Every July 4th weekend Dan and I spend at least one full day going through our family finances and our plans for retirement. We push everything else aside—laundry, cleaning, cooking, children—and dive in to money topics. We get out snacks: chips and salsa and guacamole this year. And, importantly, decide where we’re getting take-out for dinner. Then, as in other years, we start out with this question: “Do we need a million dollars to retire?”

Standing on the cliff looking down

2020 is a big milestone year for Dan and me. One of us turns 60. The other will reach 59 ½ and can now break into their retirement piggy bank with no early withdrawal penalties. And, not to throw Dan under the bus, but he is much older than I am!

It’s quite shocking to be here, nearly at the point of retirement. It’s like we’re standing high up on a cliff looking down into clear blue water. Is it time to jump? No, not quite yet. Is it going to be scary to jump? Yup, pretty scary. Is it dangerous? Not if you’re wearing a parachute!

We do realize our options are starting to narrow down to really be ready for this upcoming major life event. Especially if we find that we need a million dollars to retire.

Digging out all those documents

The first step in our fourth of July finance fun bonanza day was to dig through our files. Fortunately, I am organized, so it was pretty easy to pull out the folders of all our accounts. We have everything available online as well. But for us, it’s much easier to pour over numbers and figures with paper and pencil in hand.

We notice right off that we have a lot of different accounts. We’ve been saving now for 40 years. Boy, did those years fly by fast! Did you know that when we got our first jobs and started saving, the 401(k) wasn’t even invented yet? How crazy is that to think about?

We’ve come a long way since 1980. We’ve been able to take advantage of saving in many different types of retirement and investment accounts. But, now, we need to think about what it will mean to live off these accounts in retirement. And we just have too many accounts between us. And they are scattered around in too many different places.

It became readily apparent that one of this year’s to-do’s was to make a real effort to streamline things. And, it is not so easy cleaning financial stuff up.

Making guacamole

Our goal was to consolidate every account we could. With a total of 17 different accounts, we wanted to get down to 9 or 10. We had to start mixing some accounts together. Dan is better at this than I am. I really like to see each bucket individually.

So, it helped to think about consolidating accounts much like making a big bowl of guacamole. Start with the main ingredient: avacados. Those are your 401(k)s and 403(b)s. Then add tomatoes (IRAs), onions (taxable accounts), and sour cream (pensions). Top off with some lime juice and salt for the final taste test. In really good guacamole, you can still see all of the individual ingredients. It’s just that they combine to make something even better than their individual parts.

Same thing for our retirement accounts. Each individual account is important. But we’re soon going to have to create a paycheck from all those ingredients. It’s just more practical and effective to mix them together. We’ll make fewer mistakes when it comes to drawing down our hard-earned money in a tax-effective way, too.

Adding up the numbers

Now that we had a plan for better organizing our financial accounts, it was time to move on. To figure out if we need a million dollars to retire, we’d have to add up some numbers. This is more complicated than just looking at your statements to see how much you’ve saved.

It’s the spending side that really matters. When figuring out how much you’re going to need for retirement, the key number is how much you spend.

Everyone has a different way of keeping track of household spending. I happen to use a simple excel spreadsheet. I love a good database where I can sort large amounts of data in lots of different ways. And add everything up. It’s hands on and tangible. In about 4 seconds, I know exactly how much we spend by month, by category, and for the year.

A stark reality

With excel database in hand, Dan and I could now talk about our spending. Questions like, “We spent how much eating out?” And, “What did we buy at Home Depot that costs so much?”

The big question, though, was, “Do we think we’ll continue spending at the same rate after we stop working?” That question makes for a lively discussion with lots of different answers.

We refilled the guacamole bowl and talked for hours about these kinds of topics:

- How much we will really be willing to cut back? (Not at all.)

- Will we sell the house and downsize again? (Not initially.)

- How much travel we want to do? (A lot more than we do today.)

- How much more will we have to spend on health insurance once we get into Medicare? (A substantial amount more than today. Ugh.)

- What sort of financial support do we want to give our girls? (A lot less than today!)

Afterwards, we came to an interesting conclusion. We will likely spend as much in retirement each month as we are while we’re working. And it’s highly likely we could spend more.

It’s one thing to talk about it. It’s quite another to see it all on doodled on paper. It was a stark reality.

So, do we need a million dollars to retire?

Well, maybe. But we have to first think about where our income will come from once we get to retirement. How will we create our own paychecks? Dan’s solution is always that I should work longer. He thinks he’s funny. My solution is that Dan should work longer. We’re somewhat at a standstill with these “suggestions” and do get a big laugh out it all.

The big decision is really about when we should each claim Social Security. The longer one waits – up to age 70 – the more monthly income one receives. So, that’s a possibility for one of us. Not surprisingly, we each vote for the other to wait until 70!

(Make sure you’ve signed up for your most current Social Security statement at SSA.gov.)

We also need to think about how much cash our investments can generate each year in retirement. We think we’ll live a long time. Managing the drawdowns from our accounts will be critical to manage. We use the IRS Uniform Lifetime Table as a good way to plan our withdrawal rates.

The financial industry has made all of this planning for retirement super complicated. And, if you happen to have a lot of wealth, it can be more challenging because you have a lot of different goals. But, for most of us, it’s really not that hard.

A place to start

Just start with your monthly spending. Take that amount and multiple by 12 for an annual amount. Multiply that by 30 years. That will put you in the ballpark for how much you’ll need available throughout retirement.

Now, the economists and financial experts will be screaming at this point. You’re forgetting about inflation! You didn’t account for investment growth! What about taxes? But, I’m really not. I simply want you to see a starting point so you can answer the question: do I need a million dollars to retire?

And, your answer completely depends on how much you’ll be spending. It’s critical to start with spending. Regardless of your health, or where you live, or all your retirement dreams, your electric bill has to be paid. Your health insurance has to be paid. And, you’ll need to eat. All that and much more must be paid each and every month in retirement. No exceptions.

So, make it easy. Start with simple math based on your own spending.

A few examples

To get you started, here are a few examples – not adjusted for inflation – to show:

- How much your spending drives your retirement financials.

- How much you’ll get in Social Security determines how much you’ll need to pull from your own hard-earned savings.

- If you’re part of a couple when you start retirement, one of you will become single at some point. How much you spend will likely stay about the same as when both of you were alive. But, your income from Social Security will drop by one-third to one-half.

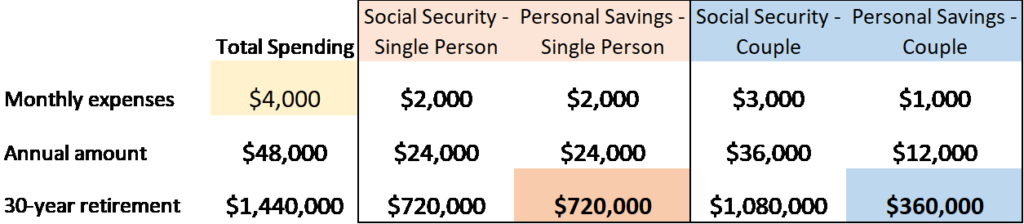

Case #1

Here’s a look at the simple math for someone who estimates they’ll spend $4,000 per month. Assume they receive a Social Security benefit of $2,000 per month. They’ll need to pull $24,000 per year from their own personal savings to meet their spending.

So, this person needs about $720,000 over the course of their retirement from their own savings. But a married couple needs considerably less—because both receive Social Security benefits.

Case #2

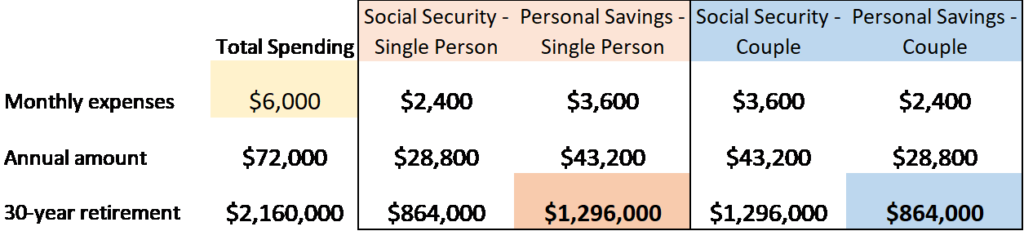

Now, let’s look at someone who is going to spend more: $6,000 per month. Assume this is a higher-income earner, so their Social Security is a little higher. They have to pull $3,600 from their personal savings to meet their spending need each month.

Here you can see that they’ll likely need about a million dollars to keep up with their spending. And, that is after accounting for Social Security. Again, with two Social Security payments, a married couple needs less than a million dollars.

Case #3

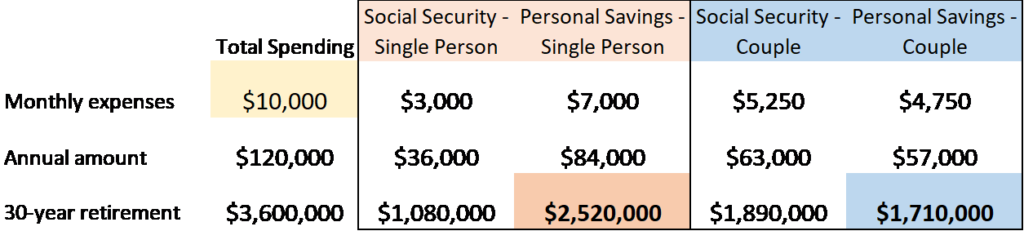

And, if someone is planning to spend even more, they’ll need even more. In fact, with higher spending comes much higher savings requirements. It’s more like two million dollars for these folks.

This is just the beginning

The reason this is an important exercise is to see on paper that retirement is going to be expensive. And, you have to rely on yourself to pay for it. There is, of course, no guarantee that you’ll live for 30 years in retirement. But a whole lot of folks do just that.

It’s important to keep in mind a few important truisms:

- You don’t necessarily need a million dollars before you retire. The savings you have at the beginning of retirement plays two important parts. First, some of your income will be pulled to meet your spending needs. And second, the rest remains invested. A portion of your assets should remain in the equity markets for most of your retirement. A 30-year horizon is a long-term game plan.

- Inflation will cause prices to continually increase. A 3% increase in annual inflation causes prices to double in 25 years. Again, keeping your savings invested for some growth is key to keeping pace with rising costs.

- Retirees often have to make tactical shifts in their plans. Something unexpected comes up, so they need to be flexible and adjust accordingly. Trade-offs are as much a part of the retirement game as investing in a well-diversified portfolio.

Try your hand at seeing how much you’ll need for retirement. Use the calculator on your phone or set up an excel spreadsheet. Or, try this NerdWallet calculator. It’s pretty interesting and just takes a minute to see where you stand.

Holy Guacamole!

Right about now, you might be wishing you hadn’t stopped to read this post. Or, you might be glad you did. It’s just important to be preparing for retirement. Meaning, you need a plan for when your current paycheck stops. A good place to start might just be asking if you need a million dollars to retire.

Before you start pulling together all of your information, grab a bag of chips and a bowl of guacamole in one hand. And a margarita in the other!