Updates and Actions to Take

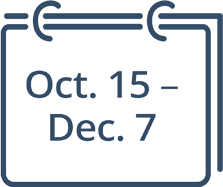

It is October 2022, and your 2023 Medicare Part D Plans are officially open for reassessment. The annual window to take a new look at your prescription coverage is open. Known as the Open Enrollment Period, it runs from Oct. 15 thru Dec. 7. After that, you are stuck with your Part D plan for all of 2023. Even if you find out that your 2022 Part D plan no longer covers your prescriptions. Or that they cost more than last year.

Getting Older Has Its Challenges

A significant percent us who make it to age 65 end up with one or more chronic health problems. By the time we’re 65 and older, some 24% of us will have one chronic condition to manage. And a shocking 63.7% will have two or more. By comparison, only 6.7% of people between 18 and 44 struggle with chronic health issues. And one-third of folks between 45 and 64.

Chronic conditions include these ten common health issues:

- arthritis

- cancer

- chronic obstructive pulmonary disease

- coronary heart disease

- current asthma

- diabetes

- hepatitis

- hypertension

- stroke, and

- weak or failing kidneys

These health problems, and so many more, are made better thanks to the miracle of modern medicine.

Millions now get to live longer thanks to prescription drugs. However, this ability to live longer comes with a price. Often, seniors who don’t have unlimited resources are faced with a steep price tag.

Medicare Part D plans and Medicare Advantage Plans that include a Part D option help manage high costs of prescription drugs. But the plans change nearly everything every year. You don’t want to love your Part D insurance plan after December 31st!

The Rise of Pharma

Earlier generations had few options for dealing with chronic health conditions. Research centered on finding vaccines to cure debilitating diseases. And medical research focused research on the needs on the battlefield – pain reduction and anesthesia.

But with every move forward, life expectancy if you reached age 65, improved. For example:

- If you turned 65 in 1950, on average you would live another 14 years to 79. That’s very young by today’s standards.

- Thirty years later, 1980, life expectancy increased by 2 years. Those who reached 65 had a 50 – 50 chance of seeing 81.

- By 2018, life expectancy was picking up some steam. You could now expect to live 20 years on average to 85. And, about 25% of older Americans could expect to live much longer.

Fast forward to today and with longevity improvements, the odds of you living well into your 90s is real.

In large part, this significant improvement in longer life has to do with the rise of the pharmaceutical industry. A new field of biotechnology was cutting its teeth in medical research in the 1970s,1980s, and 1990s. Amazing research in various areas of medicine resulted in drug development and manufacturing.

Medicine Improved, but Knocked Seniors Out

Seemingly overnight, health issues that plagued older Americans now had a cure. Or at least a way to be managed. Lipitor (1985) was life saving for those with high cholesterol. A calcium channel-blocker drug, Verapamil (1981), was the first of a chain of drugs to manage high blood pressure. And what we see advertised as Celebrex got its start in 1993. It is a powerful drug that helps people with severe osteoarthritis and acute pain.

These drugs grew in popularity. They were prescribed to those who could benefit tremendously—namely, the older population. Yet costs were rising. And rising fast.

Until 2006 Medicare didn’t cover prescription drugs prescribed from a doctor and delivered in a pharmacy. It only paid for drugs delivered when you were admitted to a hospital for surgery. This is part of Medicare Part A coverage. Or, if you received infusions, such as chemotherapy, in an out-patient arrangement. Medicare Part B covers out-patient services.

Older people in need of these new drug marvels couldn’t afford them.

The Medicare Modernization Act of 2003

Congress got heavily involved in the early 2000’s after some 20 years of kicking the can down the road. They simply had to address the cries to address unaffordable prescription drugs for seniors.

In the usual fashion at that time, the debates were long, drawn out, and heated. It took several senators and house reps to cross the aisle to secure funding that would lower drug costs. In the end, no one was really happy. But there was a bi-partisan new law. And everyone could claim some of the credit.

Just about 19 years ago, on December 8, 2003, then President George W. Bush signed the Medicare Prescription Drug, Improvement, and Modernization Act of 2003 into law. Medicare Part D plans would become available for the first time in 2006.

What Kind of 2023 Medicare Part D Plan will you choose?

For 2022, you might have had Rx coverage through a stand-alone Part D plan with a specific insurance company. Or you might have gotten drug coverage as part of a Medicare Advantage Plan. Either option works fine if it’s working for you. Meaning, your plan covers all your drugs at the least expensive premium and price.

But that was for 2022. Now, coming into 2023, everything at those insurers has likely changed. And it’s up to you to see if you need a new 2023 Medicare Part D plan to cover your drugs. During Open Enrollment Period, you can change your Part D plan to a new one. Or change a Medicare Advantage plan to a different one.

From the Part D plan coverage side, the insurers can and do change things such as:

- Which drugs they will be covering in 2023

- How much they are charging for each drug

- What the monthly premium will be

- Are they charging the full deductible or something less

- Have any drugs changed pricing tiers, added restrictions, or now require pre-authorization

- Which pharmacies are preferred vs. standard vs. out-of-network

- And anything else I can’t remember!

Also keep in mind that your own drugs or dosages may be different going into 2023. That can highly influence which Part D plan will work best for you.

Pricing Changes for 2023

In addition to the changes every insurance plan will make, there are other changes coming in 2023. Some of the changes you will see include the following:

First is pricing. Overall, premiums for stand-alone 2023 Medicare Part D may have come down slightly. If the cheapest premium in 2022 was $7.20 in your zip code, it may be $6.80 for 2023. The national beneficiary base is also slightly lower. That cost is used to calculate the penalty for anyone who missed joining a Part D plan on time.

Next is the deductible. A deductible is the amount you must pay first before the insurer starts sharing the cost with you. In 2022 it was $480. In 2023, you’ll pay the first $505 in most Part D stand-alone plans. Some Medicare Advantage plans carry the full deductible, others many choose a smaller amount.

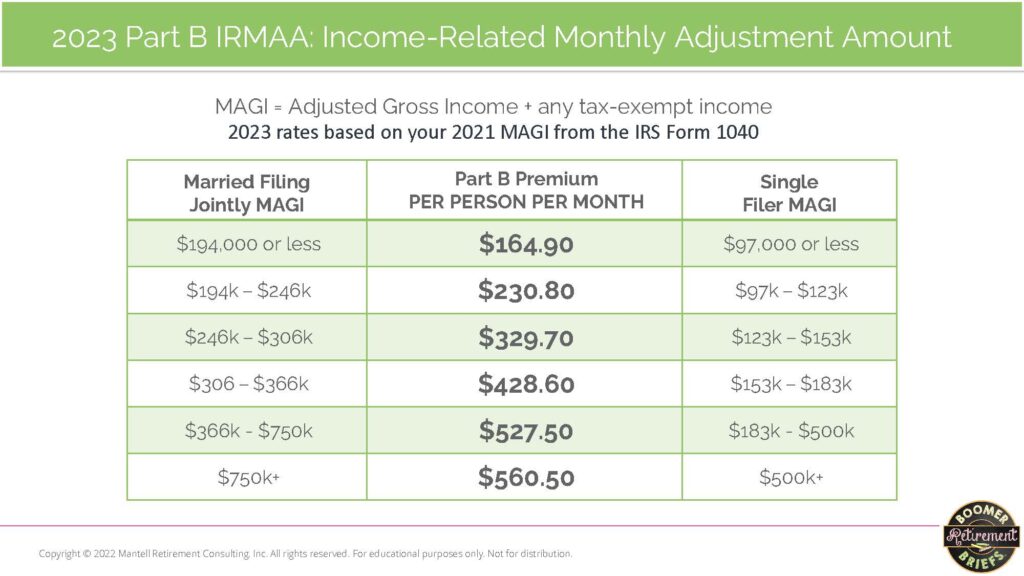

And let’s not forget about IRMAA

This is the Income-Related Monthly Adjustment Amount you pay to Medicare if you are in a high-income household. When your income, as reported on your 1040-SR exceeds the base threshold, you pay additional amounts to Medicare.

Most retirees don’t need to pay anything to Medicare for joining a Part D plan. But if you file individual tax returns (including widow(er)s) and have income above $97,000, you’ll pay a surcharge. You’ll each pay the 2023 Medicare Part D IRMAA if married, filing jointing and your household income is above $194,000.

In 2023, the Part D IRMAA ranges from $12.20 to $76.40. It will be automatically deducted from your Social Security payments each month. Or, if you are not yet receiving Social Security, you’ll get a bill in the mail. Please make sure to pay it timely.

Here is the chart with both income brackets and Part D IRMAA for 2023:

You’ll also pay a Part B IRMAA when you have high income. You can see more details about the Part B IRMAA in this post: 2023 Medicare Part B Premiums Just Released

2023 Medicare Part D Surprises in the Inflation Reduction Act

We had a major surprise in August when President Biden signed the Inflation Reduction Act into law. It includes some major changes to Medicare Part D plans and coverage.

The Kaiser Family Foundation issued a comprehensive report about the drug cost changes within this new law. If you have a few minutes, this is worth a read: Explaining the Prescription Drug Provisions in the Inflation Reduction Act.

While the headlines were about Medicare’s new ability to negotiate pricing (finally!), that provision is unlikely to affect your costs. Rather, many Medicare beneficiaries will see immediate cost relief beginning in January 2023. Specifically, those who use insulin to control diabetes. They will see wide-sweeping cost containment. Insulin and other covered insulin products will have a cost cap of $35/month. That’s a huge deal for about 16 million seniors with diabetes on Medicare.

Gob-smacked by the Diabetes Data

In digging around for some data, I was gob-smacked when I found these latest numbers from the American Diabetes Association:

- Prevalence of diabetes: In 2019, 37.3 million Americans, or 11.3% of the population, had diabetes.

- Nearly 1.9 million Americans have type 1 diabetes, including about 244,000 children and adolescents

- Diagnosed and undiagnosed: Of the 37.3 million adults with diabetes, 28.7 million were diagnosed, and 8.5 million were undiagnosed.

- Prevalence in seniors: The percentage of Americans age 65 and older remains high, at 29.2%, or 15.9 million seniors (diagnosed and undiagnosed).

- New cases: 1.4 million Americans are diagnosed with diabetes every year.

- Prediabetes: In 2019, 96 million Americans age 18 and older had prediabetes.

Unfortunately, only people on Medicare get the $35/month cap. Covering younger folks got cut from the law during negotiations in Congress.

Also in the new bill, Medicare beneficiaries will no longer pay for recommended vaccines.

Beginning in 2025, all Medicare beneficiaries will have an out-of-pocket cost cap of $2,000, including the deductible.

Using GoodRx, Singlecare, AARP’s Discount Card, etc.

I often get asked if these new discount cards are available if you also have a Medicare Part D plan. The answer is, “Yes, sort of.” You’ll have to make a choice at the pharmacy. Will you use your Part D Rx card and pay that price? Or will you pay cash and use a discount card instead? It’s a one or the other, not a double dip.

Most folks who have a Part D plan would buy a one-off prescription at a pharmacy using their Part D coverage. But, what if they find it’s cheaper (and maybe a lot cheaper) using a discount card?

Tell the pharmacy folks you want to buy this particular Rx using a discount card. The key is to find this out before placing the order. You’ll need the pharmacy to change its default billing.

I’ve only started looking into these cards, as I don’t typically need any one-off Rx’s. But I’ll do some research in 2023 and post what I find. Meanwhile, you can take a read about the AARP program here. And if you have had any experience using a discount card, please let me know!

Your Action Plan during the OEP

Keep in mind you only have about 7 weeks to get your Medicare Part D plan in order for 2023. The door closes and locks on December 7th. The easiest way to reshop your drug plans is to follow these steps:

1 – Set up your My Medicare account if you haven’t already. This is where you can store your current drugs for easy comparison shopping each year.

2 – Use the Medicare “find plans” tool. You can comparison shop for your stand-alone Part D plans and compare the Medicare Advantage plans that cover your specific drugs.

Set up a spreadsheet or use a big piece of paper to keep track of your various choices.

3 – Once you choose your new drug plan, go directly to that insurance company’s website to sign up. Or call their 800 number. Your 2022 Part D plan will NOT be canceled until December 31st. The new plan automatically starts on January 1st.

4 – If you have questions or concerns, contact your local SHIP volunteers. They really do know a lot about your local choices.

Last, but Not Least…

Once you have your new 2023 Medicare Part D plan in place and receive your Rx card, make sure to contact your doctors (all of them!) and the pharmacy you will be using. They need the new card to keep your refills coming.

If you’re feeling frustrated with your results, know you are in good company. Earlier this year I wrote a series of articles for Retirement Daily about the drug cost research I worked it. In a nutshell, I was shocked and disillusioned. Even when you only have a couple of generic prescriptions, the hidden costs are inexcusable. Read the articles here.

This process can be rather painful. But it is necessary. Depending on the drugs you take, the costs can be wildly different. Take the time to research your 2023 Medicare Part D options.

Then, mark your November 2023 calendar now with a reminder to do the same thing all over again this time next year.

Happy shopping!