Healthcare costs in retirement go way beyond “Medicare”

Medicare. Medicare. What the heck? How can a program designed specifically to help our oldest Americans be so incredibly difficult to use? Why are there so many pieces and parts? What’s with Medicare not covering all healthcare costs retiree need? And what drives those high Medicare costs?

In short, how is it that Medicare costs are only part of the overall costs retirees will spend in retirement? And not necessarily the highest costs in the healthcare budget?

Medicare Is a Law

Probably the most important part of this story about health insurance for retirees is to know that Medicare is a law. In fact, it is a gigantic law taking up several thousand pages. Technically, the Medicare law sits under the Social Security Act. Social Security was signed into law in 1935. Medicare in 1965.

Underlying this connection is the way the two programs are funded. Both Social Security and Medicare Part A are funded with FICA taxes. Since there was already a mechanism established for employers to pay into Social Security, it was simple to add Medicare to the process.

As a non-lawyer, I am always struck by the incredible level of minute detail written into retirement laws. In the case of Medicare, the law specifically lays out details like

- How hospitals can charge Medicare for payment.

- When Part A’s coverage starts and how far back the retroactive period goes.

- Which drugs are considered Part B drugs vs. Part D drugs.

- The type of procedure for cataract surgery that is eligible for Medicare reimbursement.

- That dental care, costs for vision and hearing, and podiatry are excluded from payments by Medicare.

- And on and on. For thousands of pages.

Medicare Costs Are Baked into the Law

In addition, how Medicare Part B costs are calculated and allocated between the players is baked into the law. Without going into the details, here are a few examples:

- The law defines what is included as the base cost amount and the actuarial rates for Part B.

- The specific formula used to calculate the Part B premium.

- Why and how there is a $3.00 repayment added to the premiums from the great recession.

- The percentage each beneficiary is expected to pay—25%.

- How higher-income retirees have a different share of the base cost to cover.

If you want to see the fascinating details about the law for calculating Medicare costs, check out the Federal Register. It is issued and updated every year.

Biggest Medicare Cost Surprises for Retirees

One of the more shocking parts of Medicare costs is how high-income retirees must pay more for their Part B premium. As written clearly in the law, higher-income folks do not pay 25% of the base cost. Rather, depending on their income from two years back, they will kick in: 35%, 50%, 65%, 80%, or 85% of the Part B base cost.

There are the IRMAA tiers—Income Related Monthly Adjustment Amounts.

Equally surprising is the IRMAA tier you fall into can (and often does) change year over year. Unbeknownst to most is that Part B premiums are recalculated by Social Security every year. In October or November, just after the Social Security COLA is issued. Your income in retirement will not be the same each year.

One year you may have “income” that pushes you into a higher IRMAA tier. The next, you are in a lower tier. And many married couples need to plan for a bigger surprise. When the first spouse dies, the surviving spouse becomes an individual tax filer. They may well jump several IRMAA tiers in the following years. That’s because the survivor usually receives about the same income, but now falls into different income brackets with higher tax rates to deal with.

It all depends on all the factors that make up your income on the front of the 1040. And every year is different in retirement.

Yes, You Have Income as a Retiree

Most people think of “income” as W-2 wages. Or, as self-employment income. Therefore, when we retire, our income goes away. But that’s not the case.

“Income” in retirement is not usually made up of W-2 wages. Rather, retirement income is made up of any number of these income sources:

- Pension payments

- Social Security benefits

- Annuity payments

- Distributions from traditional IRAs, including Required Minimum Distributions (RMDs)

- Withdrawals from 401(k)s, 403(b)s, 457(b)s, and such, including RMDs

- Draws from small business retirement plans, including RMDs

- Interest and Dividends

- Capital Gains

- Other Income from Schedule 1

The combination of sources available to you to create income each year in retirement can change. You often control the amount of income you draw from sources you own, like IRAs and 401(k)s. Until you reach age 72, 73, or 75.

Then, Required Minimum Distributions begin. And you must take at least a specific value out of all your tax-deferred accounts. And include those amounts as income.

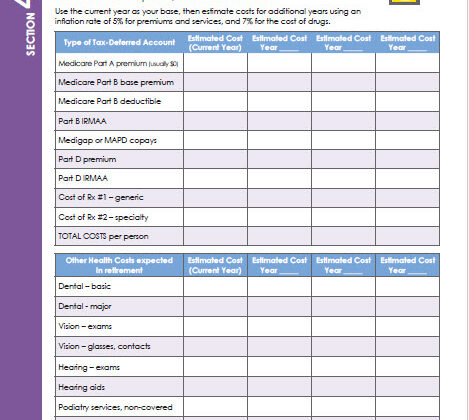

How Can You Estimate Your Medicare Costs with So Many Variables?

Until all the facts are known for any given year, it’s quite challenging to plan for and estimate your Medicare costs. The best you can do is take a shot at it based on your anticipated use of every piece of the healthcare system.

When I work with clients to help them budget for Medicare costs and all other healthcare costs, I use this worksheet. You can download a copy for free. Or you can get this one and other similar worksheets in my planning book, Cookin’ Up Your Retirement Plan.

(Click on the image to download a copy of this Medicare costs budget worksheet. Or click here.)

Key to understanding your costs come down to two big numbers:

- Your income (see discussion above), and

- Your non-Medicare covered “stuff”

Each fall Medicare (via CMS) determines and publishes Medicare premiums. Nearly every year, you can expect the premium to increase. There are occasional times when the premium stays flat. Or, it can even fall. But don’t plan on that in your forecast.

To estimate future Part B premiums, you’ll want to choose a reasonable inflation rate. For reference:

- Since Part B started in 1966, the average increase is 8% per year.

- Since the first Boomers entered Medicare in 2011, the average increase has been 3%. But there are wild swings from year to year. From a 13% decrease to a 16% increase.

- Since 2000, the average increase has been 6%.

I tend to be quite conservative on health care expenses, so I use 5% or 7% for Part B increases.

Plan for Increasing Medigap or Medicare Advantage Costs

A sizeable part of your Medicare costs plan needs to include your monthly premium for a Medigap supplemental plan if you have one. I’ve been tracking the monthly premiums for Medigaps in Massachusetts for several years now. They don’t tend to increase much. So far it’s in the $1 – $10 per month range. I don’t know how much other states allow for premium increases.

So, I suggest you start tracking what’s going on in your own zip code. Find the current year’s premium for the four or five least expensive providers that offer the most comprehensive Medigap. That’s Plan G in most states. Watch how the premiums increase each year, if you aren’t yet in Medicare.

If you already have Medicare and a Medigap, you might want to forecast using 1% – 2% inflation rate. Or just increase the monthly premium by say $10 for each future year.

For those choosing a Medicare Advantage plan, monthly premiums are generally not a big budget bite. But you are on the hook to forecast the increase in out-of-pocket maximums. They typically increase by hundreds of dollars each year. So your exposure to higher costs increases significantly if you get really sick. Also watch for increases in the out-of-network copays year over year.

Estimating Prescription Drug Costs and Dental

Two of the biggest drivers of Medicare costs are your prescriptions and your mouth.

Drug costs are completely dependent on the drugs you take. If you take two or three generics, you might estimate $10 per month for premium plus drugs. Then, increase it by $1 or $2 per year in your estimates.

However, if you have a high-cost drug, you’ll need to track the costs over a few years. Find the trend and apply it to future years. Also keep in mind the cost cap coming in 2025. All Medicare costs for drug spending are scheduled to be capped at $2,000 per person. And spread equally over the year.

And, if you are managing diabetes, stay on top of the cost management programs that have just become wide-spread. Most Part D plans are now charging a maximum of $35 per month for insulin. But other costs may apply.

Dental costs are a wild card

If you don’t typically need any dental care beyond twice-a-year cleanings and an occasional x-ray, you probably don’t need a dental plan. But if you end up at some point needing crowns, bridges, or implants, a dental plan might be something to consider.

Keep in mind, you get little value from these plans. You’ll pay a monthly premium, usually $35 or $50. That’s $420 to $600 per year. But the cost for cleaning might only be $125. So, you’re paying $600 to get $250 of services. Hmmmm….

If you eventually need some big-time dental work, having a dental plan doesn’t go as far as you may think. Most dental plans reimburse you only $1,000 or $1,500. A crown may cost around $1,500 plus additional fees. Bridges cost more and implants can be in the $5,000 – $6,000 range. But if you are paying a monthly $50 premium for 30 years, you’re paying the dental plan $18,000. And may only get $1,500 back. Hmmmm…

Best advice: talk to your dentist’s office to see what people find works well. And set aside a reserve in case you need something expensive later.

Other Costs Beyond Medicare Costs

When creating your budget for healthcare in retirement, make sure you plan for other items and services you may need.

Hearing Aids. Not everyone needs expensive hearing aids. And you probably won’t need new ones every year. There is a lot of innovation in hearing aids right now. There are over-the-counter options that are quite inexpensive. Same idea as your cheater eyeglasses. Put in your cost estimate after doing some research.

Vision care. Similar to dental plans, vision plans offer little in terms of real value. Sure, you might pay $35/month—$420/year—and get a “free” vision exam. But you’ll only get $150 toward eyeglasses or contacts every year or two. Depending on the terms of the plan.

In my case, I need four different pairs of glasses. Last time I bought two pairs plus new lenses in one. I paid over $1,200. Getting $150 back isn’t going to make much of a difference. And the premium of $420 adds to the costs in an unfavorable way.

(While I don’t have pink cat glasses, this image was too cute to pass up. Credit to Freepix.com)

Podiatry. Surprisingly, Medicare does not cover most podiatry services. Unless you are going for diabetic care. Talk to your podiatrist to get a schedule of costs for the services you use and budget accordingly.

The “CVS” Budget

One of the biggest items I find people leave out of the “Medicare” costs budget is their OTC spending. Over-the-counter. It is amazing how much we spend at CVS, Duane Reade, Rite-Aid, Walgreens, Walmart, Target, Costco, etc. All for non-prescription drugs and solutions to help our aging bodies feel better.

Many drugs start as Rx’s so they would be covered at a discount rate on your Part D plan. But then they move to OTC. And you’ll spend more. Stomach acid controllers come to mind. When they were generic prescriptions, you might have paid $2 – $5 for a 30-day supply. When they became non-prescription, OTC, they are now $25 for a 30-day supply.

My suggestion is to go to your regular drug store and load up your cart with all the health supplies you might use in a year. Everything from Voltarin to Tylenol, Band-Aids to Dr. Scholl’s shoe inserts. Don’t forget cold and flu medications, allergy relief, and eye drops. Then total up your cart.

That’s your starting budget this year for your OTC supplies. Increase by 5% to 7% for each future year in your budget.

Medicare Costs Are Really Much More Than You Might Have Expected

When we talk about the high cost of healthcare in America, it’s a combination of all these individual buckets. But we don’t pull together the full picture for people to understand. They only learn about this harsh reality when faced with insanely high healthcare bills.

I’ve been known to say there’s nothing affordable about healthcare in America. That’s because when you look at all the piece parts each of us is responsible for paying, it is not affordable for most. How could it have cost us $25 to birth a baby back in 1991? And now, it costs $2,500 for a visit with my knee doctor for a cortisone shot?

There is a lot broken about the American healthcare system. You are not going to fix it. I am not going to fix it. But we can all get a whole lot smarter about it! And go into retirement and our Medicare years with eyes wide open. And armed with a comprehensive, realistic, detailed budget.

If You’d Like More Information…

My latest book, Cookin’ Up Your Retirement Plan, has more on planning for the high costs of healthcare. The book is available on Barnes & Noble and Amazon.

If you are a fan of podcasts, you might really enjoy this one: An Arm and A Leg. “A show about the cost of health care that’s more entertaining, empowering, and occasionally useful than enraging, and terrifying and depressing.”

I’m just starting to get emails from writers on Substack. I thought it was a new platform, but it’s been around since 2017! Phil Moeller, one of the Medicare gurus I follow puts out some good info on his Substack page: https://substack.com/@philmoeller