Time to take a fresh look

April is National Social Security month. An opportune time to take a fresh look at your benefits estimate. Even if retirement is years away. If you haven’t taken a peek lately, you’ll be surprised to see a new version of the Social Security statement.

Simply log into your online account or create your own “MySocialSecurity” account on SSA.gov. Here you’ll find your most current statement updated with 2021 income information. That is, unless you’re already collecting Social Security benefits. Statements stop at that point and are replaced with payments to your bank account. But you’ll still have access to other communications and information in your account.

Perhaps Your Most Important Retirement Income Tool

Why am I spending an entire (and long) blog post on a statement? Well, your Social Security statement contains just about the most important information for your retirement income. It gives you a close estimate of how much you may receive each month of your (hopefully) long retirement. On the statement, you’ll see:

- some of your own work history,

- whether you qualify for benefits on your own, and

- how much your dependents would receive if you die too soon.

Your personal Social Security statement It is the number one document we want you to understand. And by “we” I mean those of us who work in the retirement income industry.

During the COVID-19 pandemic, the folks at the SSA decided to redesign this incredibly important document. When you pull down your current version, you’ll see it underwent quite a “face lift.” The new design is noticeably different…and not in a good way.

Lots of Missing Information on the Latest Social Security Statement

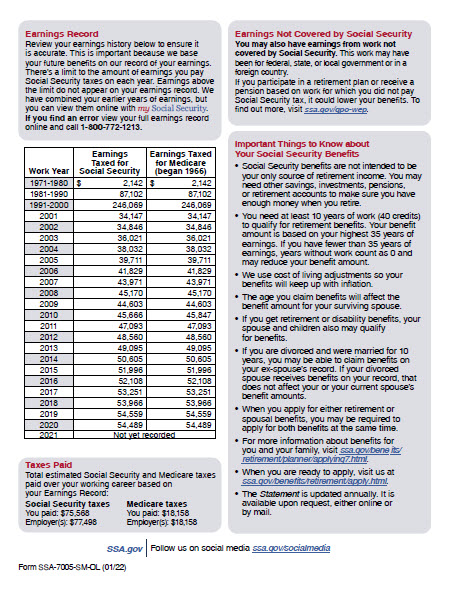

For the last 20 years, the Social Security statement has provided a specific set of information in four pages. From that information, you and your financial advisor could make clear, correct decisions about when to claim. The most important information it provided was a look at your year-by-year earnings record. In a shocking move, the SSA removed the earnings history from the latest version.

The statement has been cut to two-pages and only the most current 16 years of your work history are displayed. That won’t help you decide if you have enough years to get a maximum benefit or how many more years you should work. It’s fine if you are a 35-year-old. But not when you’re 60 and trying to make critical work or quit decisions. Or navigate your options after your job was eliminated.

Why is it important to see all your years of work history? Because your Social Security benefit amount is calculated based on your highest 35 years of earnings. A wage index factor is applied to boost your earnings from the 1980s into the modern era. But seeing the entire view of your work life helps you make key decisions for your retirement income.

Why the Earnings History Is So Important

Your personal wage history is the single most important input into your benefit calculation. Every dollar from every job where you ever paid Social Security taxes may be used in the calculation. And, now, you can’t see your full journey.

For those of us Baby Boomers who have 40 to 50 years of adult life in the rear-view mirror, we need to see our full work history. It’s important to know if we’re missing 5, 10, 12, 25 or more years. If you took any time off between jobs over the past five decades, you may well have a bunch of zeroes in your work history.

Or, if you worked in a low-wage jobs for 10 years during your work life, you can’t see that on the new version of the Social Security statement. But you can replace low-wage years with higher-wage years. If you know about that.

Importantly, when you fill holes in your work history or replace low dollar years with higher income years your estimate changes. Net effect: your benefit will be higher.

Who Has Zeros or Low Income in Their Past Work History?

Pretty much everyone! Millions of Boomers have some years of zeroes due to all kinds of life journeys. Most frequently, moms and a handful of dads stayed home to raise children. Every year at home earned you a big zero on your wage history.

Others have plenty of zeros for reasons such as,

- Years in graduate/medical/law school

- Periods of unemployment

- Working for a state or local government

- Working in a union with a pension benefit

- Stepping out of the workforce to care for an elder or sick person

- Resigning during COVID

- and more…

Knowing how many zeroes you have to replace with years of wages helps you decide how many more years you might work. If you only have one or two zeros, it won’t make a big difference in your calculated benefit. But, if you are like millions of moms who stayed home for 15 or 20 years, replacing some of those years with wages can make a substantial improvement.

Of course, you now won’t know that by looking at your statement.

Time To Get Out Your Shovel

Again, you can dig around your mySocialSecurity account page to find your full earnings list going back to 1979. But would you know to even look for it?

Not having your entire work history at-a-glance significantly reduces your decision-making data.

This is not the only missing information. Other critical information was eliminated or greatly scaled back on this latest version. The good news is you can dig around your personal account after you log in. Much of the missing information is there somewhere. But the problem is most folks won’t know they’re missing key, critical information. And the danger is they will make less than ideal decisions about when to claim. Or about boosting their monthly benefit amount.

Ok, But I Just Want to See How Much I Can Get

Well, good luck with that on the new statement! Remember the big banner across the top of the statement? It showed your full-retirement age estimate in gigantic type. It has been removed. Are you kidding me? How on earth are people supposed to see their latest estimate and make good decisions about claiming?

Your age when you decide to claim Social Security sets all kinds of financial wheels in motion. For you, your spouse if you are married, and even for dependent children.

Most of us just want to start somewhere and see how much we’ll get. Your target, or optimal, benefit comes at your Full Retirement Age, or FRA. That’s between 66 and 67 these days.

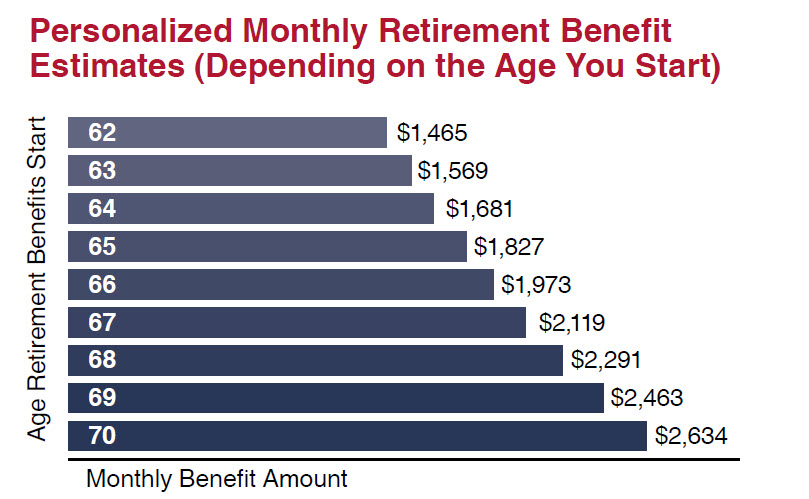

Instead of seeing that on the statement, you now see a bar graph with numbers. It shows how much you’ll receive if you claim at ages 62, 63, 64, etc. The problem is that it can be misinterpreted as these are the amounts you’ll receive when you start at 62, then get a bump up at 63, another bump at 64, etc. all the way up to age 70.

Putting a Puzzle Together

A key puzzle piece is buried in the top left gray box. This is the only place you’ll find your Full Retirement Age. You need to map that age to the chart to see your target benefit amount. You only receive that amount when you claim at your own FRA.

It’s only once you reach your FRA that you receive the full value of your benefit. You can decide to wait until after your FRA to start your benefit. Then, you receive the higher amounts shown on the chart.

However, if you decide to claim early, before FRA, you start with the reduced payments you see on the graph. But they can be reduced even further if you are still working.

In any case, the numbers on that graph do not represent what you will receive at the corresponding ages. They simply indicate how much more or less your starting benefit amount will be based on your age when you claim.

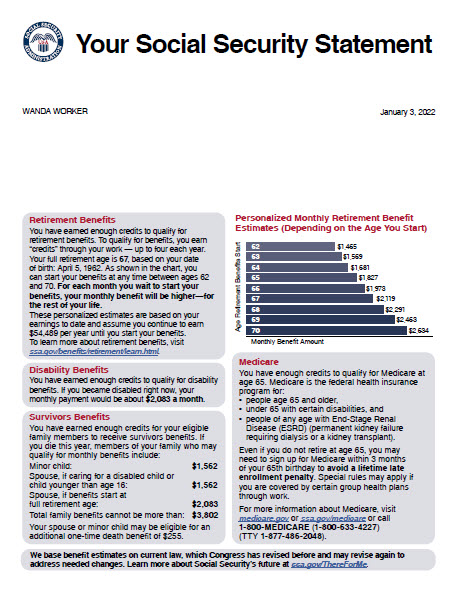

Meet Wanda Worker

Here’s an example from the “Wanda Worker” sample Social Security statement. Her benefit at age 62 is $1,465. Then, at age 63 her benefit bumps up to $1,569 according to the chart. And so on until age 70 when her benefit jumps up to $2,634 per month.

That is not at all what happens. Once you select your claiming date, you have permanently anchored your starting benefit payment. Only cost of living adjustments or additional earnings will increase your base amount.

In this example, let’s assume Wanda claims at age 62 (as do more than one-third of retirees – yikes!). Her benefit is locked in at $1,465. At age 70, she would only receive about $1,855, assuming a Social Security COLA of 3%. A far cry from her statement that show her she’ll get $2,634 at 70.

The Graph Is Nevertheless An Improvement

Despite problems showing a graph without any explanation, it is helpful to show all ages when you can claim. And, the corresponding starting value of your benefits.

In previous statement designs, you only saw three estimates. The minimum benefit amount at 62, the maximum at 70, and your estimate at FRA. But people claim at various other ages, often at 65. You’d have to call Social Security to get in-between benefit amounts. Or try to use the online tools to figure out your estimated benefit.

This new graph is helpful in one key way. It visually shows the significant difference in payments at 62 and at 70. Instead of claiming at 62, if you can wait until age 70 you do get substantially more. Usually in the range of 75% to 80%. And, that can make a world of difference in your later retirement years.

Your Social Security Statement Has Always Had This Information, But Did you Know?

Many people do not fully understand the value of their Social Security benefit. They think the dollars they contributed via FICA are theirs. And they want them back!

One thing I will say about this new statement is that the SSA left in an important detail. They do show you how much you’ve paid over your decades of work. And they include how much your employers have also paid during all those years.

Take a moment to consider the payback. In Wanda Worker’s case, she paid in $76,000. Her employers kicked in $77,000 over her 40-ish years of working and paying FICA. That’s an input into Social Security of $153,000.

If she waits until her FRA, she’ll get a monthly benefit of $2,000. That’s $24,000 the first year. Without assuming any COLA, all of the FICA-taxes-paid-on-her-behalf are returned in just 6.4 years. That is a very fast payback.

Yet, the odds of her living into her 90s are very good. And her Social Security checks will never stop arriving. Even decades after “her money” is long gone. That’s what a social insurance program is designed to do. Most of us don’t get our money back – we get 4-to-5-times our money back.

Take a Good Look at Your Social Security Statement Today

Regardless of this new statement design and all the missing critical information, it’s still a critical tool. The important piece is knowing you’ll have a safety net as long as you live.

Nearly 50 million Americans receive Social Security retirement benefits today. Another 15 million receive Disability or Survivor benefits. Spouses get their own checks even if they don’t have their own work history. Same-sex married spouses also get their own spousal benefits. Ex-wives and ex-husbands get extra benefits if they were low-wage earners.

The power is in the social insurance program itself. Your statement is access to your own information. And a reminder to dig for more. Here’s to making sure you get your account set up. Here’s to taking the time to understand your work history and how your benefit will be calculated. And we can only hope the next design of the statement will be greatly improved.

Read More Posts about Social Security

Make sure you are taking steps to protect your Social Security number <click here for the post>

Take a quiz to see how much you know about Social Security <click here for the quiz and answers>

For much more information about how your benefits are calculated, order your copy of my Social Security book – it’s for men too! <read more and order from this post>