Welcome to the follow up information from The Fearless Retirement Summit – 2021, hosted by Tom Morris of Northwestern Mutual. I hope you had a an excellent experience and learned why it’s so important to retire to something. And, of course, are now more knowledgeable about Social Security.

Everyone approaches retirement in unique and special ways. But there are some common threads that all retirees must plan for. Frankly, I find that so many near-retirees are ill-equipped to make the best Social Security claiming decisions for their future.

Claiming at 62 is often a regrettable decision

Before retiring, most individuals I hear from are so excited they are turning 62. They know they are standing at the “gates to free money.” It is often quite challenging for me to encourage them to reconsider claiming so early.

After retiring, I hear from the other folks. Those in their 70s and 80s. They are chock-full of complaints about how small their Social Security check is. How inflation adjustments don’t help much. That their companion Medicare premiums eat up the annual cost of living increases. And, many report they regret now that they claimed so early. It seemed like a reasonable decision at the time, but not so much now.

The worst, of course, are the 80+ year-old ladies who are left to handle all their finances after their husbands die. They had no idea they were going to have such a significant reduction in Social Security. No idea their check would stop immediately and they would be left with just his payment amount.

As you can imagine, it is frustrating and sad to hear these stories.

Consider your claiming strategy wisely

For those who joined us at the Fearless Retirement Summit, I hope you took some good notes. And have a fresh perspective on the role Social Security plays in your overall retirement income plan. Taking time to work with a retirement financial advisor on when to claim can help you out. Deciding when to claim is a key step in the planning process.

From one seasoned retiree: “It ain’t cheap to live in retirement!” Words to live by, indeed.

As I covered at the summit, you will claim in one of four categories. Social Security sees you as married, divorced, widowed, or single. The benefit amounts, the steps you must take, and the timing must all align for you to get your best payment for your situation.

There are many nuances under each of these categories. To help you navigate your “Social Security swim lane,” I’ve developed various checklists. These should help you get a good start on what to look at on your statements. And, how to think about your option as a worker and something else. You might have your own work record and be a divorced person. Or, you don’t have enough credits to qualify on your own, but your spouse does.

I invite you to scroll through these checklists and find the one that supports your situation. They are free to download. Just click on the image or the highlighted text.

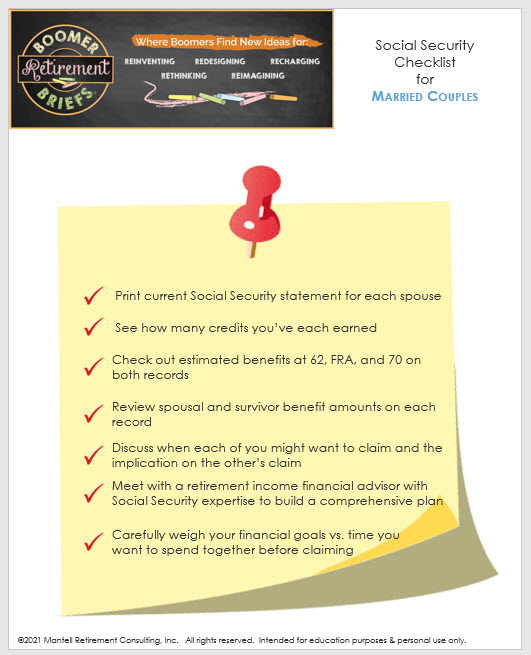

Social Security checklist for married couples

Getting your claiming strategy just right between spouses takes some time and effort. Not only are you thinking about the early years of benefits, but also the impact on the surviving spouse in later years. Click here for the checklist.

So long as you are legally married, the spousal options apply to you. Same-sex married couples or opposite-sex married couples. With Social Security, married is married.

There are many possible combinations depending who is the higher-earner, what your age differences are, and your overall financial picture. Also consider that claiming 6 months or 12 months before your FRA does not make a substantive difference for many. It might be better to spend quality early years of retirement together doing what you want to do together.

You can never get back time with your spouse.

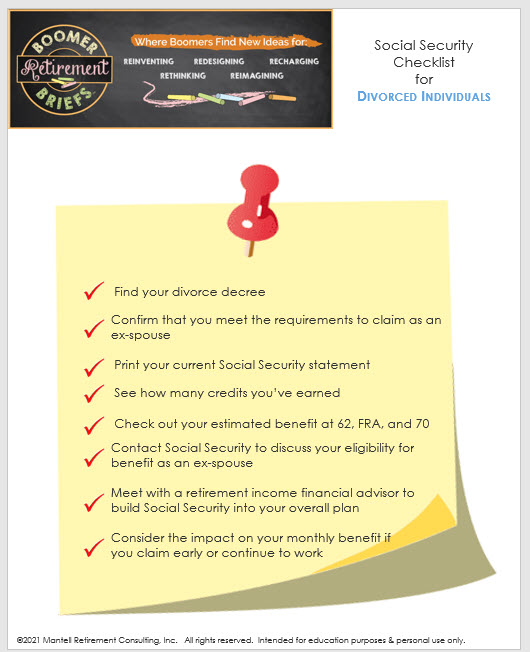

Checklist for Divorced Individuals

Many divorced people are surprised to learn they might get a higher benefit by claiming on their ex-spouse. It is possible for many. But there are specific and rigid rules that must be followed.

Review this detailed checklist to see if you meet all the rules for claiming as an ex. The maximum amount you could receive is half of your ex’s calculated benefit. And, you must be at your FRA to receive your maximum.

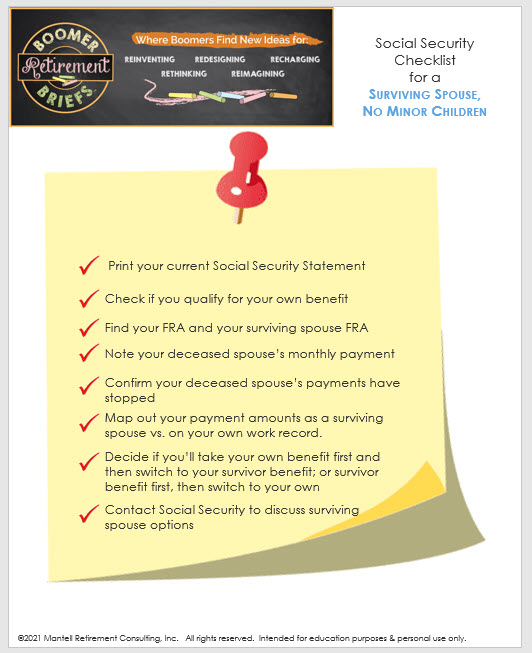

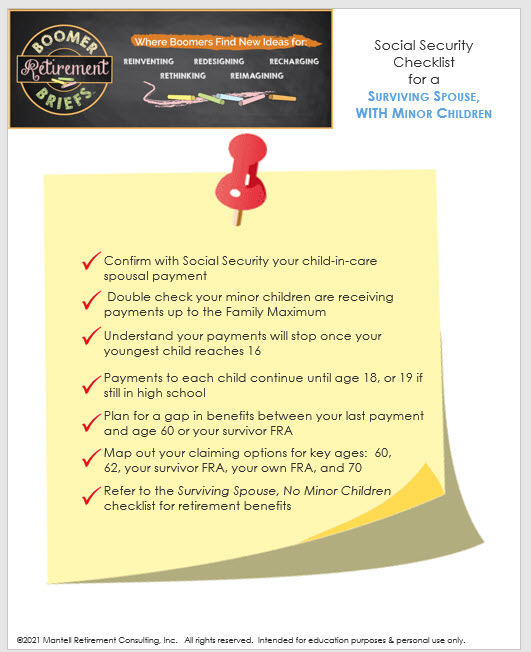

Widows, widowers, and surviving spouses with minor children

Protecting survivors is a critical piece of Social Security. But it is layered with nuances and process that most agents don’t even understand. Select from the checklists below to find the one that fits your situation. These will give you an idea of where to get started with surviving spouse and benefits for minor children.

If you are a surviving wife or surviving husband and have no minor children at this time, use this checklist.

If you are a young widow or widower with minor children in your care, use this checklist.

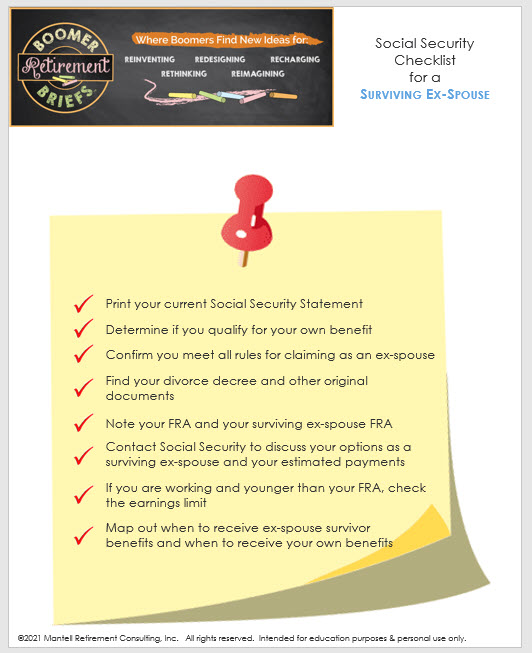

Ex-spouses are often entitled to survivor benefits

If you are divorced, unmarried, and your ex dies, you may well get an increase in your benefits. There are several rules you must meet to be eligible for ex-spousal survivor benefits. But, if this is your situation, and you are the surviving ex, use this checklist.

You may well be entitled to higher benefits.

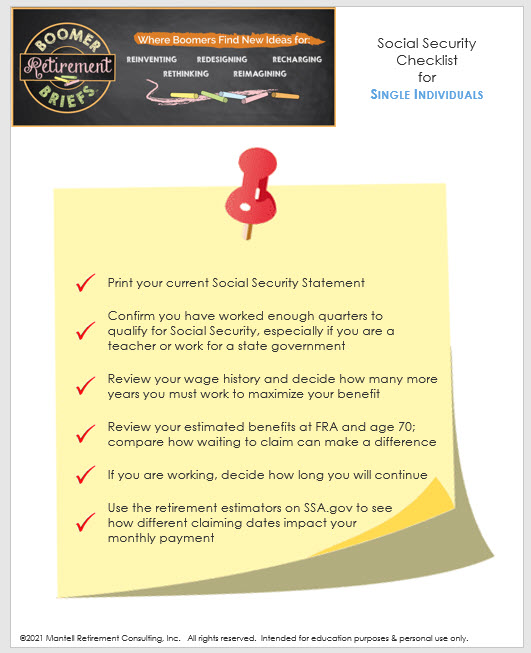

Single individuals have key decisions to make about their benefits

Not the least of which is when is really the best time to claim. Will you fare better by waiting until 70? Or, is your retirement income plan strong enough for claiming at FRA?

Use this checklist to start your Social Security process.

Additional resources

Figuring out your claiming options is one thing. Actually pushing the button to claim is generally an irrevocable decision. And, a really big financial decision.

I hope you got a good start at the Fearless Retirement Summit. Now, feel free to use these other resources here in my blog. And get a copy of my book, What’s the Deal with Social Security for Women. There are more examples and information at your fingertips.

What’s the Deal with Retirement Planning for Women

When Is Social Security going bankrupt?

And, contact me with any questions or concerns you may be having. I’ll try to help out.