(Part 2) There’s a 9-month retroactive period. Not a 6-month look-back

So many older workers are caught off guard when it comes to signing up for Medicare Part A. These are folks well past age 65. Surprise! Part A comes with a retroactive period. And it has a nasty effect on HSA contributions.

The vast majority of folks I work with have continued employment after age 65. Or their younger spouse is still working and providing the health insurance. Almost all have made mistakes with their HSA contributions in one way or another.

Unfortunately, and unfairly, it’s a big mess out there when contributing to an HSA after age 65. And then trying to coordinate their entry into Medicare correctly.

This is part 2 of a series on the complexities of HSAs and Medicare. You can read part 1 here.

Working After Age 65? No Need to Start Medicare

Baby Boomers have to wait longer to get their full Social Security payments. Instead of a Full Retirement Age of 65, many have an FRA of 66 plus 2,4,6,8, or 10 months. And for those born in 1960 and later, their FRA is age 67. They can claim earlier than FRA but will get a reduced monthly payment.

When Boomers stay on the job, they get their health insurance from their large employer. (A large employer has more than 20 employees.) Therefore, there is no need to enroll in any part of Medicare. They have full health insurance from the job.

All these workers over 65 report the daily onslaught of Medicare mail from seemingly every insurer on the planet. They think they must enroll in Medicare or face steep penalties.

But YOU DO NOT NEED TO ENROLL IN MEDICARE. Really, really.

Unless you work for yourself or a small employer with fewer than 20 employees. In that case, the rules are different. You must enroll in Medicare Part A and Part B by the month of your 65th birthday.

Otherwise, all health insurance claims will be paid by the employer plan. Just like when you were 64.

Choosing a HDHP and Funding an HSA?

Regardless of your age while working, or the age of your spouse, you can stay on the group plan. Today, many workers choose a high-deductible health plan (HDHP). And they get a companion Health Savings Account (HSA).

These folks generally fully fund their HSA. It’s part of their planning strategy. They’re socking away tax-advantage money for future healthcare needs in retirement. They can contribute up to the maximum as an individual. Or up to the family maximum if covering themselves plus at least one other person.

Eventually, when a worker decides to retire, they’ll need to coordinate applying for Medicare with losing their company plan. Since they’re now older than 65 when applying for Medicare, their HSA contributions must stop.

Under the law, an individual cannot both fund an HSA and have any Part of Medicare. In fact, they must know to stop HSA contributions six months before applying for Medicare.

The key word is “applying.” You apply for Medicare three months before your target starting date. This allows Social Security time to set up your account. And to calculate your Part B premium.

Unknowingly to the older worker, this also started their Part A clock six months earlier.

Everybody Thinks They Understand the “6-Month” Medicare Part A Retroactive Rule

But I can assure you, they do not. This includes HR and benefits folks, million-dollar earners, university professors, lawyers, plumbers, middle managers, and CPAs. I might even bet the representatives in Congress who wrote the law don’t understand how to apply the rules.

The best way to explain what happens is the following. There is no 6-month retroactive rule the way you and everyone else thinks. If someone is going to start Medicare on October 1st, they assume their Part A retroactive period started on April 1st. This is totally reasonable. Yet they would be wrong.

It’s true the Part A retroactive period is technically 6-months. The issue is from when.

It’s not six months from the start of your Medicare Part A. The clock starts ticking six months from your application date for Part A. There’s only one way to start all the pieces of your own Medicare packet on time. That is to apply three months before you need it to start.

That makes the retroactive period 9 months. Not six.

More Unwelcome Surprises

The application you fill out may only be for Medicare Part A. Or you might need both Part A and Part B, so you apply for both. In either case, stop HSA contributions six month earlier.

But what if you only want to apply for Social Security retirement benefits? You are still working and don’t need any part of Medicare. Well, unbeknownst to you, you also automatically applied for Part A. And it will start 6 months earlier than your Social Security application date.

No, I’m not kidding. And it tends to hit those 70 and older the most when they are still working.

All this is to say that your Part A retroactive period starts months before you expect it to. And, therefore, contributions to your HSA should generally stop 9 months prior to applying for any benefits. Either Medicare or Social Security.

But only if you are older than 65 ½. If you apply between 65 and 65 ½, the retroactive period only goes back to age 65. You can’t have a retroactive start to Part A if you aren’t even eligible yet.

And Still More Nuances

People who are working after age 65 for a large employer get to delay Medicare. It’s really that simple. You get to delay signing up for all parts of Medicare until you retire. Without penalty as long as you are enrolled in the group plan.

This rule also applies to your spouse. If you cover your spouse on your large group plan, they too can wait to apply for Medicare. Or, if you are covered on your spouse’s large group health insurance plan, you don’t need any part of Medicare.

However, if you live with a partner, it is likely they will not be covered on the large employer group plan. Another bit of insanity with the Medicare law is that it carved out non-married partners. In this situation, the nonemployee partner must enroll in Medicare Part A and Part B for age 65. Their Medicare needs to start the first day of their 65th birthday month.

Then, the employee can cover them on the group plan. But the group plan only pays after Medicare pays claims first.

Can You Enroll In Just Medicare Part A Anyway?

Some people do decide to enroll in Medicare Part A even when covered by a large employer health plan. They still have to reach age 65 first. Then can turn on Part A. What they’re looking to do is add some Part A coverage—just in case. An insurance to their insurance.

Medicare Part A covers costs for hospitalization and follow-up skilled nursing care. It may pick up some of your costs if you end up in the hospital. And since there is not a monthly premium to pay, it often seems like a good idea. (Your Medicare FICA taxes pre-pay Part A.)

An advantage to enrolling in Part A even if you have coverage from your employer plan is you get your Medicare number. That will come in handy if you lose your job and group coverage unexpectedly.

However, there is a problem for those contributing to an HSA. Having any part of Medicare eliminates their eligibility to contribute to an HSA. Therefore, if you’re adding Medicare Part A—just because—at or around age 65, beware. Make sure to stop HSA contributions the month before your 65th birthday.

An example: Starting Medicare after age 65

Let’s see what happens with Sally Snowflake’s retirement plans. (Sally is my alter ego when coming up with examples.) Sally is turning 67 and will be retiring soon. Her Medicare effective date is November 1st.

While still working Sally has a high-deductible health plan and contributes to her HSA. What she needs to know and plan for is when she must stop making contributions to her HSA. Since she’s older than 65, it’s easy to end up with ineligible contributions. But when exactly does she need to stop funding her HSA?

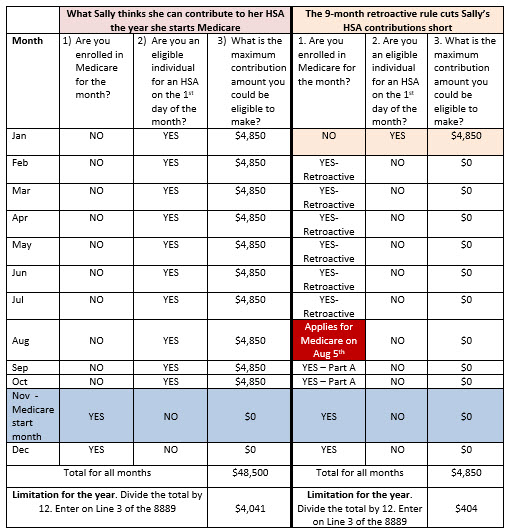

The best way for Sally to figure this out is to use the worksheet in IRS Form 8889. The table below illustrates this form and how Sally will fill it out.

To give you an example, I’ve set up two sets of columns. The left set shows what Sally, and most workers, think is going on the year they are entering Medicare. The right shows how the IRS rules really work.

The Year Sally Starts Medicare

What is Sally Running into with Part A?

Somehow, before filing her taxes, Sally needs to magically know her when Part A really started. Even though she won’t be in Medicare until November 1st, her Part A began on February 1st. This situation can be chalked up to the retroactive rules:

- For Sally’s Medicare to in place for November 1, she needs to apply in August.

- Her Part A unknowingly started nine months from her target date (November). Or six months before applying for Medicare (August).

- On the other hand, her Part B will start exactly when she thought it would. On November 1st. Oy.

Furthermore, she would only find this out when her Medicare card arrives. It will read:

- Part A, effective date February 1, current year

- Part B effective date November 1, current year

Let me tell you, this is a shock to almost everyone.

The Net Result of the 9-Month Part A Retroactive Period

In Sally’s case, she contributed $4,041 to her HSA. But she’s only eligible to contribute in January! She should have only contributed $404 for the year she’s entering Medicare.

Oops. This is going to be a problem.

She’s made an over-contribution of $3,637. It’s likely she won’t realize this until the following year at tax time.

And she’ll need to take steps to fix this situation. She has effectively not paid income tax on $3,637. That’s going to come with a penalty.

Fortunately, Sally Gets A Do-Over. If She Finds Out in Time

The rules found in IRS Publication 969 for Health Savings Accounts provide relief if you’ve overcontributed. You should also work with your CPA to file the right forms. In general, you can take the following steps:

- Withdraw the excess/ineligible contributions from the HSA by requesting a withdrawal from the HSA custodian bank.

- Withdrawals must be made by that year’s tax-filing deadline, including extensions.

- Do not claim the excess money as a tax-free distribution. This transaction is only a corrective withdrawal. And it is fully income-taxable money.

- Any earnings attributed to the ineligible contributions must also be withdrawn. Include them in “other income” on that year’s tax return.

HSAs are great – But Employees Older than 65 Need to Stop Contributions Before Well Medicare Begins

There is no end to the layers of complexity hidden beneath HSAs. Many more near-retirees are using them as a key planning strategy.

But dang. Things sure do get complicated in transition years.

It’s critical you stop contributions—yours and your employer’s—9 months before your Medicare starting date. But only when applying well after age 65.

The key to success is planning backwards. Lock in your retirement date. Make sure to identify your exact entry date into Medicare. Then count backwards.

- File your application for Medicare Part A and B three months before your Medicare starting date.

- Six months from the application date is your Part A effective start date.

- One month prior to that – last HSA contributions can be made.

See how easy and obvious it all is!