an entire month of expenses and consider that the starting point.

3. Your mortgage payments. Will your mortgage be paid off before you leave your employer paycheck behind? If so, you can decrease your monthly spending by the amount of your mortgage. Just the mortgage. Your property taxes and homeowner’s insurance will continue.

4. Any income coming from a traditional pension. Yes, lots of Boomers will still receive a pension. If you are one of them, about how much will you get each month once you turn it on?

5. Your estimated Social Security retirement benefit. It’s best to use the estimate on your most current statement as a starting point. Go to SSA.gov/mySocialSecurity to set up your account if you haven’t already.

That’s it. These are the big-5 that drive most people’s retirement income. You can, of course, go into much more detail. And you should the closer you are to retirement. But for now, the goal here is to get about the right magnitude. What are your resources versus expenses? Put them into an online tool to get a baseline. You may be surprised at the results!

And Last, Answer Just One Question

The reason I so strongly encourage you to spend the time planning for INCOME is because it’s so very important. You want to get to the bottom of one critical question when thinking about retirement income and the importance of Social Security solvency. Will my assets and income sources last until age 95?

Depending on the answer you get, you may need to get more serious about your estimates and assumptions. You can look for a qualified financial advisor with specific expertise in retirement income and Social Security. Or, you can do your own deep-dive into the numbers. The choice is yours. Just dig into the weeds so you know what you’ve got to work with.

For more information about Social Security Solvency:

Review my blog posts. You’ll find resources to help you better understand some of the workings of Social Security. Plus there’s good information to know before you decide when to claim.

- Check out my Social Security Scavenger Hunt to help you find your way through the Social Security website

- Read about the 4 Claiming Strategies and see which category you fall in today.

- If you don’t have a financial advisor, this checklist might help you find one. Ask them about their expertise with Social Security claiming strategies and options.