March is National Women’s History Month. It’s a wonderful time to recognize the women and men who have changed the world to make it better for women. As I think about the advances made for women on the financial front, there are truly remarkable achievements. Except in one particular case. Many wives still take a retirement back seat to their husbands. It’s largely because of the structure of the laws for 401(k) plans and IRAs. So, let me start by saying this to all married women: That 401k isn’t all his!

Let’s first recognize progress that has been made

Take a step back. Maybe five or six centuries. For hundreds of years women have been fighting for equal access to money and property. And for their own financial power. Take a look at some of the laws that started to open the financial gates for women:

- 1848 – The Married Women’s Property Act. Married women in New York State were granted the right to own and control certain property separate from their husbands.

- 1869 – Women’s Right to Vote. But only in Wyoming. This was the first state to allow women to vote 50 years before the 19th Amendment.

- 1974 – Women were finally allowed to open their own bank accounts or get a credit card without daddy’s signature or a husband’s approval.

- Until 1981 – Husbands could unilaterally take out a second mortgage on their jointly owned house and property. Wives had no idea, until they were left with the debt.

- 1997 – The first year an at-home mom could finally save the same amount in her own IRA as her husband who was employed and earning wages.

Clearly, we see progress is forward-moving. But it’s also slow in the making. Yet with every new law, women gained at least one step forward. And sometimes a giant leap. These laws were finally written to acknowledge a women’s roles in the financial running of their households. And, for their future as a retiree.

The Imbalance of Financial Power Between Spouses

Yet, here we sit. It’s March 2021. And married women and their spouses need to grapple with a key fact. Due to the legal structure of retirement laws, someone in the marriage does not have financial equality. And, to be clear, it can be either the wife or the husband who is in the subordinate position.

However, in my never-ending quest to help women take charge of their financial future, I’m directing this conversation to married women. Specifically, to those who have no 401k of their own. Or women who have much smaller retirement accounts than their spouse.

Married women in these situations need to understand that a husband’s 401k isn’t all his.

When a wife doesn’t have her own retirement accounts, there is an imbalance of financial power. It shows up particularly as they near retirement. At that point, wives see first-hand that they have no access to money that is for her retirement. They must ask their husbands for permission to get at money that is fully intended to be hers.

A financial power imbalance can happen in any marriage. It’s set up any time access to a financial asset requires one spouse to “ask permission” of the other. Or when laws allow only one spouse total control of a financial account that is meant for both parties.

This is exactly what is happening today. 401(k)s and IRAs have become the foundation to most couple’s retirement income. Yet, only one spouse controls all the decisions in an account.

She Has No Rights to “His” 401k

And, conversely, he has no rights to her 401(k) either.

Here’s the situation. If the husband has a 401(k) at work, the wife has no access to the account. In fact, she cannot even get information about that account. By law. So, if I call Dan’s 401(k) recordkeeper and want to know how much is in his 401(k), they cannot tell me. If Dan calls my 401(k) recordkeeper and wants to change an investment, he can’t touch it.

Furthermore, wives cannot do the following in a 401(k) that is only in her husband’s name:

- See the account balance or access the information online.

- Start, stop, or change contribution amounts.

- Select or change investments or buy and sell to rebalance the account.

And, worst of all, she has no way get at so much as a single dollar from this account. So, she has no purchasing power with money that is fully intended to be hers for retirement.

There’s No Balance of Power If She Has to Ask Permission

Unless she asks for permission. Or he grants her official access to the account.

It is no easy task to allow a spouse access to a 401(k). The husband must execute a formal Power of Attorney document. He must name his wife to act in his interest. He must send the form to his recordkeeper. And, then follow up to make sure they’ve now got this permission slip on file.

Wow. Who’s going to make that kind of effort?

Remember that 401(k)s are fully intended to provide retirement income for both spouses. They have largely taken the place of defined benefit pension plans that paid income until the second spouse died. Not so with 401(k)s.

But let me be clear here. Wives, too, have a major stake in any 401(k) in their husband’s name. They just don’t have equal rights to it.

At least until he dies. Or they get a divorce.

That 401k Isn’t All His When He’s a Married Man

Isn’t that a snarky comment? But, it’s true. Dan cannot go into his 401(k) and take out $100,000 and put it in a tax-deferred IRA with my name on it. But why not? I’m pretty much entitled to half of his everything. (I really think it should be 90%…) But not while he’s alive.

We know there is an intent of equality because of death and divorce situations. If a husband dies while assets are a 401(k), it is generally required that the sole beneficiary be his wife. Now she gets 100% of the assets. And, if a married couple gets a divorce, the 401(k) assets are generally split 50-50. Or at least the valuation is considered 50-50.

But, while both spouses are very much alive and happily married? She has no say into money that is clearly intended to be for her retirement.

Things Get Worse for Wives When the 401k Is Rolled to an IRA

There is a very real financial danger to a wife when it comes time for her husband to roll that big 401(k) into an IRA. And, it’s a hidden danger.

In most, but not all 401(k)s, the other spouse must sign the rollover request. She must agree in writing that he can move the 401(k) to an IRA.

However, without realizing it, the wife has just signed away her claim to her own retirement money. To be fair, neither spouse really has any idea this is what just happened. And, it’s not a malicious action on the husband’s part. It has everything to do with the way the laws are written for retirement accounts.

Once that money is in an IRA, it is well and truly an individual account. And there is only one owner. And he controls everything. There is no obligation to allow his wife any access whatsoever. Even after he’s dead.

Quite literally, with the push of one button, he can remove his wife as his beneficiary. Or, he can name four or five or six others as equal beneficiaries to her. So, maybe she’ll only get 20% of what should have been her retirement money.

Dan’s Tired of Hearing Me Talk About This!

Is it the intent of our retirement laws to create such a financial power grab in a marriage? Probably not. But the reality is, our current laws allow these types of actions and opportunities. The result can be cutting wives out of their retirement money. And, cutting husband’s out of their retirement money when the tables are turned.

And, I’m hoppin’ mad about it!

Dan told me he doesn’t want to hear, “But that 401(k) isn’t all his” one more time. He said it nicely. But, once I get a bone in my teeth, well, I can go on.

And, the funny thing is, I realized how dramatic the power imbalance can be in a marriage from my own 401(k). Dan and I were rebalancing some of our investments and needed to make a change in my 401(k). Since he was already doing the trading in other accounts, I asked him to place the sell order for me.

But, he couldn’t find my 401(k) in his list of “our” accounts. It’s not a small account, so he really should have seen it. I got up to show him where it was. And, to my surprise, it wasn’t there. My 401(k) was missing from our list of accounts held at the same financial firm.

Husbands and Wives Can Grant Access to IRAs, but Not to 401ks

All my IRAs were right there along with Dan’s. With IRAs, the owner can grant access to anyone to view the account or have full trading authority. But the IRA owner must do so proactively. We have already granted access to each other on our IRAs. That’s what allows Dan to see my IRAs and make trading decisions. After all, this money is meant to be for both of us in retirement.

But, 401(k)s are qualified plans. Except with a POA fully executed and in place, only the employee has any access. So, in fact, Dan was right. He could not see my 401(k) at all.

Are you noting the verbs I’m using here? Grant access. Allow. Give permission. Deny access. These words should not be used in a marriage. I don’t “allow” Dan to do things. He doesn’t “give me permission” to do things.

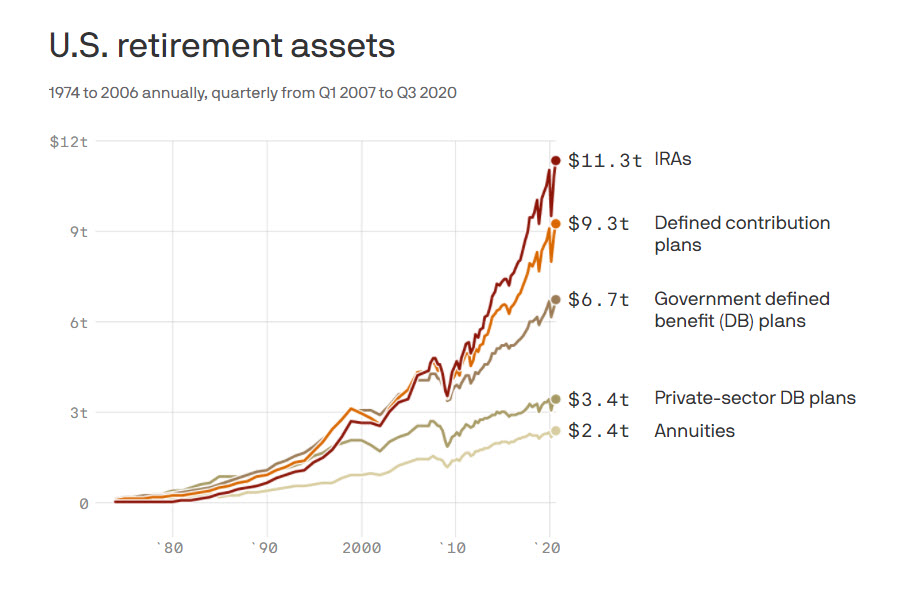

So, why is our entire $33 TRILLION retirement savings system set up in a way that can quite literally pit one spouse against the other?

This chart shows retirement asset data from the Investment Company Institute (Chart: Andrew Witherspoon/Axios). At the end of the 3rd quarter, 2020, there was a whopping $33 TRILLION in various retirement accounts. IRAs are king of the hill. There is over $11 TRILLION sitting in IRAs. 401(k)s are almost as large at $9.3 Trillion.

And, these accounts are considered “individual” even when intended as “joint” retirement income. In many, many cases, wives are powerless to control or influence their own retirement income.

This is why I am hoppin’ mad.

That 401k Is Not All His…And Neither Is His IRA

There are some 62 million married couples here in the USA. That is a whole lot of wives who don’t have access to retirement money that was fully intended to be theirs. There is no way to split retirement accounts between spouses. And, the ease and convenience of removing a wife as the sole, primary beneficiary from an IRA should make every wife angry.

Likely an unintended consequence, current tax and retirement laws create significant financial inequities between spouses. The rules are nearly impossible to know and understand unless you love to read tax laws. This is not something every spouse should have to try to figure out. But there are serious implications hidden behind the excuse of “but she signed the form.”

No one is yelling from the rooftops about fixing the financial power imbalance between married couples. It’s an opaque situation and one that is not easy to see. But, if nothing else, Women’s History Month reminds us of the determination, grit, and perseverance women are willing to take on for equality. It’s time to take this gross financial injustice and right the wrong.

A Fun Quiz for Spouses

You may be thinking that this isn’t the most important topic you have to discuss with your spouse just now. I would argue the opposite. But you decide. To see if it should be a discussion, try out this fun quiz I set up recently.

It’s easy. Just ask your spouse the following questions about the retirement accounts in your name. No cheating! Don’t look at any statements or jump online. Just see how much you really know about your spouse’s retirement accounts. While the law considers them to be individual accounts, the intent is that they are for joint use. Good luck!

- How many retirement accounts do I have and how much money is in each account?

- Where are these accounts located?

- How am I investing in these accounts?

- Where do I keep my passwords for my retirement accounts?

- Where can you independently see what’s going on in each of my accounts?

- If you call the 800 number to my financial institution, will they give you information about my IRA or 401(k)?

- Are you the only primary beneficiary on my retirement accounts? Are you sure?

- Can I change the beneficiary on my IRA at the push of a button? Can you change my beneficiaries?

- How do you get informed of any changes I’m making in my retirement accounts?

- If you want to take money out of my IRA, how do you do that?

How Did Dan Do On the 401k Quiz?

I’ll close this post by saying that Dan wants you to know about his results. He got a 10 out of 10. We do work hard at making sure each of us is well informed about the other’s retirement accounts.

But at the end of the day, neither of us has access to the other’s 401k. At any point in time, we can turn off access to our IRAs from the other. And change beneficiaries to anyone we want. If that doesn’t present a financial power imbalance in a marriage, I don’t know what does.

Laws can take a long time to change. For some inspiration, take a look at an article I wrote a few years ago. It’s about how the law came about for at-home moms to save in their own IRA.

Do let me hear how you are handling your “joint” retirement accounts with your spouse…especially when they aren’t joint at all.