Much has changed in retirement from 2005 to 2025

It is wild to think that I started my independent consulting business 20 years ago this month. Frankly, I can’t believe it. On the one hand, it seems like just yesterday that I was setting up my office in the basement of my house. On the other hand, there is such a rich and wonderful history of clients and projects that I can’t deny all 240 months of work. July 1, 2005, was the first day of Mantell Retirement Consulting. My 20th anniversary is this month. Still shaking my head!

What were the grand plans for Mantell Retirement Consulting?

Well, grand business plans might be a bit of a stretch. Let’s just say that my plans included having dinner with my two wonderful children every night, gaining some flexibility to pick them up after school, going to all their soccer games, even if they were in the middle of the afternoon. And to make sure I could be a good Girl Scout mom and teach elementary students about money. I even organized a trip and tour of the Boston Federal Reserve Bank for the troop. The girls were giddy when they each got a bag of shredded US dollars!

In fact, my original plan was to take a year off after quitting my job at Fidelity. Back in 2005, there was no such thing as “work from home.” My boss gave me a hard time when I needed to leave early on an occasional Friday to do something with my kids. The 50–60 hours I had already logged by Thursday night didn’t count. And I was exhausted from traveling nearly every week.

I never did get that year off

Before I left Fidelity, one of the EVPs from another division asked me to work in a consulting role for him. He asked what my hourly rate would be. And then said, “Great. I’ll have a contract over to you next month.”

It’s pretty darn hard to say no to a gift like that. I ended up working for this division for 18 months. It was a great start to my business development.

I’ve worked non-stop for 20 years for the largest financial firms. Over the years, I turned my focus to helping financial advisors. Several employers have found me and asked for help with their older employees who are retiring. And consumers just find me and ask for help, often with sticky Social Security or Medicare situations.

Networking was key to my business success…

In this age of online job searching and sites like Monster.com and Indeed.com, it’s easy to forget the golden rule of business and career development. Network, network, network. You have to know people to get new jobs and new opportunities. Online bots and AI will not replace who you know.

I spent a lot of time staying connected with people in my professional sphere and attended many conferences. One of my big new financial clients approached me while standing in line for a buffet lunch at a conference. We had known each other from a distance, but started up a conversation while waiting for chicken and salad. Next thing I knew, she asked if I could help her build out the retirement income planning project her financial firm needed.

Yes, indeed, I could do that!

I loved being on the speaking circuit. And still do. I was an early adopter of online webinars and events. I was doing video work and virtual presentations way before the Covid pandemic forced almost everyone online.

…as well as another rule I lived by

That was another golden rule on my end. Say yes to opportunities that came my way. Don’t overthink it. Just say yes. I knew I’d figure it out once I got into the projects. And you never know where that one project—no matter how small—might lead in the future.

Some people think saying no is a better strategy than saying yes. They focus more in a niche or other specific area. I didn’t want to be bored. And almost every project I worked on added to my tool bag of knowledge and skills. I did not want to miss out on that development.

During my 20 years at Mantell Retirement Consulting, I rarely had to pitch for any business. My network was (and is) strong and my clients loyal. And I am a loyal consultant who keeps their work confidential. It’s been great!

My family has grown and changed over these 20 years…

The hardest part about looking in the rearview mirror is seeing how my kids have grown. Like most moms, I do miss those awesome years when the kids were home. They now live 1,400 miles away in Minnesota. There’s hardly a chance they’ll casually pop in for dinner. They are no longer the cute little cherubs who were my whole world back in 2005.

At 34 and 29, they are real adults. They may be fighting “adulting,” but they are doing it all. Working, taking good care of their pets, managing a house, and occasionally cooking…

I am truly so proud of them. And am so happy that we have stayed a close-knit family.

Dan and I are so different in some ways 20, more years into the game. It’s hard to believe we’ve been married for 42 years now. And had our first date in 1980. Really? How can that be?

He has been my biggest champion over the years I’ve had my own business. Now, he loves to be the trophy husband at events where I’m speaking on something retirement related.

…and the retirement industry and laws have rapidly changed

Speaking of retirement…how much has changed over these 20 years! While I was at Fidelity, I worked on projects that created what we now know as the rollover IRA business. And was involved in the early years of developing a retirement income program and RMD communications. Then, there were new products to launch: the Roth IRA, SIMPLE-IRA, and Homemaker’s IRA for at-home moms.

Every year, there were changes to the contribution limits. Or some rules of the game would be altered by Congress, the Labor Department, or FINRA. And we’d have to drop everything to implement those changes.

Since 2005, however, the speed and complexity of the changes in the retirement world have accelerated. The financial and retirement industries, as well as the legislature, are reckoning with the fact that at least 60% of American workers will not have enough money for all their retirement years.

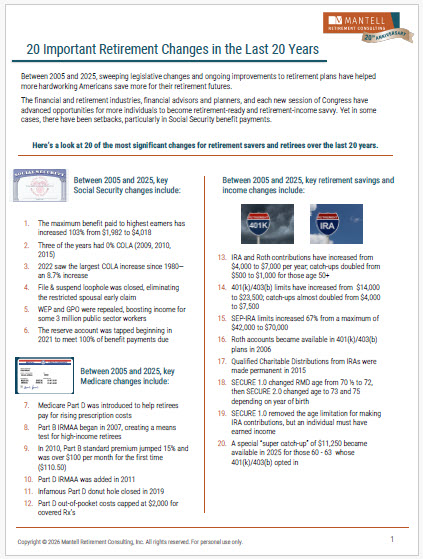

20 important retirement changes in the last two decades

I did a retrospective look at many of the rather dramatic changes in the retirement world. And came up with a list of 20. There are more, but this summary gives you a good look at how fast and how sweeping the changes have been.

Changes to the retirement savings and income categories are largely favorable. Employees and individuals generally have greater access to tax-advantaged savings and can save more than ever. There’s even a super catch-up provision for workers ages 60 to 63 in 401(k)s and 403(b)s. They can catch up to a maximum of $11,250.

Looking at the retirement income side of the equation, RMDs have improved from an owner’s perspective. Many folks won’t start taking distributions until age 75 (if born in 1960 or later). But most non-spouse inheritors will generally have to fully liquidate the account by the 10th year after death. And inheritors generally must continue RMDs if they had been started by the owner.

The attached chart gives you a good visual of what’s been happening over the past 20 years. Please click this link to access the full chart.

Social Security and Medicare have also changed

On the Social Security front, well, that is fraught with drama right now. Congress can’t get its act together to pass laws to shore up the program. But they’ve known about the depleting reserve account for all of these last 20 years. And longer. Since 2005, cost-of-living adjustments have been modest. Retired folks will say they can’t keep up with the high costs for their basics.

Medicare has also seen major changes, particularly the introduction of IRMAA for higher-income folks. The income-related monthly adjustment amounts are surcharges on the Part B and Part D premiums. High-income retirees are none too happy about that. However, out-of-pocket spending for covered prescription drugs has been capped at $2,000. This is a major improvement for people with high-priced drugs.

Do we finally have a solid, working retirement “formula?”

I’m going to go with no as my answer. With all these changes to retirement and tax laws, we’ve made a huge plate of spaghetti. Most American workers really have no idea how to navigate all these rules. Heck, the folks at Social Security and the IRS can’t keep up with the rules either!

The retirement laws take up tens of thousands of pages. There was an original law at some point. Plus, the corresponding regulations. Then the law was amended. And, amended again. And again, and again, and again.

I could spend every waking moment of the next 20 years deep in the details of these laws. And still not know everything.

Getting to retirement requires one set of knowledge and skills. Living off your assets throughout retirement requires a completely different level of know-how.

But I do appreciate that most retirement topics (except Social Security) are relatively bipartisan in Congress. And they do manage to make improvements for current and future retirees.

Where will Mantell Retirement Consulting be in 20 more years?

Fully retired, I hope! I’ve invested a lot in my small but mighty business. Building expertise in Social Security and Medicare was not on my dance card. Yet here I am. I’d like to continue building on the knowledge I already have and move it forward into the next years.

I’m not so sure I’m in the game for another 20. I think Dan and I will look at retirement some years from now. There is still so much to do and so many people to help.

For now, I’m going to enjoy a year of celebrating Mantell Retirement Consulting’s anniversary. And hope to update a couple of my books and meet some policymakers in Washington. Time will tell! Stay tuned!