December can be such a complicated time of the year. The holidays are both stressful and enchanting. Things at work should be winding down, but often amp up to get a jump-start for the next year. Add to the mix this year: holidays during COVID-19. Now what are we up against? What is a sane person to do? It seems that everyone has decided to decorate early. Sales of Christmas trees are up 29% after Thanksgiving. Decorations in front yards—those crazy blow up Christmas and Hanukkah characters—are out early. We’re trimming the tree and lighting the menorah. But, are you also setting aside a few hours to decorate the rooms in your financial house?

But, first, decorating with twinkly lights

Before diving into your financial house, let’s first celebrate the holiday season. Like so many others, this year, I wanted to do more decorating outside. We have a few bushes by the front steps. I always put multi-colored lights up on those bushes.

And, we put hundreds of multi-colored lights on the white fence in the backyard. I can see these festive colors from my kitchen and laundry room. And, neighbors can see them as they drive down the street toward our house. So, they are a lovely outdoor decoration.

But, this year, I’m extra excited that we found these very twinkly round balls of lights. And, fake snowflakes with 150 mini lights. They will look amazing placed among some of the pine trees at the front of our driveway. It’s a little mini-forest area, and some added sparkle should be just the lift I’m looking for.

What do you mean we have no electric power?

We decided to decorate on Sunday. It was relatively warm for New England, and it wouldn’t take long, so we thought. But, we immediately ran into a problem when Dan checked the outside electrical outlet for the front lights. All of a sudden it didn’t work. Really?

Then, Dan asked me an interesting question: “If we hang your new “twinkly lights” in the mini forest, how are you going to plug them in? There’s no power outlet on that side of the driveway.”

Well, good grief. I can’t think of everything!

Needless to say, Dan got a trip to his favorite store out of our decorating fun. Home Depot to the rescue. He bought a new outlet for the porch and some 250 feet of super-industrial-strength, outdoor, extension cords. Turns out, there are outlets in the garage. And who doesn’t need 250 feet of extension cords laying all around the yard for twinkly lights?

It’s all quite magical

I’m happy to report that we successfully decorated the outside of the house. It took us about 6 hours each to add that extra sparkle. But, when that sun goes down and the lights go on, it is all quite magical.

We’ve noticed cars slowing down and neighbors stopping by to see the new lights in the mini forest. Glad to spread some holiday cheer. Especially this year.

Next up is to decorate the rooms in our house. It’s amazing how many nooks and crannies all of a sudden need a sprig of holly or a few ornaments. We have the menorah and dreidles out near the Christmas tree. The railings have evergreen swags and stockings hung with care. And, the nutcrackers stand like sentries at the top of the stairs.

All in, we’ll probably spend somewhere around 15 hours each decorating and wrapping presents. All for one day of celebration.

Think about the rooms in your financial house

Throughout the year, I talk with a lot of folks who are reluctant financial people. They get frustrated with how complex the rules of money really are. They find it very frustrating to deal with all kinds of different financial accounts. And twice as frustrated when we start talking about how every different account has different tax requirements.

But, we all have a lot of accounts. Some people collect Christmas ornaments over the years. Others have a treasure trove of dreidels. Regardless of your personal collections, we all have a necessary collection of financial accounts.

Sometimes it helps if we compare each financial account to a different room in house. A kitchen serves a certain purpose that is different from the living room. Bedrooms might be for sleeping or now for working from home. But the purpose they serve is definitely not the same as the bathroom. Or the laundry room. Or the unfinished basement.

Yet, each room is necessary, and you really can’t do without those rooms.

“Decorate” the rooms in your financial house

It’s the same idea for a financial house. You need all of those different accounts. Most of them cannot be combined into one giant great room. There are too many different rules and tax considerations that require different accounts.

So, as important as it is to make your house look special for the holidays, it’s just as important to “decorate the rooms in your financial house.” Meaning, give each account the extra attention it needs. Freshen it up a bit. Add a bit of sparkle as you think about how that money will allow you to do so many things in the future.

This isn’t the time to do a deep-dive into your investment strategy or rethink long-term goals. Unless you’d like to do that. It’s more of dressing things up and making sure your accounts are current and titled properly before things get so crazy at tax time.

Why December?

Why is it important to do in December, though? Well, frankly, after Hanukkah and Christmas, you aren’t as pressed for time. For many of us, our houses are as organized as they get all year. Everything looks so nice. And you can finally relax as you wait for the New Year to roll in.

You or you and your spouse or partner can likely find four hours of quality time to talk about your money. It’s a quiet time to think about where you’re going with all those accounts. And, how they will pave the path to your financial future.

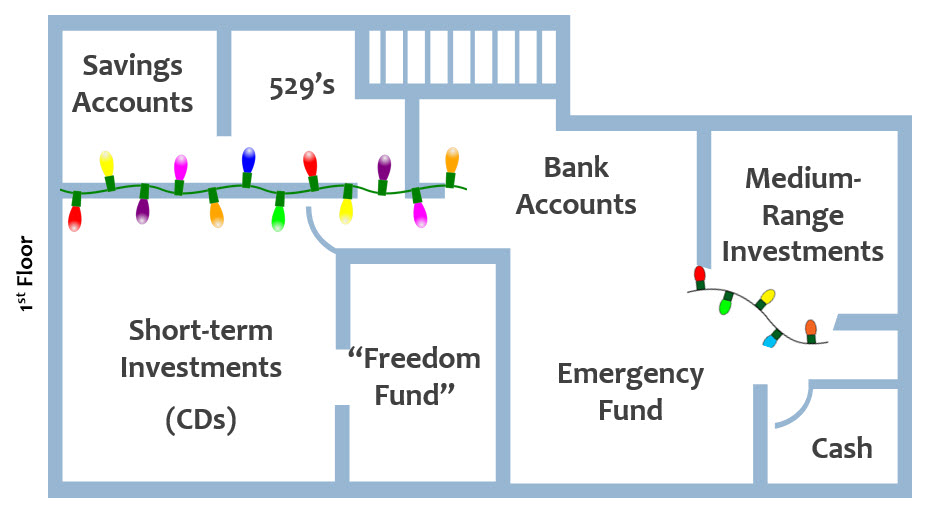

Decorating the rooms in your financial house – the first floor

The rooms on the first floor of your financial house are the more active accounts. They are the ones you use to run your household on a daily basis. Most are for cash flow and short term needs, but a few are investment accounts for meeting medium-term goals. It’s important to check in on these accounts to make sure they are set up properly, with current information. You know, like adding some decorations!

For example, your taxable brokerage accounts typically have an option for you to name a “TOD”. This is a transfer on death directive. This allows someone to take over that investment account upon the owner’s death without going through probate. In many cases this is a simple form you can get online from your brokerage firm. Many people don’t know to take this extra step. It’s easy to do and important.

Even your bank accounts should have proper papers on file to allow for the transfer of money upon death. Do you have a POD on file with your bank–a payable on death order? In fact, that’s one thing I have to recheck this December on my own accounts. Like a TOD, the POD is a simple form that you fill out and sign for each bank account. You choose who will inherit the account upon your death, again, avoiding probate. (Read more here.)

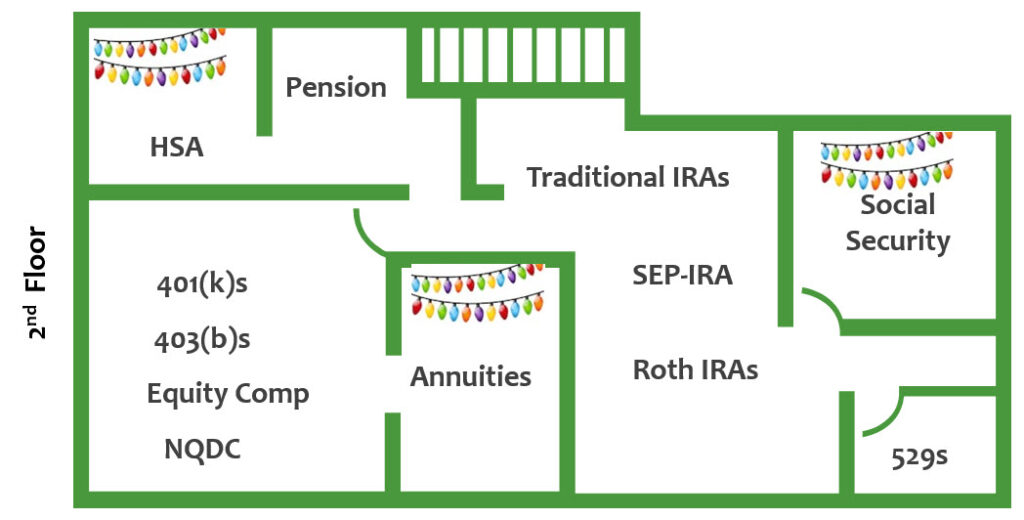

Decorating the rooms in your financial house on the second floor

Think of the rooms on the second floor for retirement and long-range goals. One of the most important things you can do is to check your beneficiaries in these rooms. On every different account you have. And, on every one your spouse or partner has.

All types of IRAs that you own need beneficiaries named. It’s amazing how many people find that they haven’t named new grandchildren on their IRAs. Or, a beneficiary has passed away, yet they are still listed on an account. Either case creates problems for inheritors. Check all Traditional, Roth, Rollover, SEP, and SIMPLE IRAs.

Did you realize you can change beneficiaries on college savings 529 plans? And at any time without tax consequences on that account? Each 529 account can only include one person as beneficiary. (Read more here.)

However, there are often times when the original beneficiary doesn’t end up using all the money. The owner can change the beneficiary to any other qualifying family member. Including to yourself. If you are looking forward to taking some college classes during retirement, this could be an ideal situation. You just fill out a “change of beneficiary” form available at the financial institution that holds your 529.

What steps will you take this holiday season?

You may be thinking that it’s not the same thing to decorate your house for the holidays as to decorate the rooms in your financial house. But, my real point is this: If you can

- spend 15 hours stringing lights all over your yard,

- enjoy 8 nights celebrating Hanukkah, and

- take 2 days to enjoy Christmas,

surely you can find a few hours by the end of the year to put some shine on your financial accounts. When we find ways to better incorporate our financial household into our regular household, we’ll be more successful.

Wishing you and yous the happiest of holidays this December.