March is Women’s History Month

A woman’s approach to planning her retirement has always been different from a man’s approach. That’s not to say that men aren’t doing a good job. But rather a fact that men and women approach most things differently. Women’s opportunities to own and manage their own finances is a recent development, largely thanks to some women in the 1800s and 1900s.

Women could not own bank accounts

Due to the legal structure the original colonists brought over from England, married women were legally excluded from owning property or assets. If a woman earned a paycheck, it went directly to her husband. Practically speaking, bank accounts were unnecessary. What did she need it for anyway? Her husband or father handled all the household finances.

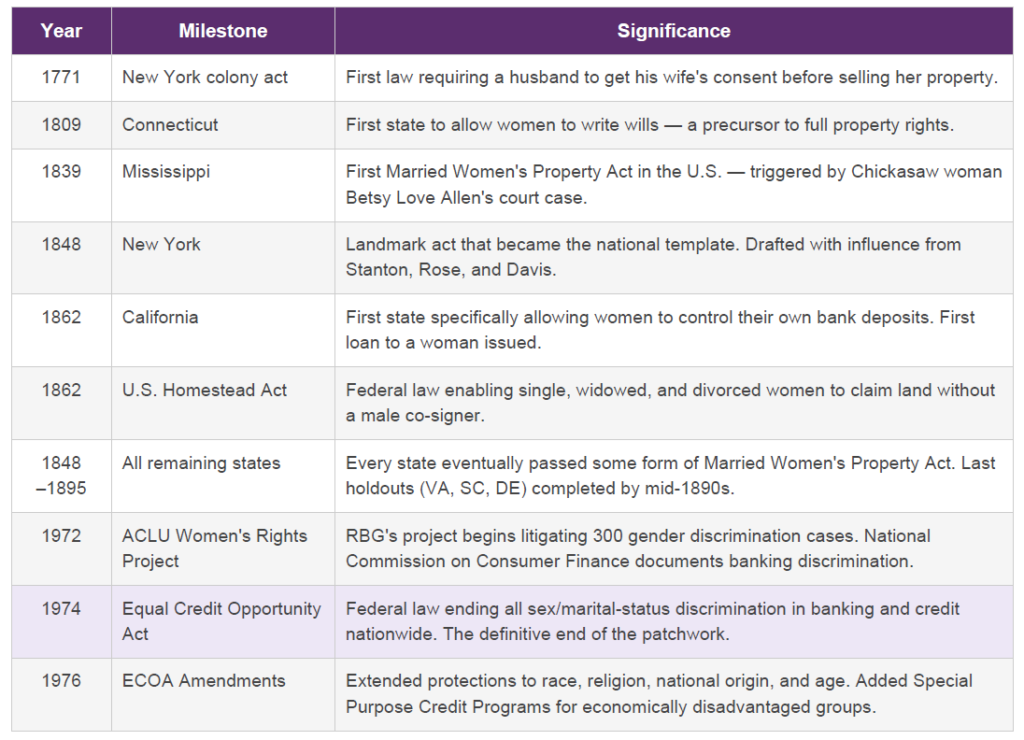

A watershed moment occurred in 1848 when New York State passed the Married Women’s Property Act. This gave women full property rights, the ability to enter into contracts, and to keep their inheritance. It also relieved her from debts incurred by her husband.

But she still could be (and was) discriminated against when trying to open or manage a bank account. California made the first move in 1862. The lawmakers in California specifically allowed women to control any bank deposits in her name. It was the first such banking protection in the US.

The states were slow to enact property protections for women. The last three states—Delaware, South Carolina, and Virginia—finally got on board by the late 1880s and 1890s.

Lawmakers spent a century lollygagging

It took another 100 years before women could fully be a part of the financial and credit system in the United States. 1974 ushered in the federal Equal Credit Opportunity Act. Only then could all women across all 50 states fully participate in their financial future.

Women could now open bank accounts and apply for credit cards. They could obtain mortgages and business loans independently, even if married. Their gender could no longer be used against them in financial services.

That was only 52 years ago. I was a teenager.

Women took matters into their own hands

It should come as no surprise that women were not always delighted to get married. They were stripped of all their financial assets, abilities, and worth upon marriage. And surely you aren’t shocked to learn that femme sole (unmarried women) faced more hurdles when applying for banking or credit services.

But it may surprise you to learn that in 1877, an 87-year-old woman opened a bank. She was Deborah Powers of Troy, NY. As a widow, she ran her husband’s manufacturing business and turned it into a worldwide success. The business was valued at about $2 million.B

It is the first known US bank opened by a woman. She likely needed to start her own bank. Dealing with successful, financially strong women was not the norm in banking at the time. And it was probably a better way for her to protect her estate. She died in 1891 at the age of 101, and the bank closed shortly thereafter.

Eight women in total opened banks in several states during the late 1800s and early 1900s.

The feminist banking wave in the 1970s

It wasn’t until the 1970s, after the passage of the federal Equal Credit Opportunity Act, that another 8 banks were opened by women. Historically, this is considered a “feminist banking wave.”

I’m not so sure I buy that label. In the 1970s, among nearly 14,000 banks in the US, eight were founded by women. Fewer than a dozen surely cannot be considered a great wave of change.

Today, only 18 banks are listed in the banking regulatory system as women-owned.

That’s right. Only 10 more women-owned banks exist today than did in 1978.

Getting data about women in banking is challenging. One summary I read noted:

“Nobody was counting women bank owners or presidents in the 1970s. It was so rare it wasn’t considered a meaningful category to track.”

Ouch.

Why then would a woman have an approach to planning her retirement?

This is a less-than-illustrious history of discrimination, lack of access, and putting the little lady in her place. Is it any wonder that many women haven’t embraced planning for their retirement?

If a woman couldn’t even have a bank account or credit card until 50 years ago, it’s a pretty big leap for her to start investing. Let alone knowing how to plan her retirement income, which needs to last 30 years or longer. Or even where to start.

That’s one area I focus on. And one way I can help women move forward in building their own financial and retirement knowledge and know-how.

Many women have no idea what planning her retirement entails. This is not a quick weekend project. Rather, it’s the culmination of decades of learning to make the right moves at the right time.

The good news is that many women, especially in younger generations, are making rapid gains across financial and retirement fronts. But it’s not a universal skill or area of interest by any means.

Help is available to get a good start moving forward

I’ve tried to address the realities of being a modern-day woman. We’re all part of a group that has had meaningful financial access and the possibility of power for only 50 years. We might not know as much as we need to about planning for retirement. But we are now in a position to change that.

Continuing the conversation with hundreds of women led to my updated book. Now in its second edition, What’s the Deal with…Retirement Planning for Women? is available on Amazon. If you haven’t had a chance to read it, I encourage you to do so. I think you will recognize yourself on many of its pages.

There were many revisions to make and updates reflecting recent changes in the law. There are also new topics, including the importance of a high credit score and how much your “free” Medicare might cost.

Planning her retirement with 13 key questions

This update is similar to the original version of the book I wrote back in 2015. You’ll find 13 key questions you need to ask yourself. And ideas for how to answer them for your own unique circumstances.

“It’s a non-traditional, fun-filled book that poses a baker’s dozen questions every woman needs to talk about…”

I wrote the book from a woman’s point of view. I wanted to recognize and give credit to the unique ways women approach life and money. Rather than trying to fit us into a “traditional” financial planning structure, the book shows women how to leverage their experiences. And it credits women for embracing their personal style to manage money.

The book is short, sweet, and practical, and filled with resources. Each woman I talk to about planning her retirement is too busy to go through a financial textbook.

It recognizes that women’s priorities are centered on family, community, and traditions, but that can leave them financially vulnerable. The book outlines specific actions women can take to protect themselves financially.

Most of all, it celebrates women’s love of planning a party… but stresses that we need to plan for the price tags, too.

Continuing the legacy of 19th and 20th-century women

It never fails to stop me in my tracks when I read about the women who settled America. For hundreds of years, they had no financial power. They were beholden to their husbands and fathers.

Often, women achieved financial success after their husbands died early. She had to step in to continue the work he had started. Even then, the patriarchal financial system did not allow her to participate.

Fast-forward to today. Women still find themselves lagging behind in planning for retirement and in owning retirement assets. It’s important to understand that your husband’s 401(k) is not yours! You are not a party to his retirement savings… at least not under current law. On the other hand, your husband is not party to your 401(k) either.

It’s important this month to honor the women who helped us get this far. We also need to continue moving financial freedom forward. Stay mindful of the financial access we have and fight the barriers we face. We owe our gratitude to Deborah Powers and many other women who refused to settle for less.

The best way to continue the legacy in the sisterhood is to make sure you are planning for retirement. It’s not going to happen by magic. Sometimes it starts with a good book that challenges you to think about your financial future.