If you receive an early retirement offer from your employer next week, are you prepared to make such a big financial and personal decision?

Getting such an offer may be a good thing…or a whopping insult. The reality is that many employers are using early retirement offers as a way to ease us older folks out of higher paying jobs.

However, many Baby Boomers and older GenXers have not saved enough for retirement, and the idea of taking an early retirement offer isn’t on their radar.

Rather, they are counting heavily on these high-earning years to save more, climb out of debt, and enjoy some of their new-found freedom of an empty nest. Retirement is still off in the distance.

A Common History

If you look back on those early years of building a career, it’s no surprise that many people are ill-prepared to pay for retirement.

First, we had to pay off student debt, which many shouldered well before it became today’s national crisis.

We bought houses, and maybe over-extended ourselves with mortgages that were too pricey for our wallets.

We raised a new generation of children who are the rising adults of the Millennial generation, and paid for some or all of their college tuition. Plus, many of us are taking care of parents, older family members, and friends. None of this is cheap. And retirement seemed so far off when we were 25, 35 and 45. Today, in our 50s and early 60s, we are facing retirement reality: Retirement is getting closer, and there’s only another 10 to 15 years to super save for it.

Employers Want Younger, Hipper, Less Expensive Employees

Early retirement offers are a sign of business and industry transition. It’s a trade of older, often more expensive employees, for younger, hipper, and lower paycheck employees. It’s hard to get your arms around this situation when you’re in the prime of your career. Think about what you would do if you ran a company that needed to be profitable. Would you pay older employees to work well into their 60s or even 70s? More to the point, will your current employer really want you around as you approach your 60th birthday? How about 65? That seems to be a thing of the past.

There are always certain professions that lend themselves to keeping and valuing older workers such as high-ranking lawyers and tenured university professors. Small business owners can call the shots on when and if they want to retire. But, the vast majority of employees don’t have the option to name their retirement date. When employment laws changed to lift mandatory age-65 retirements, it opened a window for later retirements AND early retirement offers.

A Newly Minted Workforce

It’s a different world today than in generations past. Employers look to younger employees, not only because they get paid less and their benefits are not as costly, but because they have fresh ideas and the high-tech skills that are critical for long-term success. They really can walk and text at the same time. Since they are likely your children, it is a good thing that employers want them!

As a result of the current environment, it’s probably a smart idea to consider the possibility that you might not be able to continue to work at your job with your current employer as long as you had thought. Many employers are offering employees in their 50s and 60s early retirement offers and pretty tempting packages. If you suddenly find yourself with just such an opportunity, are you prepared to make a decision?

How Two Women Looked at their Early Retirement Offers

I interviewed two women who faced the situation of early retirement offers. Neither was of “retirement age” and were surprised to find an early retirement offer in their inboxes. Both in their 50s, they had to make serious financial and career decisions. You can read about their journeys, the approaches they took to come to a decision, and their outlooks for their next 15 years at TheStreet.com, a daily financial website, or check out my blog on the topic.

Isn’t Taking an Early Retirement Offer A Big Risk?

When you think about it, how big a risk would it be to leave your job? What are some of the most important challenges you’d have to face? Even if you make it on the job until age 65, you’ve likely got decades of life in front of you, and key situations to consider, including:

Longevity…

The average life expectancy for healthy 65-year-olds is long. From the Society of Actuaries, a woman’s average life expectancy is about age 90, and they have a 25% chance of living to 96. Men’s numbers are 3 years younger. If you get an early retirement offer from your employer at age 55, you could easily be looking at a 40-year era called “retirement”. Unless you’ve got millions stock-piled in the bank, your security could get wobbly in your 80s and 90s.

…and Healthcare Costs in Retirement

Health care costs in retirement will be significant. You can’t access Medicare until the month you turn 65, What will you do for coverage if you take an early retirement offer? Paying for health insurance and health care needs is a growing concern. A study from the Nationwide Retirement Institute in June 2018 found that 73% of older adults say “out-of-control health care costs” is one of their top fears in retirement. The report revealed that 64% of future retirees say they are “terrified” about what health care costs may do to their retirement plans. If you are relatively healthy today, it might be wise to earmark about $1,000 per month per person for health insurance and other health care expenditures in retirement. If you have a chronic health condition, budget more. That’s a lot when you don’t have a paycheck coming in the door.

If you get an offer to retire early, there are other financial risks to consider as well. Is your mortgage paid off? Are the kids through college? Were you planning on travel, a new car, house renovations? Have you really saved enough for a “normal” retirement, let alone an extra 10 years?

Early Retirement Offer: It’s More Than About the Money

While there are serious financial considerations to any decision about leaving your job, there are also non-financial opportunities that rarely become available to grown-ups. You won’t be getting any younger and there may be things you hoped and wanted to do. Having the chance to go on sabbatical or just break out of that routine (or rut?) you’ve been in for the past 20 or 30 years may look appealing.

It’s easy to fall into complacency when you’re a long-timer on the job. You may no longer be looked at as a candidate for promotion. Your bosses may be getting younger and less experienced in every reorganization. The environment may not be what it once was, but you feel you have more to do and give. An early retirement offer may be an incredible opportunity for you. Perhaps unexpected, but welcomed. From many who have faced the decision of “do I take this package or don’t I?”, they say that the real gift of an early retirement is time.

You’ll have time to think about your options. You can remember and celebrate your past successes while trying new things. Take the time to make thoughtful decisions and rebuild faith in yourself and your abilities. Not a bad option when the horizon is still so far in the distance.

Plan for New and Exciting Opportunities at 50

Get ready for opportunities that could be coming your way if you take an early retirement offer. If you aren’t thinking about the possibility that you could lose your job, getting an early retirement offer email may be a bombshell. And, other life events can get in the way of your career plans. What if your mom or dad need care-giving and you have to step off the full-time job to help? Have you considered your role if your spouse or partner becomes ill? What if you want to pick up tuition costs for your kid’s college? We all know people in these situations, so thinking through how ready you are to handle an early retirement offer is a worthwhile exercise.

One idea is to start “pre-paying” your retirement years. After you’ve put the kids through college, why not take the former tuition money and bank it for your first year of retirement? Read more about this idea in my January blog on New Year’s Resolutions. Another is to use age 50 as your mile-marker. Take a hard look at your financial picture and make strategic decisions around debt repayments and your mortgage. The earlier you start, the more prepared you’ll be.

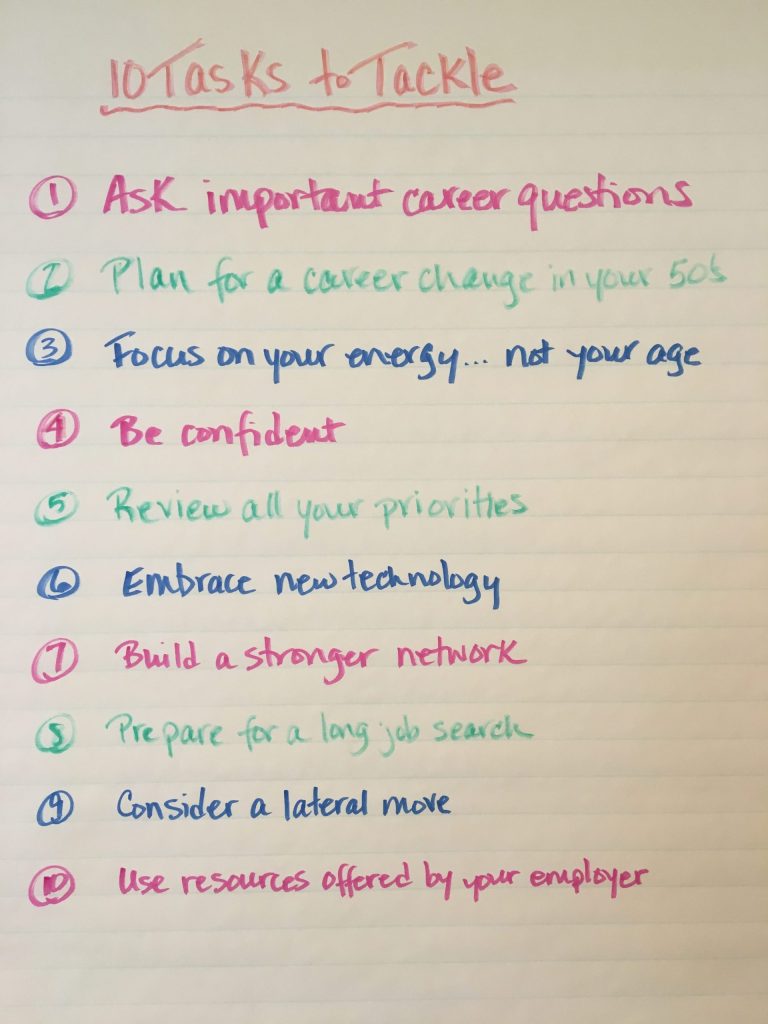

10 Tasks to Take On (even if you don’t get an early retirement offer)

Regardless of your level in an organization, you may be on the receiving end of the latest variety of the pink slip. An early retirement offer generally comes to all employees in a certain age band, even if you’re a senior leader or executive.

Prepare yourself to take advantage of a personal sabbatical. Think about what you want to do for career number two. Below are 10 critical tasks to take on when thinking about your future. These are helpful hints from others who faced the early retirement decision. You would be well-served to get out your to-do list and tackle these tasks before an early retirement offer appears in your inbox.

The first 4 tasks

- Ask yourself three questions: What do I really want? If I don’t have it all, why not? Have I taken control of my career or have I been content to let someone else choose the path for me?

- Your answers may surprise you. Maybe you want to take on more responsibility and have a bigger job. Leaving your current job doesn’t mean you have to settle for something less.

- Don’t be afraid to take a career leap in your 50s. There is no job security.

- While many employers may want younger employees, smaller businesses, local community colleges, and not-for-profits may feel they struck gold when you bring your experience to the table.

- The job market is receptive to your energy – not to your age. Prepare an “ageless resume” and focus on what you’ve done in the last 5 – 10 years.

- It’s easy to forget all you’ve contributed to your field. Take the time now to create a biography instead of a resume. Work with a career coach if you prefer more structure and a sounding board.

- Be confident. You have experience, skills, knowledge. Not everyone can do what you do. If you’ve raised a family, you now have freedom, wisdom and leadership. Put it all out there!

- Try the 3-minute Fascinate personality test to see how you unique you really are. Be different. That’s what you have to offer.

Four more to consider

- Review your priorities – family, financial, professional, personal…fun. Where do you want to spend your time and resources now?

- Learn and embrace new technology. Like it or not, social media and technology that moves at lightning speed are here to stay. Demonstrate that you’re tech savvy and current. Get on Facebook, try Twitter (my personal favorite), or use Instagram to post your everyday life in pictures.

- If you don’t feel confident, get some advice. Check out the how-to’s on You Tube. There are workshops and courses that help, but your kids and grandkids know a lot … for free or for cookies.

- Build a strong network and reconnect with colleagues. Use LinkedIn for building and tracking professional contacts and FaceBook for personal stuff. These are powerful social media sites with features like private message options and groups to join. Phones still work to talk to friends and colleagues. And, yes, people still like getting phone calls.

- If you’re looking for that next job opportunity, use your knowledge and interests to share news stories, blog posts, and current off-the-beaten-path information with your LinkedIn connections.

- Be prepared for a long job search. Many jobs are online, but recruiters and your network are more helpful. As always, talking directly to people one-on-one provides you with valuable information. Talk to everyone you know about your interest in finding a new job in a particular industry. It works.

- Attend industry conferences in your local area. Chambers of Commerce are a great resource. Join a local volunteer committee to meet new groups of people who might connect you with others.

And don’t forget about the last 2

- Take a lateral move or even a step down for the right opportunity. Stepping sideways is not a bad way to go: “lattice vs. ladder” workers. By taking some steps down and across to work in areas you’ve always wanted to pursue, but couldn’t given demands at work and home, are super opportunities for fun and growth.

- Make sure you have a water-tight financial plan in place so you know you can afford to choose this path. Get tips on how to find a financial planner by checking out this blog post.

- Use any resources offered by the employer you are leaving: seminars, resume writing classes, career coaches. It’s a whole new, fun world out there.

- Don’t take an early retirement offer too emotionally; it’s just business. Instead, collect your experiences, memories, and results of the great work you have done and get ready to repackage you and your success. Using the resources offered can help you make faster progress.

Your 50s and 60s are a time for change and control. You’ve got the experience to become even more relevant with a stronger, more powerful voice. Bring it all to the table and go for what you want when that “early retirement offer” email arrives in your inbox. You’ll be in the place to seize the day if and when you need to do so.