Social Security benefits are the most important source of cash many people have for retirement. The checks won’t necessarily be your biggest source of income. But it is the very foundation upon which your financial success is built. You can think of this source of money like the foundation of your own house. Without strong and sturdy blocks of cement, your structure is unstable. So, knowing that Social Security is going to be this important, let me ask you a question. How much do you really know about Social Security?

Let’s take a deeper dive into this very important, yet highly misunderstood program.

But first, stop reading!

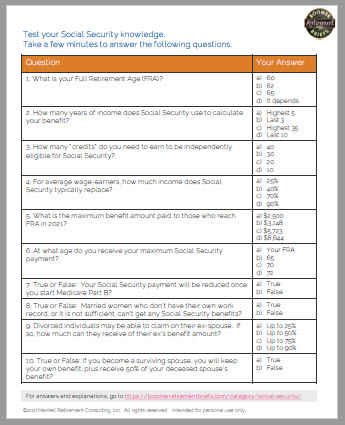

Before you continue in the blog, make sure you first download this quiz. Take a few minutes to read the questions and circle your best-guess answers.

When you finish, continue reading this post. I’m going to answer each of the 10 questions and give you a little more explanation.

Download your free copy of the quiz. See how much you really know about Social Security.

Social Security is a law

There are several parts of Social Security that easily trip folks up. But if you have a good basis of the general rules, it helps keep this program in perspective.

The first stumbling block is understanding that Social Security is a Federal law. That means it is wildly complicated. Even though it is for the best of intentions. Everyone’s situation will be different. The law accommodates virtually situation for you as a worker, a spouse, a divorced person, or a widow(er). Plus, there are family benefits available in some situations. And disability if you are one of the nearly 10 million who are unable to work due to health circumstances.

How much of my money do I get back?

The second area that makes people scratch their heads is why they don’t get back all their money. Or do they? For a vast majority of us, we get back all the money we’ve contributed over the years. And, we also get back all the money our employer has contributed on our behalf. Live a long time, and you get even more back. Accounting for average cost-of-living increases, you can easily get a cumulative benefit of a half million to more than a million dollars. You did not put that much into Social Security.

Keep in mind, the money you pay into the program goes right back out to pay current retirees. In turn, our kids will pay in for our benefits. It’s not that you have a special account with your name on it. Rather, you earn credits for making your FICA tax payments. Once you earn enough credits, you fully qualify for Social Security and also Medicare Part A.

Why doesn’t Social Security replace my income?

Last big issue is the following… How much of your income Social Security is meant to replace? Well, not much. From the very beginning, Social Security was designed and intended as a modest safety net. It’s been critical if you didn’t save enough money for your retirement.

Keep in mind, Social Security came about after the Great Depression in the early 1930s. Older Americans lost jobs and couldn’t find more work. Poverty was rampant among the oldest citizens. They were starving. Social Security provides limited protection for retirees and the disabled. It was never meant to replace your paycheck.

Time for some answers…

So, you’ve taken the quiz. How much do you really know about Social Security? Let’s find out.

Question 1

What’s your full retirement age? Answer is: d) it depends. Why? Your “Full Retirement Age” is a technical term that is based on the year you were born. This is the age when Social Security deems you retired. Whether you are still working or not doesn’t matter.

What does matter is that it is at this age when your full, unreduced benefit is available to you. Your Social Security benefit is a calculated benefit. If you claim it before your FRA, you lock in a permanent decrease in monthly payments. Claim after FRA, and up to age 70, and you’ll get higher monthly payments.

FRA is 67 for everyone born in 1960 or later. If you were born between 1955 and 1959, your FRA is 66 and some number of months. Find your exact FRA on this Social Security page.

Question 2

How many years of income does Social Security use to calculate your benefit? Answer: is c) your highest 35 years of earnings. Your exact amount of benefit is based on your own personal earnings record. Social Security will adjust all those early years for wage inflation, then it pulls in your overall highest 35 years.

If you’ve worked 43 years, that’s great. But, only your highest 35 years are part of your calculated benefit.

If you’ve only worked 27 years, that’s fine, too. Social Security still uses your highest 35 years of earnings. In this case, your calculation includes 8 years of zeros.

Question 3

How many “credits” do you need to earn to be independently eligible for Social Security? Answer is a) 40 credits. A credit is confirmation that you paid at least a minimum FICA tax in any given year. You can earn up to 4 credits per year.

During your career years, you must work at least 10 years, or 40 quarters, where you’ve been taxed on earnings. Some jobs do not pay into Social Security and instead have a pension. These jobs are usually in the public sector – fire fighters, police, State and Federal workers. It can also be that you have a union job with a pension in place of Social Security.

Question 4

For average wage-earners, how much income does Social Security typically replace? Answer is b) 40%. Again, we need to remember that Social Security is an insurance benefit. But the reality is many people want to know how much of their ending paycheck will be replaced with Social Security.

Social Security’s calculation provides a higher “replacement” percentage for those who are at the lower end of the pay scale, and a lower replacement for the higher earners. Most people fall into the middle.

Question 5

What is the maximum benefit amount paid to those who reach FRA in 2021? Answer is b) $3,148. And that includes anyone who made a lot of money throughout their career. Specifically, this person would have reached the taxable wage base all of their years of work.

Again, your benefit is calculated based on your own earnings history. Social Security FICA payments stop being pulled from your wages if you are a high-income person. Therefore, if you make a million dollars, that’s great. But in 2021, you stopped paying into FICA when your salary reached $142,800.

You can get a higher benefit payment if you wait to claim until after FRA. You get an 8% per year “bonus” up until age 70 if you choose to delay claiming your benefit.

Question 6

At what age do you receive your maximum Social Security payment? Answer is c) 70. Adding to the general confusion of retirement ages and birthdays, you maximize benefits the month you reach age 70. Waiting longer just leaves money on the table. Your money!

If circumstances work out that you can wait to claim, that is great. But only about 5% of all retirees wait to claim. While getting an 8% increase per year is an excellent return rate, the fact is, you aren’t getting 8% on a million-dollar portfolio. It’s your benefit amount at FRA that is increased 8% per year.

Let’s say you are on track for $2,500 per month in benefits at FRA. If you wait until 70, you’ll receive between $3,100 and $3,300. Your specific amount depends on your FRA. And, you’ll need to raid your portfolio or keep working until 70. After all, those bills have to be paid from somewhere.

Question 7

True or False: Your Social Security payment will be reduced once you start Medicare Part B? Answer is True. The Medicare and Social Security programs are closely knitted together. Once you are enrolled in both programs, your Part B premium will be automatically deducted from your Social Security payment.

It’s important that you plan for this. The Part B standard premium is $148.50 per person per month in 2021. And it typically increases each year. That is quite expensive for most retirees. However, the premium can be even higher.

You might have high income in retirement from large required minimum distributions or from continuing to work, for example. In those cases, your Part B premium can be between $207.90 and $504.90. Per person, per month. That’s in 2021. You can expect higher premiums each year in retirement. It’s important to adjust your Social Security estimates to account for automatic deductions to pay for your Part B.

Question 8

True or False: Married women who don’t have their own work record, of it is not sufficient, can’t get any Social Security benefits. The answer is false. Married women who didn’t work outside the home for wages still contributed mightily to the economic success of the household. Social Security recognized this situation and the law accommodates for at-home moms. And, now for at-home dads as well.

The lower-earning spouse is entitled to 50% of the higher-earning spouse’s calculated benefit. But she has to claim at her own Full Retirement Age to get this amount. Otherwise, she gets a reduced payment. Her benefit is paid as a separate check as her own benefit.

Question 9

Divorced individuals may be able to claim on their ex-spouse. If so, how much can they receive of their ex’s benefit amount? The answer is b) up to 50%. An ex-spouse who meets certain qualifications can receive the same benefit payment as if they were still married.

But the key is the marriage had to be a long-term marriage before the divorce was finalized. The Social Security rules are very specific when it comes to claiming on an ex:

- The marriage had to last 10 consecutive years or longer;

- Each of the ex-spouses has reached age 62;

- The divorce was finalized at least two years ago, or the ex is already claiming;

- The spouse claiming on the ex cannot be married; and

- The amount of the benefit on the ex must be higher than their own benefit.

It’s all a bit complicated. But there is often good news. Many lower-earning ex-spouses will receive a higher benefit than they thought.

Question 10

True or False: If you become a surviving spouse, you will keep your own benefit plus receive 50% of your deceased spouse’s benefit? The answer is false. However, most people think this is how the survivor benefit works.

In general, it will help if you remember one general rule. There is only one benefit paid to any individual at any one time. So, while both spouses are alive, he gets one benefit and she gets one benefit. When the first spouse dies, there is only one individual left. That person will get only one benefit. It will be the higher amount between the two payments that were coming into the two-person household. The lower payment is dropped. The higher payment is paid to the survivor.

So, How Much Do You Really Know about Social Security?

Did you score well, in the 9 or 10 range? Or, were you surprised by your incorrect answers? No need to worry if you got only a few correct. The real point is that Social Security is riddled with rules and regulations. It is a massive law that attempts to accommodate each and every person’s unique situation.

The key is to spend plenty of time analyzing your personal benefit. Then, coming up with the best strategy for your claiming benefits. Think about the near-term implications and the long term. And, if you are married, it’s especially important to consider how your benefits will or won’t support your spouse if you die first.

Let me know what you’re thinking for your own claiming strategy. Or if you have questions, send me a note. I’d love to hear from you.

For More Information

You’ll find some additional interesting information from the Center on Budget and Policy Priorities.

And, if you want more on why Social Security is not going bankrupt, read my blog “When is Social Security going bankrupt?”

Make sure you set up your my Social Security Account. That’s where you’ll get your most current statement and other good information about the program.