Key information and a checklist before you claim

Are you happily married today? You’ll probably need to keep that in mind when you sit down to figure out your Social Security claiming strategy. There may be a healthy debate over who will claim first. And it may be hard to consider how your decision could affect your spouse after you die. Not such a pleasant topic. But super important. Let me encourage you to read on for important information specifically about Social Security for married couples.

Social Security for married couples works differently than you might expect

Social Security is an individual benefit. It became a law in 935, signed by Franklin D. Roosevelt. You’ll see that it clearly reflects the culture and beliefs at the time. One example is that Congress was very clear that a social insurance benefit must be based on a worker’s wage history. This was not going to be a handout or a welfare program.

Another is that in 1935, most women in the middle and upper classes didn’t work outside the home. Rather, they married, raised the couple’s children, and ran the household. Lower-income families relied on the wife’s outside income to make ends meet. She often worked in jobs that did not have “covered wages.”

Instead, she worked as a housekeeper, farm-hand, or in personal services. Those employers were exempt from contributing to Social Security. Therefore, she would have no earned wages on which to calculate Social Security benefits.

The net effect of Social Security on married couples’ benefits was therefore based solely on the husband’s income and wage history. However, Congress recognized that women also contributed to the household’s economic success.

As such, wives should also receive a Social Security retirement benefit. Originally, the law identified such benefits as “Wives’ Benefits.”

Wives’ Benefits continue today, but are now available to husbands too

But how much wives received in benefits wasn’t necessarily ideal. A wife could receive half of her husband’s Primary Insurance Amount, or PIA, once she reached age 65. (PIA is the calculated benefit each worker is eligible for when they reach Full Retirement Age.) That was the retirement age from the 1930s through the early 1980s. Simply put, if his benefit at age 65 was $400, she would receive $200. And less if she claimed as early as age 62.

During this era, most husbands worked outside the home and built a wage history. There was no provision for “at-home” husbands or dads until the 1970s.

Thanks to an important case argued by Ruth Bader Ginsburg, some lower-earning husbands now receive spousal benefits. Other husbands work in public-sector jobs and don’t meet the requirements to earn their own Social Security benefits. They typically receive a public pension rather than Social Security and haven’t earned the 40 Social Security credits required.

In these cases, he may receive up to 50% of his spouse’s benefit once he reaches his Full Retirement Age (FRA).

Interestingly, these aren’t called “husband’s benefits.” They are just called spousal benefits. The old-fashioned term “wives’ benefits” has been replaced in the law.

Having a legal marriage is key to spousal benefits

Furthermore, any legally married spouse may be eligible for spousal benefits. This means that same-sex married couples are treated equally for spousal benefits.

A few states still recognize “common-law marriages” without a legal document. But partners must prove that they were living as if legally married. If this is your situation, it’s best to do some research in advance. Make an appointment with your local Social Security field office. Or consult an attorney in your state to make sure you can claim spousal benefits. NOLO offers a good article as a place to start.

In some cases, long-term partners who aren’t legally married may be considered spouses. This is a gray area, but worth discussing with Social Security if this is your situation. And with an attorney who specializes in this area of family law.

Who gets spousal benefits?

To the disappointment of many spouses, only the lower-earning spouse has the potential to receive any spousal benefits. And not all lower-earning spouses will qualify. In your marriage, one of you may have a Primary Insurance Amount (PIA) three times larger than the other. Other times, you’ll both have similar PIAs. It all depends on each spouse’s work history and wages earned over the decades.

Let’s first take a look at the general rules for spousal benefits:

–Lower-earning spouses are eligible for a benefit equal to 50% of the higher earner’s Primary Insurance Amount (PIA). The higher earner’s PIA is their calculated benefit at their Full Retirement Age (age 67 for most).

–If any spousal benefits will be paid, the lower earner’s own PIA must be less than 50% of the higher earner’s PIA.

–No spousal benefits can be paid until the higher earner has claimed their benefits. Married couples got hitched at least one year ago. And now your Social Security benefits are hitched together as well.

–If the lower earner claims before their own FRA, they’ll receive less than 50%. The reduction (aka, penalty) for claiming early is steeper for spousal benefits than for one’s own benefits.

Social Security for married couples gets even trickier

If you are the lower-earning spouse, how will you know whether you’ll receive a spousal benefit? Keep in mind that being a spouse doesn’t guarantee any spousal benefits.

These are the typical cases where spousal benefits are paid to the lower earner:

- The lower earner has no wage history of their own. In this case, they are eligible for the full 50% of the higher earner’s PIA when claiming at their own FRA. This applies to an at-home mom or a spouse who worked in the public sector.

- The lower earner worked for some years, but not long enough to qualify for their own benefits. They did not pay into FICA for at least 40 quarters.

- The lower earner has their own earned benefit and may receive a spousal “top-up.” This is an additional payment added to their own benefit. Together, the lower earner’s benefit and the spousal top-up will total 50% of the higher earner’s PIA.

Again, it’s important to understand when the lower earner receives 50% of the higher earner’s PIA. That only happens if the lower earner claims at their own FRA. If they claim before age 67, benefits are reduced.

This is crazy! What exactly do these rules tell me?

Are you shaking your head as you read these rules? I know I did…for the first 20 times I tried to figure all this out. Using examples is a better way to understand the various ways spouses might be eligible for spousal benefits. Turns out, it’s not as complicated once we put some numbers in play.

For more detailed examples, jump to Part 2 of this post. There you’ll meet my favorite fake couple, Sally Snowflake and Richard Raine. They have been happily married for 40 years. (You only need to be married for one year to be eligible for spousal benefits.)

Or read about other married couples in my latest Social Security book—Social Security: Lightly Toasted, Not Burnt. It’s available on Amazon and Barnes & Noble in paperback and e-book formats.

Other considerations with Social Security for married couples

Once you run the numbers, the results often point individuals toward one claiming direction: You’ll get more if you wait until age 70 to claim. Note that only 10% of all retirees wait until age 70 to claim.

But when combining two people’s situations to optimize or maximize benefits, things become more complicated. It’s common to find that only the higher-earner might want to wait until 70 before claiming. The lower-earner might be better off claiming before FRA. You need to do the math!

Adding to the complexity is the fact that most people have a strong point of view about Social Security. About the program itself. And whether they think the money will be there for their retirement years.

They also have strong opinions about when they want to start getting what’s theirs. By their early 60s, many people are more than ready to quit working. But leaving a paycheck behind is financially difficult. Their plan is to start Social Security. Even if it means taking a reduction in benefits.

It’s not so easy to take all the emotion from the decision. Married couples are not always the most rational human beings!

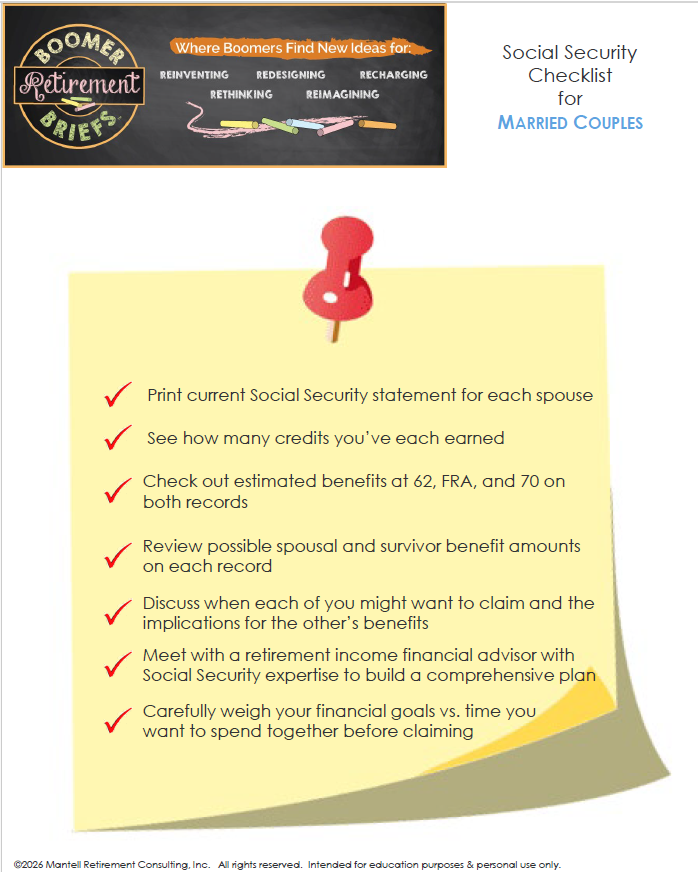

Download your Social Security for married couples checklist

There are many rules and extenuating circumstances to consider before either spouse files a claim. Before worrying about all the ins and outs of the law, it’s probably best to step back and gather the basic information you need.

- Start by downloading your most recent statement. Review the monthly benefit amounts you’ve earned.

- Talk to each other about retirement plans and possible retirement dates.

- If you’re ready to stop working, figure out whether there’s a viable way to delay claiming Social Security until FRA or later.

To help you get started figuring out your own situation, download this free checklist: Social Security for married couples.

It will help guide your thinking and decisions about this incredibly important part of your retirement income

Also, keep in mind that we’re at an important juncture for the Social Security trust fund. You’ll want to better understand what could happen if Congress continues to drag its heels. In short order, benefits will be reduced about 23% for everyone. This one “wrinkle” makes your decision when to claim even more important.