Remain calm, cool, and collected during times of great economic uncertainty and personal unknowns (Part 1)

Back on Aug 19, 2019, we started hearing the “R” word come out of hibernation. And it wasn’t “retirement.” At that time most economists believed the United States would tip into recession by 2021. Now, four years later, we continue to hear we’re moving into a recession…no, we’re going to have a soft landing. The market is down…no the market is up. The wind is at our backs…nope those are gale force winds in our faces. Good grief. That’s a lot of angst in the air. A lot of uncertainty. And for retirees trying to manage their portfolio and create an income? Well, the crazy swirl of the economy is asking them to do the impossible.

Retirement Was Supposed to Be Relaxing

Those who retired back in 2008 and 2009 entered retirement in a state of shock. The great recession made for a mighty stressful start to retirement. While not as dramatic, today’s retirees face noise and haranguing by the media about the ills of the economy. Every day.

It is just as uncertain a time to be a retiree as ever. So much for that long-awaited retirement filled with relaxation and leisure.

Instead, many pre-retirees and retirees face more uncertainty as they are asked to do the impossible. Remain calm, cool, and collected as they deal with the great unknown forces of global markets and economies. And as they try to figure out how to address the very real likelihood their retirements will last for decades.

Regardless of what’s going on in the economy, each retiree faces certain perils.

In this post, we’ll look at some personal risks and situations that create angst and uncertainty in retirement. In the next post, we’ll explore some of the political and financial issues making retirement more challenging than ever.

Longevity: A Blessing and a Threat

Living a long time sounds like a great idea when you’re 40 or 50. Even at 60. My dad loves the prospect of living much longer…he’ll be 85 this fall. And my in-laws are amazed they’ve celebrated their 99th and 100th birthdays.

Longevity is no longer some abstract concept for many—or most—families. The silent generation folks are still around. Boomers will quite literally be here for decades to come. Not to mention the younger generations who should have millions more living even longer.

We all need to wrap our arms and legs around longevity. It is truly a blessing for so many, but also a threat. It is a risk we must plan for. Yet we are asking our retirees to do the impossible when it comes to their longevity.

“So, Charlie, just how long do you think you’re going to live?”

That’s hardly a conversation starter. But it’s the critical piece to the retirement puzzle. If you’re only going to have a 3-year retirement, the state of the world doesn’t really matter. But if you see 93 or 103, the forecast is very different. And you won’t want it to be rainy for your entire retirement.

“I’ve never needed a budget”

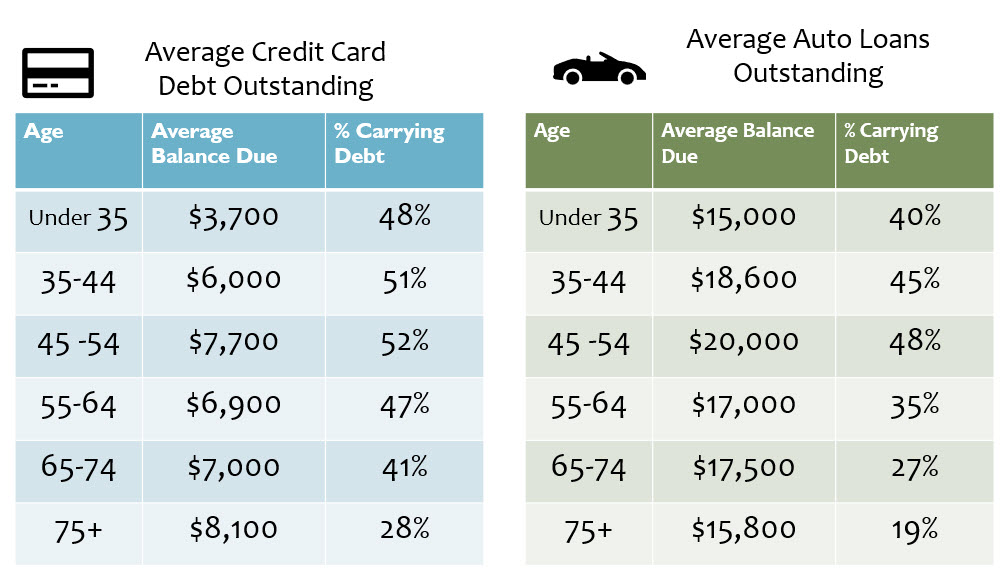

The fact of the matter is many folks who are retiring have never needed a formal budget. They lived within their paychecks and made adjustments when their household needs changed. Furthermore, the Boomers are the generation who first embraced credit. Why pay cash when you can charge it? You might even score some rewards points. Oy. All that does is saddle so many with a lot of outstanding debt.

According to the latest available data from the Federal Reserve Survey of Consumer Finances (1989 – 2019), we can see just how comfortable we are carrying debt.

As you look down the short road to retirement, time to figure out how you’re going to service that consumer debt. And your mortgage. And any student loans you may have.

The financial debt decisions we made years ago can have a mighty big impact on how our retirement spending is going to look. It’s another unknown piece of how we’re asking our retirees to do the impossible.

Budgeting for retirement is different. There is no paycheck to divvy up. You’re on your own to make your money last. Now’s probably the time to give a budget a try.

Asking the Impossible: How Healthy Will You Be 5 Years from Now?

Well heck, if I knew that, I’d have played in the last big lottery for the $1.5 billion win. We know that our own health or that of a loved one can change on a dime. And it will cost a whole lot more than a pile of dimes to pay for the care we will need.

The American healthcare system is fraught with complexity and costs impossible for most to understand. Including those in the industry. It is anything but “affordable.” Even with Medicare and supplemental coverage, the cost of health insurance and healthcare is a budget buster for most.

Add to the mess that is our healthcare billing system is: there’s no way to know this information. Unless you know where to look. Unless you’re willing to go deep and dig into Medicare’s Plan Finder tool. And if you’re willing to spend hours and hours researching the various private insurance market options.

Doesn’t that sound like something you want to be doing each year in retirement?

Failing to get into this healthcare game will be nothing but exasperating, frustrating, and costly. Yet that’s exactly what we are asking our retirees to muddle through. Asking for the impossible.

Set Up Your 4 Ps to Deal with the Impossible

In a nutshell, retirees are being asked to deal with the impossible on their home front. They need to navigate their next 30 years filled with personal uncertainties. To be fair, we’ve navigated the last 30 years which were also filled with uncertainty. But those earlier years came with a steady paycheck. We knew how the bills would be paid. Vacations and fun get-togethers just happened. No one had to over-think uncertainties.

But now, new personal risks enter the equation. Retirees are asked to predict the future using only a rearview mirror. And their personal best guesses for the future. Without spending all their money. A very tall order, indeed. To help get a start dealing with personal uncertainties, I suggest these 4 Ps as a place to start:

1 – PLAN for a long life…

…even though you may not really want to. That means at least 30 years of retirement, or until 95 or 98. Even if your parents didn’t live that long. The world is different today. There are so many modern miracles of medicine.

2 – Take a PRACTICAL approach to healthcare options.

to those modern miracles of medicine. Keep in mind cures and replacement body parts all cost a lot of money. We won’t know the language or many of the options. But be prepared to state your preferences.

3 – PERSIST against the odds and obstacles of aging.

Don’t take no for an answer when you need or want something. The world is not only here for the young! You may have to fight through phone trees, automated “help lines,” and other non-helpful processes before you get to talk to a person. And it’s up to you to keep up with the latest technology changes.

4 – PULL together that budget.

Even though you think it’s a waste of time. The costs of living are so much higher than you may realize. Add in inflation from these past couple of years, and costs rise fast throughout retirement. Clearly know where your hard-earned savings are going.

Stay tuned for Part 2 to come shortly…

For more information…

Get a free budget worksheet to help you tackle this thorny task in the blog post Plan for the Party & the Price Tag

And from the archives, you can check out Backyard BBQs and Back-of-the-Envelopes Budgets for some inspiration before summer is over.