A $0 monthly premium should be a clue

Are there really any advantages to Medicare Advantage plans? Over 50% of retirees on Medicare have assigned their benefits to a private, for-profit health insurance company. I can assure you, these 32 million people have no idea what they’ve signed up for. But they think a zero-dollar monthly premium is a great advantage. But is a Medicare Advantage plan right for you? And how can you make such an important decision?

Just the facts, ma’am. Medicare Part C Is Medicare Advantage

Medicare Part C plans are part of the extensive Medicare law. They are essentially insurance-in-a-box for older Americans who are eligible and enrolled in Medicare. These all-in-one insurance plans were created as a pilot program under TEFRA in 1982. Today, all the big guys offer these plans. They go by the acronym BUCA: Blue Cross, UnitedHealthcare, Cigna, and Aetna.

For the past 150 years, these BUCA insurers have controlled the vast majority of the healthcare insurance market. They provide insurance (and a bunch of other stuff) for employees, retirees via Medicare Advantage/Part C, union members, and even veterans. Plus, they offer Medigap supplemental plans.

Part C plans have evolved over time. When they were first introduced, they were called Medicare+Choice plans. With these plans, you got the same coverage as in Medicare Parts A and B. Plus some cost sharing for dental, vision, and hearing. Those healthcare services are specifically prohibited from original Medicare. Insurers thought they’d make some extra profits by offering a little more to older Americans.

You can see the complete range of plans offered on Medicare’s website.

What started out as a simple option has ballooned into complexity

Part C plans are a packed plan offered by the BUCA private insurers and others. You choose the type of Medicare Advantage plan that works for you. Your decision will be based on your comfort sticking to a network. Are you willing to get your healthcare within a limited number of doctors and facilities? Think about that as you consider life and health in your 70s, 80s, and 90s.

The more limited network means a lower monthly premium. But which kind of Medicare Advantage plan is right for you? How should you analyze the two main Part C options available today?

The original Medicare Advantage (MA) plan was a Health Maintenance Organization, or HMO. Under this plan, all your healthcare services are provided within a local network. This arrangement works well for the insurer, as they can control costs better.

But older folks didn’t always like the restrictions of a network. Sales of MA plans stalled, and more Medicare retirees chose the highly flexible Medigap plan. They were willing to pay a monthly premium to see any doctor anywhere. The insurers responded with Preferred Provider Organizations, or PPOs. These MA plans offer more flexibility for you to go in and out of network.

Aren’t Medicare Advantage Plans Free?

In a word, no. With most HMOs and many PPOs, the monthly premium is $0. However, you’ll pay your Medicare Part B premium. ($174.70 in 2024 or more.) There are no additional monthly premiums paid to the MA insurer.

But, and this is a huge but, you will pay for each individual service you use. Every MA plan has a very detailed plan document with cost information. You’ll pay a particular dollar amount for a particular service. Or you’ll pay a stated percentage of the cost of care.

Surprising, you’ll pay these fees until you reach the annual out-of-pocket (OOP) cap. CMS—the Center for Medicare and Medicaid Services—oversees MA plans and sets rules. They set a cap on how much older Americans should pay for in-network and out-of-network services. If you decide a Medicare Advantage plan is right for you, you’ll need to budget for your cost exposure. And the numbers are high:

- In 2023, the OOP cap for in-network services is $8,300 and $12,450 for combined in and out-of-network use.

- In 2024 the OOP cap for in-network services is $8,850 and about $13,300 for in and out-of-network use.

How much should you budget if a Medicare Advantage plan is right for you?

I’m big on budgeting and making sure I know how much of my hard-earned life savings will be spent on healthcare in retirement. But getting my arms around the not-free MA plans has been a challenge.

If you choose a Medigap plan, you know the monthly premium. And you know you won’t pay any bills or copays when you use the healthcare system. Unless you use something not covered by Medicare.

However, with a MA plan, there is no way to know how much you’ll spend. You only know the maximum you can spend.

In an attempt to get some idea about how much to budget, I called one of the BUCAs in Massachusetts. It was a frustrating call. They do not have any general information about costs. The representative insisted I had to know what the doctor or surgeon was going to do. And if it was an in-patient or out-patient procedure. I simply wanted to know how much to budget.

The representative’s only response? Go through the plan document and estimate my own costs. The document is 286 pages long!

Making my own best guess at Medicare Advantage costs

Well then. I’ll just do that. When I get mad, I jump into action. So, I dug through that darned PDF to try to figure out what I’d be charged if I had a MA plan. Here’s what I found. (Though I have no idea if I’m really right.)

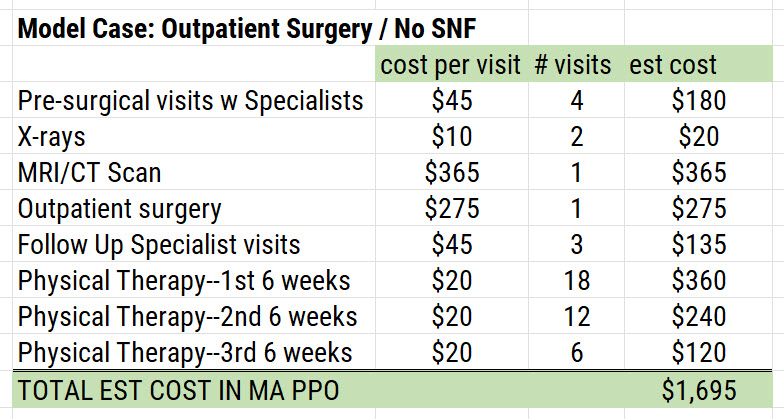

If I were getting an outpatient knee replacement surgery, the course of treatment might look like this. The costs are right from the handy-dandy 286 page document.

Wow. That’s one expensive knee to have replaced. Of course, I have absolutely no idea how close I am to what I will pay. None of the insurance customer service folks can help.

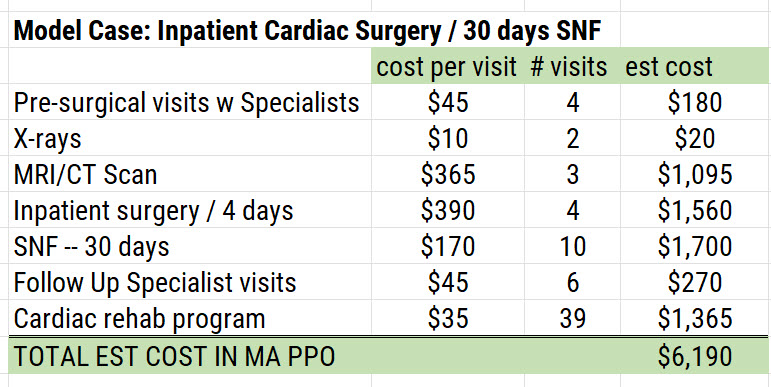

While digging through the document, I found a different category if you have a cardiac need. So I pulled together an example if someone needed heart surgery. Plus 30 days in a cardiac skilled nursing facility (SNF). Here are those cost estimates:

In this case, the actual OOP maximum may be less than $6,190. So this person may only pay, for example, $5,500. But they would reach the cost cap that year.

Deciding if a Medicare Advantage Plan is right for you is not so easy

Besides the fact you can’t budget for anything, there are many other questions you should ask before signing away your original Medicare to an insurance company. And a network. Plus a lot of restrictions.

Here are my top 10 questions everyone should ask before signing on the dotted line.

Q1: Have you read the plan document for your MA Plan?

The long and unclear documents are readily available at each insurance company’s website. Settle back and take the time to peruse nearly 300 pages. And be prepared to do this every year you are in a MA plan.

Q2: Are your drugs covered in the plan you want?

You don’t buy a separate Part D prescription drug plan if a Medicare Advantage plan is right for you. Drugs come wrapped in the package. Make sure yours are covered.

Q3: What happens if you end up in the hospital? Or need surgery?

As shown in the above examples, it’s almost impossible to know how much you’ll pay. If you have a hospital stay, you’ll front the costs for the first 4 or 5 days with a MA plan. If you have original Medicare A and B plus a Medigap, usually, you’ll pay nothing for the first 60 days.

Q4: Do your doctors and specialists take your MA Plan?

They don’t have to. You need to check when you enter a MA plan. And every year thereafter.

Q5: If you want to switch from MA to original Medicare, can you really do that?

Not really. You can quit your MA plan and restart your Medicare Parts A and B. However, it is unlikely you can buy a Medigap plan. Those trying to switch are generally older and sicker. They need and want more flexibility.

In most states, insurance companies can (and do) deny access to a Medigap policy years into Medicare. Or they charge significantly higher rates. After all, you were the one who decided a Medicare Advantage plan was right for you.

Unless you live in Massachusetts, Connecticut, Maine, or New York, it’s unlikely you will be eligible to add a Medigap.

Q6: How much do you like to fight with insurers?

When you are 78, 84, 92, will you be willing to advocate for yourself if a treatment gets denied? Or a surgery get delayed?

Remember, in a MA plan, the insurer makes the final decision. Someone who knows nothing about you decides if you can have that surgery or not. That’s what preauthorization is all about.

But you can appeal the decision. Really? When you are old and sick? Seems like a tall order to me.

Q7: Are you willing to fight for your doctor’s Rx recommendation?

MA private insurers place hurdles in front of a lot of different drugs. While you want to get better, the insurer wants cost savings. You should plan to jump through hoops to get many prescriptions if you end up with chronic diseases.

Q8: Will you have enough money to pay for expertise outside the network?

HMO members get their care inside a local network. They choose a Primary Care Physician who will make all referrals to specialists in the network.

If you would rather go outside this network, you’ll need to write a big check. Healthcare professionals outside your network are under no obligation to see you. And your HMO will not cover any of the costs. This one’s on you.

If you have a PPO, you may go out-of-network. But you’ll need to get approval from the specialist you want to see. And you’ll pay more.

Q9: Can MA plans be canceled?

Yes. And you’ll have 60 days to get into a new plan. Keep in mind, the new plan may not cover all your prescriptions. And your doctors, specialists, or hospital may not be part of the new network.

Sadly, this health insurance situation can happen at any time. Even when you’re 82, 92, or 102. Buyer beware.

Q10: How much should you set aside if you get really sick?

As you saw in the examples above, getting sick or injured can come with a hefty price tag. Cancer treatments, dialysis, and other treatments for chronic illness can run up to the out-of-pocket maximum for several years in a row.

It’s probably a good idea to create a reserve “bucket” of cash to pay these out-of-pocket maximums. If you have a Health Savings Account, HSA, that might be the answer. Or if you have millions already saved for retirement, you’re probably fine.

Deciding if a Medicare Advantage Plan is right for you takes some research and homework

Everyone needs health insurance. Once you turn 65, you are now in Medicare land. And it’s complicated.

Each individual is on the hook to make their own decisions. It’s going to take some time to do your homework. Looking under the hood of MA plans means digging through the plan documents. Estimating your costs means creating some scenarios.

You can do it. It’s not as hard as it may sound. But you need a lot of time. You have to get used to the tools. And read. There is a lot to read.

Start with these resources as you explore if a Medicare Advantage plan is right for you:

Medicare.gov has a “Find Plans” tool. It’s a good place to start.

Start pulling together your costs with my Medicare worksheet.

Good luck and let me know if you have any questions along the way.