Example Cases to Check out

Social Security decisions for married couples are best approached step-by-step. Then the rules make more sense. There are several “behind-the-scenes” calculations that you don’t see on your statements. Different options are compared to see if either spouse will be eligible for a spousal benefit. At the end of the process, each spouse will receive the highest benefit for which they are eligible. In this post, Social Security for Married Couples – Part 2, we’re diving into the math. Let’s build on the first post and explore how real couples need to consider their options.

Meet Sally and Richard in Social Security for married couples – part 2

Let’s visit my favorite fictional couple, Sally Snowflake and Richard Raine. They have been happily married for 40 years. (You can be married for one year to qualify for spousal benefits.)

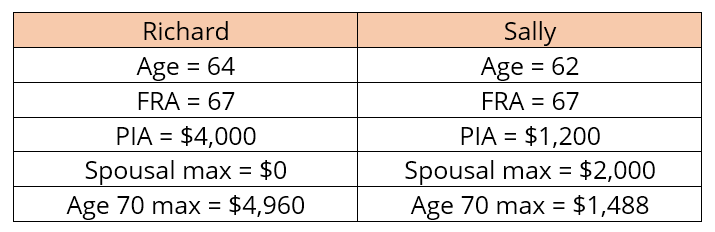

They are now in their 60s and thinking about Social Security. Each pulls their Social Security statement from their online mySocialSecurity account. Here’s their basic information:

A reminder about the shorthand you’ll find in Social Security:

- FRA is Full Retirement Age. It’s 67 for most people today, but it depends on the year you were born. It is no longer 65 for anyone.

- PIA is Primary Insurance Amount. This is a dollar amount calculated for each worker based on their highest 35 years of earnings as of their FRA.

- Spousal max is the spousal maximum. This is 50% of the higher-earner’s PIA. A lower-earning spouse may be eligible for an additional benefit if their PIA is less than 50% of the higher-earner’s PIA.

Analyzing Richard’s situation

Richard is the higher earner and receives the larger benefit. If he waits to claim benefits until his FRA of 67, he’ll receive $4,000 in gross benefits. If he claims before 67, the amount he receives will be reduced.

His decision carries twice the weight it would if he were single. First, his benefit needs to provide as much monthly cash flow as possible while they are both alive. Second, the amount Richard receives will ultimately become the survivor’s benefit. Regardless of which spouse dies first, Sally’s lower monthly benefit will stop, and Richard’s higher benefit will continue.

So, you can already see here in Social Security for married couples – part 2 how Richard’s claim will affect their financial situation. It matters for early retirement and later in life. Richard’s claiming age is a critical financial decision for them.

Considering Sally’s situation

Let’s now look more closely at Sally’s situation. She worked for many years, earned 40 credits, and has a PIA of $1,200. If she claims at age 67, her FRA, she’ll receive the full $1,200. If she claims earlier, she’ll lock in a reduced benefit. But that is her benefit. It is based on her work history and paid directly to her.

Because Sally is the lower-earning spouse, Social Security will look at her spousal benefits. When they compare her own benefit to the maximum spousal benefit, they’ll see a gap. Half of Richard’s PIA is $2,000. Her own PIA falls short of $2,000, so she should receive a spousal benefit.

Sally will be eligible for an additional spousal top-up. If she claims at her FRA, she’ll receive her full $1,200 plus an additional $800. This way, she receives her spousal maximum. It just comes in two parts.

But timing is important here.

Once she claims her own benefit, she automatically claims her spousal top-up at the same time. However, she might not yet receive her spousal top-up payment. This is known as “deemed” filing. A lower earner is deemed to claim all benefits at the time of their initial filing.

Sally cannot decouple her claim and ask for only one of her two benefits. It’s all or none.

She’ll receive her own benefit when she claims initially. But until Richard turns on his benefit, Sally’s top-up is unavailable. There may be different start dates for her two benefits, but she will eventually receive $2,000 per month. Assuming she claimed her own benefit at her FRA.

What if Sally didn’t have her own PIA?

Many wives do not qualify for Social Security on their own. More husbands in younger generations will be in the same boat. Here in Social Security for married couples – part 2, we’ll look at what happens to a fully “dependent” spouse.

If Sally never accumulated 40 credits to earn her own benefit, she is still eligible for 50% of Richard’s PIA. But only when she reaches her own Full Retirement Age of 67. Otherwise, she’ll get a reduced spousal benefit.

If Richard is already claiming when she reaches 67 (he would be 69 by then), her full spousal benefits are available. She’d receive her full $2,000 spousal maximum on his record.

However, if he’s waiting until 70 to collect and maximize his higher benefit, she must also wait to claim spousal benefits. She would be 68 before spousal benefits become available.

And if Richard decides to claim before his FRA, say at age 65, Sally has a decision to make. Will she also claim early, at age 63, and accept a steep reduction in monthly benefits? Or might she decide to wait until her own FRA to reach the $2,000 per month?

And, if Sally’s PIA is higher than $1,200?

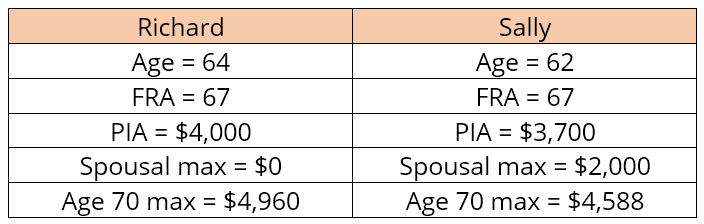

Let’s now look at how spousal benefits work for many married couples today. Both spouses had long careers and earned higher incomes. In this example, Richard still has the higher PIA, though not by much:

The spousal maximum is still calculated behind the scenes. It remains at $2,000, or half of Richard’s PIA. Then, the lower earners’ benefits will be compared—her own PIA ($3,700) versus the spousal maximum ($2,000).

In this example, Sally’s $3,700 PIA is well above the $2,000 spousal maximum. Therefore, she is not eligible for spousal benefits. Her Social Security benefit will be based on her own strong work history.

How much she can collect depends on her age when she claims. If she claims at 62, she’ll lock in a 30% reduction in benefits, lowering her monthly payment to $2,950. She cannot make up any difference with spousal benefits. She may also choose to wait until age 70 to fully maximize her cash flow.

Nuances of the Social Security law

The bottom line: Just because you’re legally married doesn’t mean you receive spousal benefits!

Further, the nuances of the law can make the decision when to claim even more challenging. For example,

- If you claim before FRA and keep working, you might not receive any monthly benefits. If your income is too high, your benefit payments will be temporarily clawed back. You won’t pass the earnings limit test. In 2026, if you are younger than FRA for the entire year, you cannot earn more than about $25,000. These clawed-back benefits are added back into your calculated benefit once you reach FRA.

- Unbeknownst to almost everyone, when you claim Social Security, you are automatically enrolled in Medicare Part A. If you were funding a Health Savings Account, you need to stop making contributions. Once any part of Medicare is active, HSA contributions are no longer allowed.

- Social Security benefits are generally taxable income. Up to 85% of the gross amount is reported as “income” on IRS Form 1040. For married couples, you’ll report between 50% and 85% of your benefits as income once your combined income exceeds $44,000. Combined income is your Adjusted Gross Income (AGI) plus any non-taxable interest plus half of your Social Security benefits. See IRS Publication 915 for more details.

The most important step you can take

This is often the most overlooked step when deciding when to claim benefits: talking to each other. In our early 60s, we’re often still very busy with demands at work and at home. So it’s especially important to start talking early. About retirement, if you’re going to retire. And about how to best take advantage of Social Security for each of you.

Remember to download your free checklist from part 1. It’s a good place to start the conversation.

After all, you’ve made it this far in your marriage. You may as well plan for the happily ever after to last another 30 years or longer.