Here’s quite an interesting story that sums up the current state of women and money. It’s definitely complicated.

Three women who are clearly friends sat behind me on a flight to Tampa recently. I was minding my own business, reading Sarah Smarsh’s book, Heartland. It’s a book about one woman’s journey to break the cycle of teenage motherhood and poverty here in the land of plenty. Then, I heard the word “retirement” from the row behind me. My ears perked right up. Were the women behind me talking about retiring? Is that why they were going to Florida?

While I try not to eavesdrop, I couldn’t help but tune in to their conversation. Sadly, I once again got a strong look into the situation of so many boomer women and their money.

The conversation went something like this:

Woman 1, “I’d really like to retire, but I just don’t know if we have enough money to.”

Woman 2, “Oh, I’m sure you have enough. You’ve been working for so long you must have enough saved.”

Woman 1, “I’m not sure and every time I ask my husband how we’re going to pay for things in retirement he says to me, ‘You keep asking me the same question. I’ve told you I’ve got things covered. Now, stop asking me.’”

Woman 3, “Well, maybe all is set then.”

Woman 1, “I just feel anxious about the whole thing. I don’t know if I should retire or if I should keep working. I really don’t know where the money is going to come from.”

Woman 2, “Well, don’t forget, you won’t be spending as much after you retire. And, remember, you don’t pay tax on any of your money any longer.”

Woman 3, “Oh, I don’t think that’s right. I think you do have to still pay taxes.”

Woman 1, “I just want to know where our money is going to come from.”

The drink cart came at that point and the conversation moved to something else. I was left speechless and quite sad.

So Much Is Wrong with This Conversation

At first, I felt badly for the woman who didn’t even know if she could or should retire. She was clearly ready to retire, but was so uncertain about where their money would come from, or if it would last, that she couldn’t move forward. What was wrong with that part of the conversation? Her husband! Maybe it would be fairer to say that their communication needed improving or that they needed a marriage counselor, or a financial advisor. Either way, the husband was withholding critical information from his wife. And, this is never ok in my book.

The second issue I had with the conversation was the lack of facts being exchanged among the women. One was plain old wrong—who would ever think they are excused from paying taxes?! The others didn’t know enough to counter her in any meaningful way.

The most disturbing issue for me was that these women were only now, on the cusp of their retirement years, thinking seriously about money. They were 40 years too late. Or were they?

Women and Their Money: It’s All Complicated

Married women have a complicated history with their husbands and their money. It is not always easy to sort out the issues when a husband feels he is the provider and protector. Many husbands don’t feel it’s necessary to share money and financial planning with their wives. Maybe well-intended, but the protector role does not leave Boomer women in a good or secure place. In fact, it will backfire when she’s left alone as a widow or ex-wife.

The Last 100 Years Opened the Gates for Women and Their Money

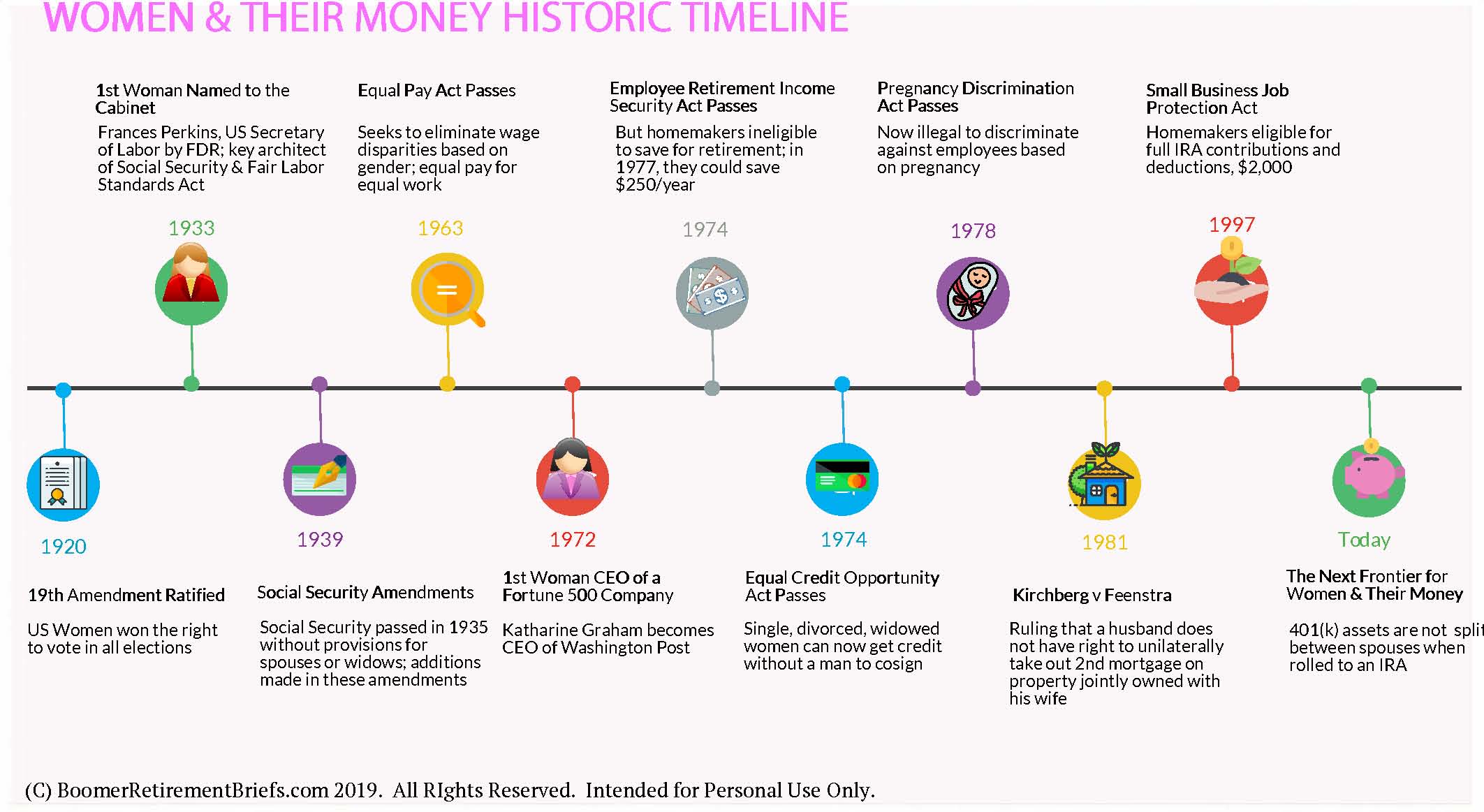

March is Women’s History month and I took this month to look more into women’s relationship with money. In trying to understand why women, and especially Boomer women (born 1946 – 1964), are so hesitant to own their own money, we find a trail of no opportunity. The issues of women and their money is rooted in centuries of bad behavior and archaic laws.

To illustrate the last 100 years, open up the timeline attached to this post: Women and Their Money_Timeline_030619 (1)The timeline highlights some of the laws that have passed giving women rights to their own money. It is a stunning reality to see how women’s hands and money were tied. Whether they were interested in personal finance or investments or not, any interest and involvement literally had no place in the home. And, I’m talking about here in the United States! Throughout the 1900’s.

Making Dinner Is Ok; Casting a Vote Is Not Ok

When you take a step back to look at what’s happened over the last 100 years in the US, it is both absolutely remarkable and disappointingly horrible. Forget the fact that women only won the right to vote in their own country in 1920. It was ok for women to walk across rugged terrain in long skirts during the westward expansion, work the farms alongside their husbands, grow the food, make dinner every day, and raise the children, but casting a vote? No, women’s voices didn’t count.

Thankfully, through political skill and will, and sheer determination, the 19th Amendment was ratified just about 100 years ago. We’ve seen in election after election how securing the women’s vote can be critical to the success of a candidate. Women’s voices do matter.

A Thirty-Year Span Between Key Legislation for Women

1935 saw the passage of the Social Security Act, helping to secure a somewhat dignified retirement for the workers of America, but not for their spouses. And, not for the widows of the workers. So, unless a woman was also working outside the home for reportable wages, there was no retirement social safety net for her.

This oversight was relatively quickly corrected with the Social Security Amendments in 1939. But really? Congress couldn’t acknowledge women who worked at home raising the children and managing the household? At-home moms made it possible for the men to work. How were they to live without any income in retirement?

Fast forward to 1963. Almost all Baby Boomers are born by 1963, when finally the Equal Pay Act passes. The idea that there should be equal pay for the same work regardless whether a man or a woman was doing the job took decades to get on the books. Even after Rosie the Riveter donned her coveralls and kerchief in the 1940’s to work in heavy manufacturing in the support of the War effort!

There still is a significant wage gap between women and men, but at least there are laws that try to address same job same pay. Unless women have access to the best paying jobs and opportunities to improve their weekly paychecks, it’s irrelevant to worry about them becoming investors. The concern is whether there is enough money for the basics of living: food, shelter, health care.

Three Really Awful Situations for Women and their Money

There are three laws that infuriate me like no others. They are laws that should never have been needed. But, the level of ridiculousness that was going on in the labor market and in banking is almost too much to take. What do you think about these?

• It wasn’t until 1974 that single, widowed, or divorced women could obtain a credit card…unless they could get a man to co-sign the application. And, the income she reported would be significantly discounted, keeping her credit line much smaller than it should have been. So, a woman’s money wasn’t as green as a man’s?

• I was a senior in high school in 1978, the same year a law finally passed making it illegal for employers to fire a pregnant woman. Those of us who worked all through our pregnancies, performing just as well on the job as when not pregnant, can’t even imagine being kicked out of a job because of our “condition”. No work, no pay. Again, it’s hard to become an investor when you have no money.

• Let’s consider the Small Business Job Protection Act of 1996. Buried in this bill was a small allowance for women who were at-home moms: The Homemaker’s IRA. Beginning in 1997, women who stayed at home to raise their children could finally save for retirement in their own IRA at the same amount as their working husband. Until then, they were totally dependent on their husbands for every dollar saved for retirement. There’s certainly no incentive for women to get involved saving for retirement when they are all but forbidden to save any money.

The Opportunities to Own Their Own Money Were Slow in Coming

The laws of the land all but jailed women for trying to get a foothold in the world of money and finance. They may have wanted to save and invest, and to get into the profit side of money. But women’s hands were tied at every juncture – from wage restrictions, to being fired for pregnancy, to being denied credit, to not even being allowed to save for their retirement.

To say a woman’s relationship with money is complicated is an understatement. Now, with only a few decades of a more even playing field, is it any wonder that more women are not more engaged in high finance and investing? Is it any wonder that many women don’t know the facts around investment policies and taxation? Is it any wonder that women are concerned and anxious about how they will be paying for their retirement? Sometimes women do put their heads in the sand…but, most often they’ve been blind-folded and told to look away.

At any point when a woman might have wanted to be more involved in her personal financial situation, she ran into a brick wall. Thankfully, most of the bricks have crumbled. However, women need to get into ownership of their money and their financial security in a more meaningful way. It will take some time to learn the skills and discipline needed to fully come up to speed on what it takes to be an investor.

3 Financial Steps to Take

When there is a reference to “women”, the assumption is that we are all the same. Not so. Many women have full control of their financial today and tomorrow. At the other end of the spectrum, we find the women in the row behind me on the plane who have been kept in the dark for far too long about their financial future.

Regardless of where you are on the money spectrum, there are key financial steps every woman—married, single, divorced, or widowed—should have in place. If you don’t have every one of these items, time to get a move-on!

1. Own an IRA –

Set up and fund as much as you can into an IRA. 2019’s limit is $6,000 per person, plus an additional $1,000 if you will be 50 or older. Even if you can only put a few hundred dollars into a Traditional or Roth IRA, do it. This account is a powerful. It gets you in the game. You have to fund it, invest the money, monitor and manage it for growth. More importantly, you own it outright. It is not a shared account. You make all the decisions, including who you’d like to receive the assets when you die. It does not matter if your contributions are tax-deductible or not. It’s about ownership and calling your own shots. It’s about your money.

2. Get a Credit Card in Your Name –

This is a card with just your name. Not a joint card with hubby. You may well need access to your own credit line at some point, and a shared credit line might not be available. Furthermore, as you are the sole owner on this credit card, you’ll solely be responsible for paying the bill. The responsibility is on you, and the benefit is yours as well. Those who manage their debt well, pay bills on time, and don’t overuse credit are rewarded with excellent FICO credit scores. The higher your score, the higher the credit line and more favorable interest rates you’ll receive when you need a car loan or a mortgage.

3. Set up your Personal Freedom Fund –

Having a little stash of cash is a great financial strategy for every woman. The idea here is that you set up and manage a taxable account that is just for you. It’s separate from the grocery money and household spending. Your checking account doesn’t count. Rather, it’s a savings account at a bank or investment company where you can tuck away a little bit of money every month or so for something you want in the future.

Read my blog post Ladies: How Big Is Your Freedom Fund? to get more information, or better yet, read my book: What’s the Deal With Retirement Planning For Women?

Though a woman’s relationship with money has been fraught with landmines, there is no longer any excuse for not starting or expanding your financial footprint. It’s a powerful thing when you have your own money. We have many women to thank who fought for each of us to have access to our money. Let’s make the most of what we’ve got!

More on the women who made women’s financial futures possible:

The Woman Behind the New Deal: The Life and Legacy of Frances Perkins, Social Security, Unemployment Insurance, and the Minimum Wage, by Kristin Downey

Women Make History for Women’s Retirement Security, by Marcia Mantell, published in Retirement Weekly

Lindy Boggs – Congresswoman behind the Equal Credit Opportunity Act. “She was influential in composing the Equal Credit Opportunity Act of 1974. When the Banking committee marked up the ECOA, she added the provision banning discrimination due to sex or marital status without informing the other members of the committee beforehand, personally inserting the language on her own and photocopying new versions of the bill.” (Wikipedia) And, she’s Cokie Roberts’ mother.