Time to Reshop Your Part D Plan for 2026

I left Dunkin’ Donuts this morning with a medium hot coffee on a blustery fall day. Two construction workers walked behind me, laughing. One of them said that when he retires, he plans to spend every morning sitting in Dunkin’s. The other guy chimed in, saying he’ll do the same. He can’t wait to drink coffee and eat donuts every day. Well now, that’s quite a picture of retirement. I didn’t burst their bubble by telling them that retirement might not look exactly like that. At least not at this time of year when the Medicare Part D Open Enrollment Period (OEP) comes around. Yes indeed, it’s time once again to reshop your Medicare Part D plan.

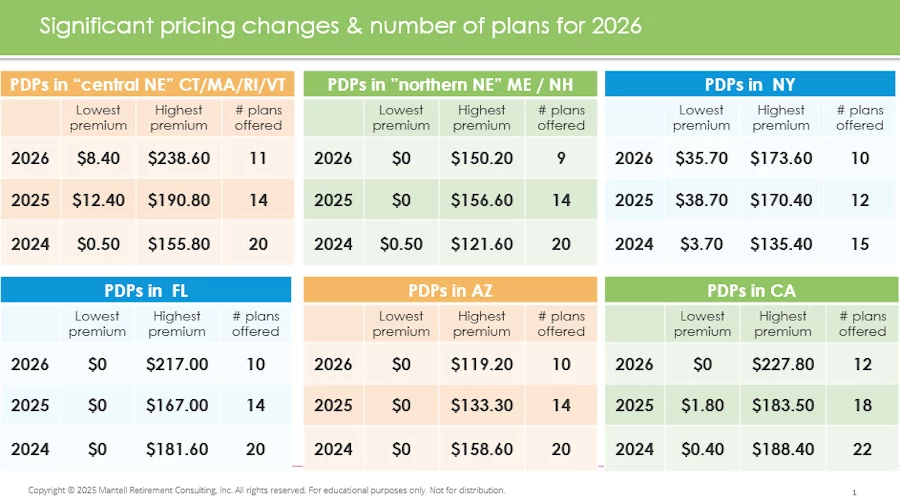

There are many more changes in Medicare Part D plans coming for 2026

It’s always important to reshop your prescription drug plan during Medicare’s Open Enrollment Period. But this year, there are more changes than we’ve seen in a long time. You will likely be affected by changes in your zip code. But if you don’t do the research, chances are good you’re going to be stuck paying more for your drug coverage than you should.

Here’s a summary of what’s changing from the insurance side of Part D plans:

- Some Medicare Part D insurers are pulling out of the market entirely.

- You will likely see fewer Part D plans available. In Massachusetts, there were 14 plans in 2025, but only 11 in 2026.

- The least expensive plan in 2025 may not be the cheapest for 2026.

- The name of the plan may have changed. Particularly, Cigna has changed to HealthSpring. Expect the drug coverage in the newly named plan to have changed as well.

- The drugs an insurer covers under their plan—on their “formulary”—will be different. Expect fewer drugs to be included in each insurer’s plan.

- Check your drug pricing tier. Some may now be more expensive, while others could be cheaper.

A look at more changes for selected states:

Checking the pharmacy status is key to success

Besides checking whether your Rx’s are covered or not, it’s super important to take a good look at the pharmacies in your area. As part of your Medicare Part D plan review for 2026, take a fresh look at the current status of the pharmacies.

Typically, you get the best prices when a pharmacy is “preferred, in-network.” Those that are just “in-network” tend to offer better prices than those “out-of-network (OON).” And OON are usually the most expensive. “Mail order” is often the most cost-effective option.

Unfortunately, the small, local pharmacies that many people like to support can rarely compete with the giants. You can still shop with them for most items, but your prescriptions may be cost-prohibitive at the small shop.

Your OOP limit is now $2,100…

You may recall a new law capping the total out-of-pocket (OOP) spending for covered drugs. The Inflation Reduction Act of 2022 was signed into law by President Biden. Notably, this law provided the federal government with a path to negotiate drug prices, especially for expensive medications. It also limited what consumers with a Medicare Part D plan would pay for their covered drugs.

People with a Medicare Part D plan—either as a standalone plan or wrapped in a Part C plan—had a $2,000 spending limit in 2025. That was the first year this cap was in place. However, the law was designed to adjust the OOP limit for inflation. As a result, the cap has increased for 2026. Those who have expensive drugs will pay slightly more, as the new cap is $2,100.

…but you can pay more in Medicare Part D plans

Many people find it frustrating that their total out-of-pocket (OOP) costs are not limited to $2,100. The cap only applies to the costs of drugs included in each Part D plan’s approved list—their covered drugs. It’s not necessarily your complete cost. You need to budget for premiums and drugs that are not covered.

Most standalone Part D plans have a monthly premium. You pay that directly to the Part D insurance company to participate in their plan. For folks with high-cost drugs, premiums tend to be higher. For example, in Massachusetts, the Blue MedicareRx Value Plus Part D plan premium is $20.70/month. That’s for their basic coverage plan. If your prescriptions require you to move to the Blue MedicareRx Premier, your premium for enhanced coverage jumps to $238.60/month.

For folks whose only option is the latter, their covered drugs will be capped at $2,100. But their total OOP will be $4,963.20!

And that assumes their Rx’s are covered. Just because they were covered in 2025 does not mean they will be covered in 2026 in the same plan. It is critical that you reshop and review all the options on November 1st for 2026.

Are you sure your Part D plan is still being offered?

This year, more so than in previous years, many Part D standalone plans have been discontinued. Insurers have reduced their options, and you may find that the plan you’re on no longer exists. Or, that it has changed names.

IMPORTANT: If you have a standalone Part D plan in 2025 that is discontinued for 2026, you must find a new Part D plan during OEP!

You will not be automatically switched from one Part D plan to another. You’ll need to take a fresh look at the new options and figure out your best new option.

To give you an example, in Massachusetts in 2025, there were 14 different Medicare Part D plans offered by six insurance companies. The 2026 offerings now include only 11 Part D plans. Wellcare pulled one of its plans. Cigna replaced its three plans with a new plan entirely. HealthSpring Assurance Rx was owned by Cigna but was acquired by another insurer in July. Who the heck would make the connection that it might be the same plan? Or is it?

Again, it is up to you to figure this out.

The Medicare Part D OEP is only 7 weeks long

The annual Medicare Part D OEP runs from October 15 through December 7. You’ll see this period referred to as OEP (the technical name) or AEP, which stands for Annual Enrollment Period. Either way, this is the only time of year you can reshop your Part D plan to make sure you’re getting the best option for the upcoming year.

While it’s helpful to have 7 weeks, I find it can lead to procrastination. So, I strongly recommend you lock in November 1st this year and every year as your day to reshop your Part D plans.

While frustrating and frankly unfair to make our oldest Americans jump through these flaming hoops every year, it’s how you’ll get the best deal. Medicare Part D plans are only 12-month-long contracts. Anything and everything behind the scenes can change during the year. And typically, things do change.

Please schedule this fun reshopping event on your calendar.

But I just started Medicare in 2025

I’ve helped many new retirees make the transition from employer group health insurance to Medicare over the last few months. So, they just started their Part D plan as of September 1 or October 1. They went through the process to select their first plan and received their Part D card a few weeks ago.

If you fall in this group, you’ll still need to reshop your Medicare Part D plan for 2026. You can only use the 2025 plan in 2025. And you won’t know what has changed if you don’t check out the underlying changes for the next year. The good news is that the process should be quite familiar.

The bad news is you will likely need to change your Part D plan already.

Where to reshop your Medicare Part D plan

Reshopping your plan isn’t hard, but it does take some dedicated time. And assembling all your Rx bottles. Hopefully, you’ve set up your “MyMedicare” online account. That’s where you save your Rx details, exact dosages, and your current pharmacy. It’s easy to confirm your drugs or make changes as needed.

If you haven’t set up your MyMedicare account yet, you can do so here: https://www.medicare.gov/account/login. You must have a Medicare number before you can set up your account.

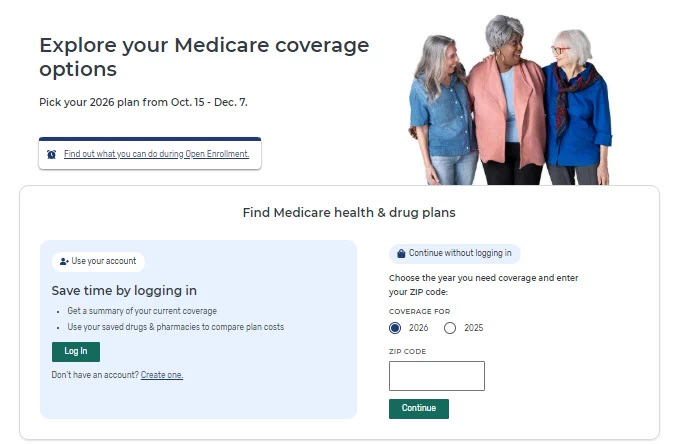

You will reshop your drugs and Part D insurance options using the Medicare.gov Plan Finder tool.

The most important steps to take:

- Make sure all prescriptions you’re taking now and will continue to take in 2026 are listed correctly. Double-check to prevent mistakes like confusing a capsule with a tablet. Or mixing up a 10 mg tablet with a 20 mg tablet.

- Include mail order as an option, even if you don’t love the idea of mail order. You may find significant savings.

- Choose multiple pharmacies to check their current status. You might need to switch pharmacies to find the lowest cost.

Caution! If you use a broker, they may not be able to get you into the least expensive plan

In an unfortunate development for consumers and the brokers many depend on, most insurers have decided to stop paying commissions for 2026. Brokers are only paid a commission on the sale or renewal of an insurance plan. They have been kicked to the curb. Insurers no longer want to pay brokers for the expertise they bring to the Part D analysis.

And you, the consumer, might not hear about the lowest cost plan for your specific Rx’s.

This is yet another game insurance companies play to stay focused on driving profits on the backs of unsuspecting consumers.

It is unfair to expect any broker or insurance agent to present a product option to you for no compensation. So, it’s up to you to get on board with reshopping your full range of insurance options before talking with your broker.

Do your homework, ask the tough questions

So how will you find out if you are getting the lowest cost Medicare Part D plan for 2026? You won’t if you don’t do some homework up front. Use the Plan Finder on Medicare.gov to get the full view of all plans offered in your zip code.

Then, ask your broker or agent directly about the plan they are recommending. You should feel comfortable asking them why they are recommending a particular plan for you. Especially if it is not the cheapest.

Which insurers have cut brokers out of paycheck?

To give you an idea of what’s happening out there among the biggest players, here’s a partial list of no-commission Part D plan situations:

- Wellcare (Centene) has been offering $0 and $0.50 plans for the past few years. They stopped paying commissions on all their stand-alone Part D plans. But many states include Wellcare with $0 or very low premiums, making them a consumer best-buy.

- Aetna has eliminated commissions for new Medicare Advantage and some Part D plans in specific markets.

- Cigna has done the same as Aetna.

- Humana says it is ending commissions for some of its stand-alone Part D plans. But it has become the least expensive in some areas. And it’s not paying commissions for new enrollments in nearly 300 Medicare Advantage plans.

- UnitedHealthcare has ended commissions for some of its Medicare Advantage and Part D plans.

- Anthem has scaled back on both standalone Part D plans and Medicare Advantage plans, discontinuing some plans.

- Elevance has cut commissions for new enrollments into some Medicare Advantage plans in some markets. And they have exited the standalone Part D market entirely.

- Health Care Service Corp (HCSC), the company that acquired Cigna and is offering HealthSpring Part D plans is not paying commissions for new enrollments in most of its PPO plans.

- Mutual of Omaha is not paying commissions on Part D plans because they have discontinued offering all Part Ds.

And the situation seems to change daily. Humana and Anthem are still up in the air whether or not they will pay commissions on standalone Part D plans.

A new option is available for everyone

I’ve been searching for alternatives for my clients, friends, and family. How can I help older Americans deal with these shenanigans? Something significant happens every year. And the game gets more and more complex. It’s nearly impossible for those of us who spend a ridiculous amount of time deep in the weeds of Part D plans to figure out what’s happening. Asking our 75, 85, and 95-year-olds to just “hop on their computer” and figure this out is reprehensible in my book.

So, I was intrigued when I saw the fantastic team at i65 came out with something they call “Hey MOE!” I wasn’t so sure about the name until I saw that “MOE” stands for “Medicare Open Enrollment.” Ah! Now, I get it.

So, I set up time with the amazing Melinda Caughill, who is the co-owner of i65, to get a demo of her latest software solution.

And I was super impressed!

How Hey, MOE! works for your Medicare Part D plan options

In a nutshell, Hey MOE is a clean, easy-to-use application that analyzes all your Part D options. It’s a super-fancy Medicare PlanFinder. But rather than you having to do the work, Melinda and her techie husband, Michael, proactively send you the latest information. All customized for your drugs from plans offered in your zip code.

Initially, you do have to take a few steps…but they are the same as you do when you set up your myMedicare account:

- Enter your exact prescription drugs, dosages, and details.

- Put in your zip code and county.

- Set up an account with Hey Moe for $30/year subscription fee.

I think the price point is very reasonable for the custom analysis and output you’ll get. Plus, Melinda was gracious enough to offer you a discount just for trying Hey Moe! Use coupon code “MARCIA” to get $5.00 off your subscription this year. Thanks, Melinda!

AND…drum roll here… you do NOT need to figure out which pharmacies are in-network, preferred, or out-of-network. Your custom output report shows you all of this automatically!

AND…another drum roll…the output also compares the price of Rx’s to what you could get on GoodRx!!

Hey, MOE! greatly exceeded my expectations

I am so tired of all the hype and hoopla about technology platforms, applications, and online “solutions,” only to be sorely unimpressed. Most folks who know me would say I am pretty critical. I can’t argue with that! My expectations are high. I believe we should do a lot more to make life easier for older people. And 99 times out of 100, these so-called solutions pretty much stink.

So, I set the bar very low (sorry, Melinda!) for my meeting about Hey, MOE. Instead, I had my socks blown off!

I couldn’t believe how comprehensive the analysis was. This program does everything I spend hours working on in the Plan Finder. And they compare so much more. The clarity of the information and the presentation was impressive. And the font was large enough that I didn’t have to zoom in or reset my laptop.

Yeah, these folks know what it’s like to get older and need three pairs of glasses to read at various distances!

It will be worth your time to check out Hey, MOE!

To be clear, Melinda had no idea I was writing this. And she hasn’t seen it in advance. I simply asked her if I could mention Hey MOE in my annual blog post. She said, “Sure.” And she immediately offered to set up the special coupon code for those on my distribution list. (Again, use “MARCIA” –all caps– when signing up to save $5.)

I don’t get anything from i65. The reason I’m sharing this option is to keep you up to date on a solution that might make OEP less daunting. I do think it is worth your time and your thirty bucks to try it out for one year.

You’ll get a complete set of your Medicare Part D options

The i65 team uses all the same data from CMS that the Plan Finder uses. And all that information comes directly from the Part D insurers and their pharmacy conspirators. So, you will get a complete view of your options in your zip code. The results are proactively delivered to you, so you don’t need to do a deep dive on your own.

Of course, it will be up to you to enter your correct Rx’s. And the tool is only available for standalone Part D plans. Not for Part Ds that are wrapped in Part C Medicare “advantage” plans.

I hope you will check it out, then let me know what you think.

Where to get more information

Just got to the Hey MOE home page: https://www.heymoe.com/ to take a look around. There, you will find all the information you need to decide whether to try Hey MOE.

Scroll all the way to the bottom. That’s where you’ll find these two key videos to watch:

- What happens when you have a MOE account?

2. How to set up your account.

You can also schedule a live demo and ask Melinda and the team questions.

Can you believe all the hoops you have to jump through just to get your Rx’s?

This is the question I ask myself every day from mid-September on. I truly cannot fathom how our Congress thinks this is the way to treat the Americans they represent. Especially the oldest Americans.

The penalty for missing the Dec 7th deadline or for skipping a year of shopping hits you right in your pocketbook. There is simply no way to get the best price if you don’t shop every year.

The penalty is two-fold:

- If you miss getting into a new Part D during OEP, you won’t be able to get a new plan until next year at this time. So, you’ll pay full retail costs for all your medications for the entire year.

- Then, going forward, you will pay a permanent penalty of 1% per month that you’ve been out of a Part D plan. Or, 12% of the base premium for every year you miss.

Mark your calendar for November 1st

So once again, I’m going to stress November 1st as your day to reshop your Part D plan. There are three tasks to tackle this November 1st:

- Hop onto Medicare.gov to revisit your online account. Read any communications. Update your Rx’s. Make sure everything is in good order for your current situation.

- Run the PlanFinder for your 2026 options, making sure you only use pharmacies that are preferred, in-network. Don’t be surprised if you have to change insurers this year to get the best price.

- Try out Hey, Moe! See if you like their approach, customized analysis, and output better than the Plan Finder.

Whichever way you decide to reshop your plans is just fine. The key is to reshop those dang Medicare Part D plans. This November 1st and every future November 1st.

Send me a note if you have something fun to share, something frustrating, or just to say hello. Wishing you the best this Open Enrollment Season!

Other helpful Medicare Part D resources

Take a fresh look at all your healthcare costs and project them out for the next few years. Use the free worksheet in this post, Estimating Your Medicare Costs.

Wall St. Journal article, Big Changes Are Coming for 2026 Medicare Plans. You might see a quote from me in this article!