Retirement means freedom from a lot of the hustle and bustle of decades of a fast-paced life. It’s time to take the exit ramp from that overheated, super-highway of life. These are the best years of our lives. And, we’ve earned the time to take it easy, and ease off the gas. Sounds idyllic, doesn’t it? But it turns out that taking it too easy can be a problem. Especially in terms of the ever-increasing complex financial industries. And, in regard to our credit score and credit history.

Turns out, we’re going to need to keep a close watch on our credit all throughout this modern era of retirement. Seems that everywhere we turn these days, someone wants to know our credit score. And, if it’s a crappy score, we won’t get new loans or credit cards. Or we’ll get them, but with much higher interest rates.

Even continuing to get favorable rates on our homeowner’s insurance policies depends on good scores. As does getting into the nursing home or continuous care living arrangement we want.

Realities of the financial system today

It all used to be so easy. I’d babysit on Friday and Saturday nights. I got paid $1.25 an hour. Some families would round up to the next dollar or give me an extra buck for a tip. After spending a good 12 hours babysitting little children, I’d haul in a whopping $20 bucks. In cash.

Then, when I wanted something, I’d go buy it. In the store. With cash.

Today, that option is all but gone. No store wants cash these days. And, the snarly looks when you pull out cash are less than necessary. My big ah-ha that the world had really and permanently changed was when McDonalds started taking debit and credit cards. For a $3.87 burger and fries. Really? You have to charge your burger at McDonalds?

Why, yes you do these days. Or better yet, use your ApplePay or GooglePay. Or something else in your digital wallet.

Cash is dead. Credit scores critically important

And so, here we are after a great, global pandemic. Most now shop for nearly everything online from their couch. It all seems so easy. Scroll around on your favorite websites, choose items for your cart, then push the “click-to-buy” button.

But none of these online options would be available to you without an underlying good credit score. All of these cash-less purchasing and payment options are linked to a credit card. Yet, to get a credit card with the best interest rates, you need some credit history. To build a really good credit score, you need a long run of a very good payment record. And, the cycle gets more and more complex all the time.

So, we think we can exit this crazy super-highway as we move into retirement. But it simply is not possible to take a step back. In fact, having an excellent credit score is more important than ever.

Changes to the credit score algorithms

How exactly our credit scores are determined is partly a mystery. And, the definition of good, better, best credit changes frequently. Today, the crediting agencies score our credit worthiness from 300 to 850. “Very good” credit scores start at 740. You need to reach 800 or better to be in the “excellent” category.

So, it is critical for every individual – whether single or married – to have their own good credit score. You cannot get loans and other credit for your online shopping if you don’t have your own score. Married women, especially need to make sure they are independently maintaining their own good, high credit score. To help understand what goes into the scoring algorithms, here are some helpful hints:

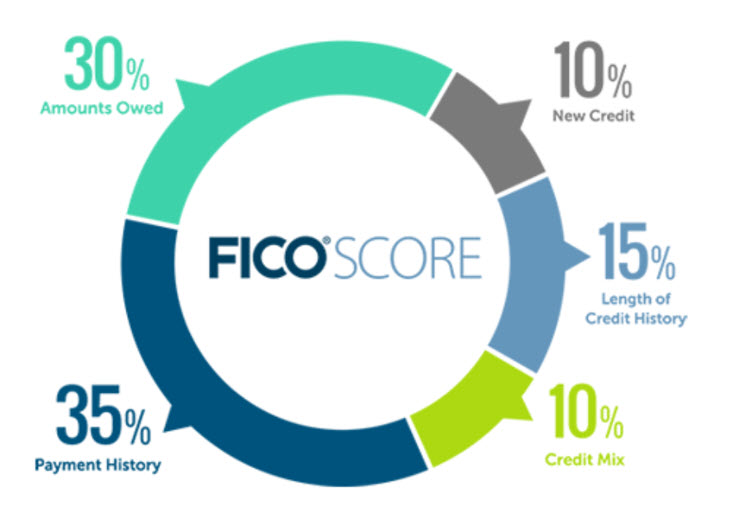

35% of your credit score is based on your payment history.

This is the biggest factor going into your score and the most important. Bottom line, credit scores indicate to a potential creditor how likely you are to make your payments on time. You wouldn’t want to get late payments from a renter or a friend. Those who lend you money – and that’s every credit card in your wallet – want to be paid back timely. Every month. Every year.

Length of credit is not as important as you think.

Most think young people have low credit scores because they don’t have a long enough history with credit. But only 5% of the logic is based on length of credit. It’s not nearly as important as paying your student loans on time and keeping your utilization low.

20% of the credit score is split between credit mix and new credit.

· It’s not a terrible thing to open new types of credit. You just don’t want to open up too much all at once. This is where Boomers and older folks have a leg up. Over decades, we’ve assembled a good mix of credit (mortgage, paid-off student loans, paid-off car loans, credit cards, store cards, etc.). And we don’t open a lot of new credit accounts. But, if you’re signing up for Apple Pay or Google Pay, that’s a new type of reportable credit. Apple Pay reports to one of the credit bureaus. PayPal reports to others.

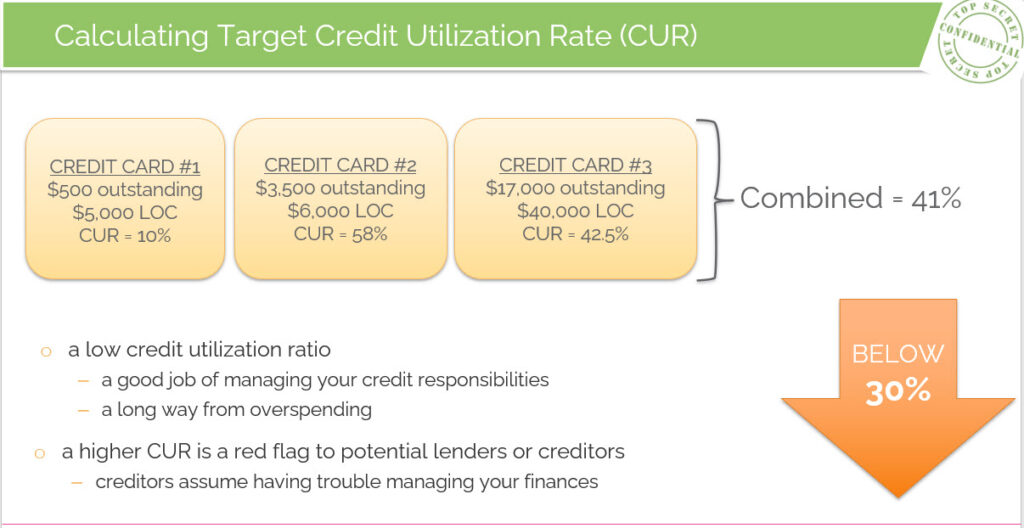

Credit Utilization: a newer concept necessary for a good credit score

Another big chunk of your score is based on your credit utilization. In fact, 30% of your score is based on what creditors call “amounts owed.” This is percentage of how much you owe versus how much you have to borrow.

There are 5 key considerations creditors use when assessing your risk level and if they want to lend to you:

- Total amount owed

- Amount owed on different kinds of accounts

- Number of accounts with outstanding balances

- Credit utilization ratio on revolving credit

- Installment loan balance vs. original note

Long-term loans like mortgages and student loans are in one category – the really serious category. You really have to pay these loans in a timely manner.

What lenders look for is how stretched you are on your credit cards. That’s #4 on the list. Ideally, you never want to use more than 30% of your revolving credit available.

Here’s how I teach about this topic:

Why I am so hot on this topic? Missteps and marriages

The financial and credit systems have become more and more part of our financial success. And failures. It’s no longer just an “oops” if you make a payment misstep. Or max out a credit card. The speed of technology is making it impossible to make mistakes. And, the lack of transparency makes it challenging to know what’s going in to create credit scores. Plus, the rules change all the time.

And, married women need to understand how important it is to build their own credit. Independent from their husband or wife. For those of us who set up financial households decades ago, it may be time for a major financial renovation. Many choices throughout retirement will depend on access to lines of credit. Make sure you are outfitted with your own good credit score.

If you’re thinking it’s too late, let me assure you it is not. Before any married woman becomes a widow, it’s essential to have financial assets, accounts, and credit in her own name. It will help deal with financial needs during turbulent times after losing your spouse. Being prepared for financial realities needs to be a top priority. Otherwise, it’s like leaving the house braless! And that’s not good for anyone.

A few interesting items on this topic

First, take a look at the attached resource document I pulled together for you. There are several important steps to take years before you reach retirement to secure your own strong credit score.

Download your copy and take a look at the key action steps you can take to build a strong credit history and maintain your own good credit score.

Next, check out a few other good resources. Make sure you are fully up to speed on the latest and greatest information about credit history and credit scoring. It’s worth the time to be in-the-know:

- Who has a better credit score, men or women? You may be surprised at the answer.

- Do you really understand your credit? Check out this terrific article.

- What if you’re divorced? How is your credit impacted?

- More on the credit utilization rate. See how it all works in more detail here.