There are some 45,000,000 retirees collecting Social Security retirement benefits today. More than half of these folks decided to claim their benefit before their Full Retirement Age or FRA. In fact, 52% of men pushed the “grab-and-go” button well before Full Retirement Age. And, nearly 59% of women did the same. Full Retirement age is the age considered officially “retired” by the Social Security actuaries. As a result, every one of those 25 million retirees got a penalty. They locked themselves into permanently reduced Social Security income for their retirement years.

To be fair, some truly needed this income to stay afloat. But, many others just couldn’t wait to get their hands on the money. They thought Social Security solvency was going to be a problem. So they took their money before it was too late.

A Classic Financial Dilemma

This is a classic financial dilemma of emotion and lack of facts wrestling rational thought to the mat, and winning.

Social Security solvency is a big topic, but the facts are deeply buried in today’s media hype. The result is that people get scared and decide to claim early, “just in case Social Security goes broke.” Sadly, they haven’t done the research, explored the balance sheet, or read and evaluated the Trustee’s Report. They claim as early as possible to get monthly deposits rolling in.

You Are Not Alone

You are not alone if you are concerned with Social Security solvency. Several surveys over the past 3 years show the same unfortunate results. Fifty percent of Boomers are concerned Social Security will not be there throughout their retirement.

There is good news here: the other 50% are confident it will be around. It will take political and financial pressure, combined with discipline and fortitude, to address the situation. And strengthen the program for the next 75 years. There is time to do just that.

How Social Security Gets Funded

The creators of Social Security in the 1930’s did a remarkable job developing a viable system meant to last. In 1940, the OASI (Old Age and Survivors Insurance) Trust Fund was established as a separate account in the US Treasury Department. The Trust Fund maintains and invests the surplus between net income and costs to run the program. There was a 3-pronged funding system to ensure Social Security solvency and the OASI Trust Fund.

1. Payroll taxes, required by law for funding Social Security;

2. Interest on the investment of the Trust Fund reserves; and,

3. Any General Fund reimbursements.

Far and away, Social Security was set up as a “pay-to-play” program. Designed for workers to pay their share while working so they could reap benefits when they retire.

Social Security Solvency Crisis

Between 1975 and 1983 the Trust Fund was “going broke.” It ran a deficit each year as outflows outpaced inflows. It was during Ronald Reagan’s presidency that Social Security solvency became a crisis. Part of the solution to shore up the system was to create a new funding category to support the system. Specifically, Congress started taxing Social Security benefits. (Many other amendments were enacted during this time as well, including changing the retirement age to 67 over time.)

The Magic Ratio for Social Security Solvency: Workers-to-Retirees

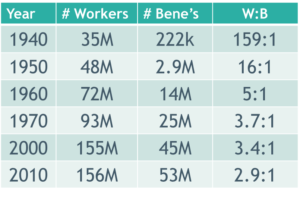

Back in 1940, there were more than 150 workers paying into Social Security for every retiree taking his or her benefit. Today, the ratio is less than 3-to-1. To meet monthly payments to all 45 million retirees, the SSA had to once again tap the Trust Fund. It’s estimated that 2018 will be the first year the Fund runs at a deficit since 1983.

With all the usual disclaimers that I am not the Queen Bee of Social Security; I’m not a member of Congress; nor, do I possess special powers to see into the future, I am highly confident that Social Security will be here for us Baby Boomers. Before you consider claiming your well-deserved retirement benefits too early, spend some time reading. It’s important you know the facts supporting Social Security solvency. And equally important you understand the consequences of an early claim.

Chop Your Estimated Benefits by 25%

Once you’ve seen your own estimates, chop them by 25%. Why? Because even if nothing is done to shore up Social Security, benefits will be cut. It’s estimated the payroll taxes from current workers will provide about three-quarters of our Social Security benefits. As a result, you’ll get an income from Social Security. But it won’t be as generous as the most current approximations. However, running at a deficit does not mean the Trust Fund is “broke”. At least not yet!

A Good Place to Start: “Do I believe Social Security will be there for me?”

This is the most important question you can ask yourself. Like many, you may have formed strong, specific perspectives and beliefs about the viability of Social Security and its solvency. This mindset can be a positive force, or one that you might want to reconsider. It’s important as you think about how you will create a paycheck in retirement to get a good handle on the inner workings of the Social Security system.

If you believe in Social Security solvency and that the funds will be there for your retirement income, that’s great. Keep current by reviewing your most recent Social Security statement and run your projections using the calculators on SSA.gov. You might also find it helpful to discuss your options with a financial advisor who is well-versed in the nuances of Social Security solvency, how the program works, and retirement income planning overall.

Or, “Do I believe Social Security will NOT be there for me?”

On the other hand, if you believe Social Security is on the brink of disaster and you’ve set your sights on claiming at age 62 no matter what, then you’ve additional analysis to do. Before you pull that irrevocable trigger, I strongly suggest you read the Trust Fund report. I know…it’s 270 pages long. So, hunkering down and reading it is a stretch! But, if you read only the summary on pages 1 – 5, you’ll get most of the information you need to make a well-informed decision.

What you might find even more interesting is how the Trust Funds work. You can read a brief (2-page) article from the Center on Budget and Policy Priorities. It’s called Policy Basics: Understanding the Social Security Trust Funds. I think it will give you a good start, as will their short article on what the 2018 Trust Fund report really tells us.

If you aren’t going to read these riveting reports, suffice it to say that Social Security is set to last in its current form until around 2034. If Congress moves sooner to strengthen Social Security solvency, the program should last for another 75 years into the future.

What You Stand to Lose When You Claim Early

The claiming decision around Social Security is critically important because it sets the foundation for your paycheck throughout retirement. Those who claim early, regardless of the reason, run into four landmines.

Locking in a 25% – 30% pay cut.

It’s important to understand that you are entitled to a specific monthly income amount and an overall lifetime benefit. When you claim early before your FRA, the assumption is you’ll live just as long as if you had waited; therefore, your lifetime payment has to be spread over more years. So, you’re locking in 25% to 30% less in monthly income from Social Security, and you’ll be drawing down more of your own money at a faster rate.

Leaving the lower-earning spouse with a lot less income.

Let’s assume you are married and the higher earner . Your Social Security payment is more than your spouse’s. If you die first, your surviving spouse stops receiving her or his check. They will step into your shoes, receiving your higher Social Security benefit. If you claim early, you’re ensuring your spouse will get the least income from Social Security when you’re gone.

Deferring monthly income.

Have you heard of the earnings test? It’s a comparison of your wages versus a limit on the income you can receive once collecting Social Security benefits. When you claim Social Security before your FRA, you are assumed to have retired. If you continue to work, logically, you aren’t retired! You can “dabble” and earn some income. But it can’t exceed about $1,400 per month (indexed for inflation). If you earn more than that amount, your Social Security benefit is clawed back. This means you will not receive payments from Social Security. You’ll miss out on months of benefit checks. Not forever. Just until you reach your FRA when the SSA will recalculate your benefit amount.

Paying more in taxes.

Social Security benefits became part of a retiree’s taxable income in 1984. There is confusion about how much is taxable, so you’ll need to use the worksheet in IRS Publication 915 to see your taxable Social Security income. Bottom line: if your retirement income exceeds $44,000 for married couples and $34,000 for individual filers, as much as 85% of your benefit will come onto your IRS 1040 form as taxable income. Plan accordingly!

Do You See Social Security Solvency as a Glass Half-Full or Half-Empty?

Just because this incredibly important program needs a tune-up doesn’t mean you should make short-range decisions. You stand to damage your retirement income or run out of assets too soon. Common sense says that few employers, if any, will hire anyone who’s run out of money at age 80!

It’s critical to get your arms around how Social Security works to create a retirement income plan that allows you to see how, where, and when your retirement “paycheck” is going to show up and where it comes from. If you don’t have any Social Security income, how will you make up 20% to 40% of your income with just your own savings?

Create Your Retirement Income Plan

Social Security will be around. It just might pay each of us less than we were hoping for. So, understand the program and plan for your long-term retirement paycheck. You’ll see how it all works in your retirement income plan. Have you created your written retirement income plan? Whether you see the Social Security glass as half-full or half-empty, it’s time to start.

For more information:

Review some of my blog posts and resources to help you better understand some of the workings of Social Security and where to get good information before you decide when to claim.

- Check out my Social Security Scavenger Hunt to help you find your way through the website

- Read about the 4 Claiming Strategies and see which category you fall in today.

- If you don’t have a financial advisor, this checklist might help you find one. Make sure you ask him or her about their expertise with Social Security.